Answered step by step

Verified Expert Solution

Question

1 Approved Answer

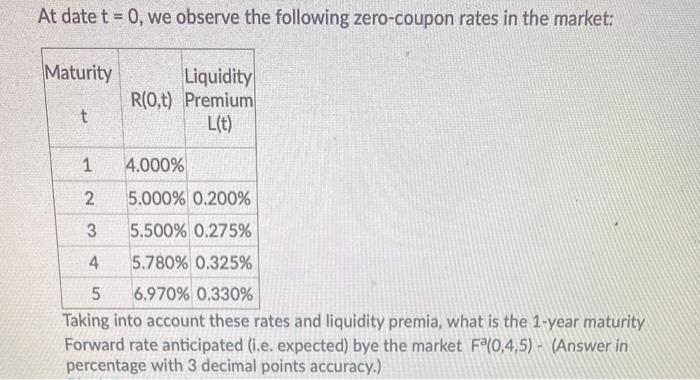

please show work At date t = 0, we observe the following zero-coupon rates in the market: Maturity Liquidity R(0,t) Premium L(t) t 1 4.000%

please show work

At date t = 0, we observe the following zero-coupon rates in the market: Maturity Liquidity R(0,t) Premium L(t) t 1 4.000% N 5.000% 0.200% 3 5.500% 0.275% 4 5.780% 0.325% 5 6.970% 0.330% Taking into account these rates and liquidity premia, what is the 1-year maturity Forward rate anticipated (i.e. expected) bye the market F*(0,4,5) - (Answer in percentage with 3 decimal points accuracy.) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Freedom And Finance Democratization And Institutional Investors In Developing Countries

Authors: M. Haley

1st Edition

0333914481, 1403940185, 9780333914489, 9781403940186