Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please show work for P8-14 a,b,c,d a. Calculate the expected portfolio return, , b. Calculate the expected value of portfolio returns, over the 6 c.

Please show work for P8-14 a,b,c,d

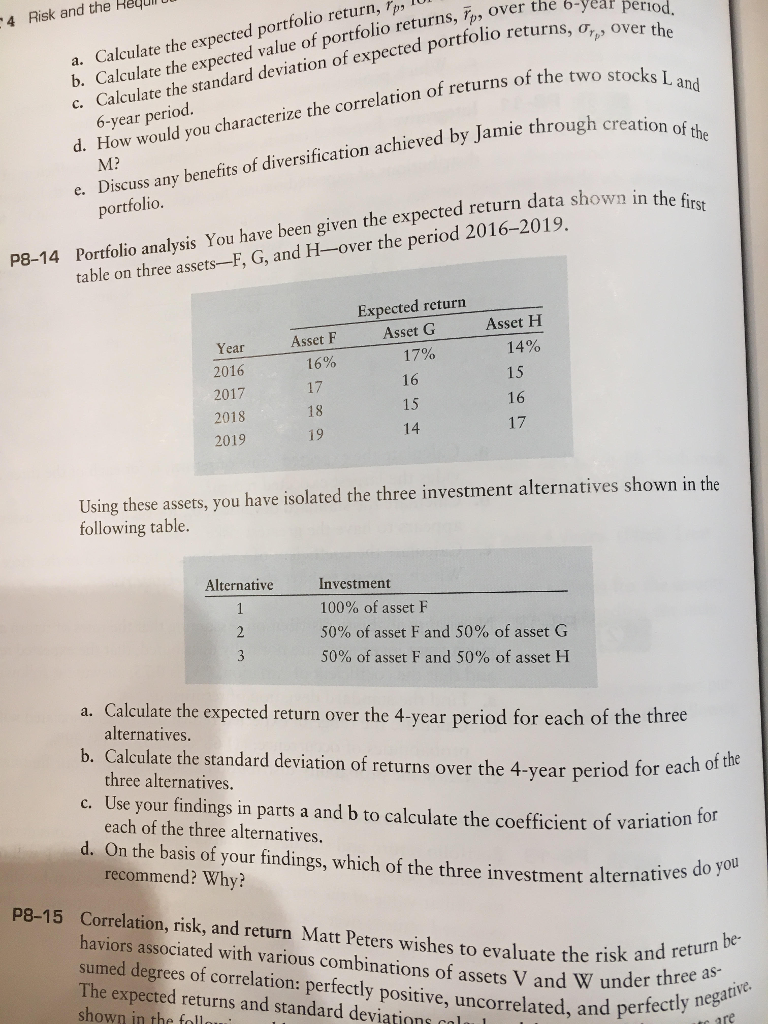

a. Calculate the expected portfolio return, , b. Calculate the expected value of portfolio returns, over the 6 c. Calculate the standard deviation of expected portfolio returns 4 Risk and the Heul , ,p, over the 6-year period. n achieved by Jamie through creation of he M? Discuss any benefits of diversification achieved by Jam portfolio d. How would you characterize the correlation of returns of the tw e. P8-14 Portfolio analysis You have been given the expected return data shown in the fico table on three assets-F, G, and H-over the period 2016-2019. Expected return Asset H Year Asset F Asset G 2016 2017 2018 2019 16% 17 18 17% 16 15 14 14% 15 16 17 Using these assets, you have isolated the three investment alternatives shown in the following table. Alternative Investment 100% of asset F 50% of asset F and 50% of asset G 50% of asset F and 50% of asset H a. Calculate the expected return over the 4-year period for each of the three b. Calculate the standard deviation of returns over the 4-year period for each alternatives three alternatives. c. Use your findings in parts a and b to calculate the coefficient of variation each of the three alternatives. d. On the basis of your findings, which of the three investment alternatives recommend? Why? do you P8-15 Correlation, risk, and return Matt Peters wishes to evaluate the risk and haviors associated with various combinations of assets V and W under negatie sumed degrees of correlation: perfectly positive, uncorrelated, and pert The expected returns and standard deviations caluu shown in the follo three as- perfectly negativeStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Trading From Your Gut How To Use Right Brain Instinct And Left Brain Smarts To Become A Master Trader

Authors: Curtis Faith

1st Edition

0137047681,0137051689