Answered step by step

Verified Expert Solution

Question

1 Approved Answer

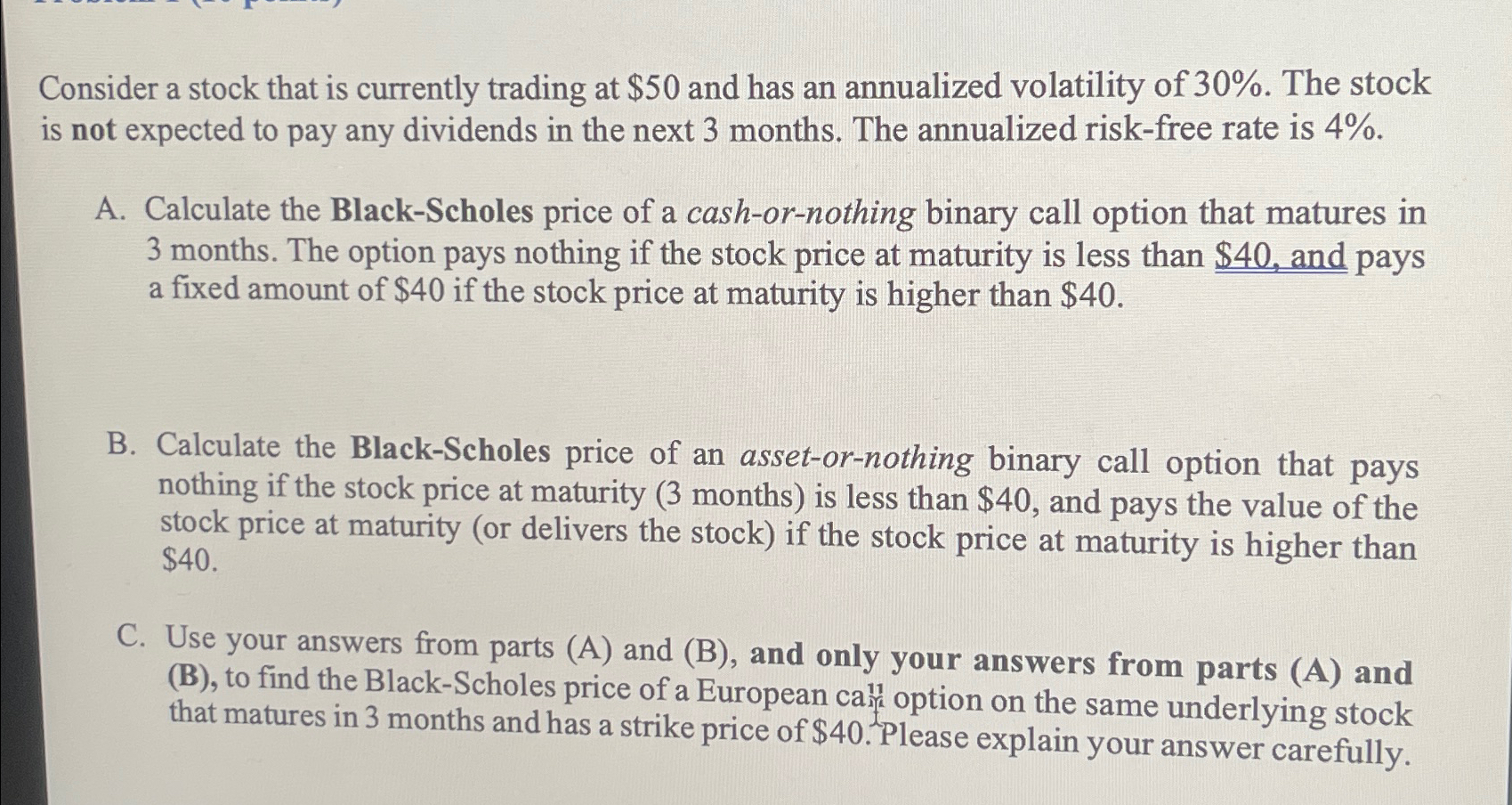

PLEASE SHOW WORK. No excel! Thank you Consider a stock that is currently trading at $ 5 0 and has an annualized volatility of 3

PLEASE SHOW WORK. No excel! Thank you

Consider a stock that is currently trading at $ and has an annualized volatility of The stock is not expected to pay any dividends in the next months. The annualized riskfree rate is

A Calculate the BlackScholes price of a cashornothing binary call option that matures in months. The option pays nothing if the stock price at maturity is less than $ and pays a fixed amount of $ if the stock price at maturity is higher than $

B Calculate the BlackScholes price of an assetornothing binary call option that pays nothing if the stock price at maturity months is less than $ and pays the value of the stock price at maturity or delivers the stock if the stock price at maturity is higher than $

C Use your answers from parts A and B and only your answers from parts A and B to find the BlackScholes price of a European ca option on the same underlying stock that matures in months and has a strike price of $ Please explain your answer carefully.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cases In Financial Management

Authors: I.M. Pandey

3rd Edition

0071333428, 978-0071333429