Question

Please show work with formulas in excel A portfolio manager is considering the benefits of increasing her diversification by investing overseas. She can purchase shares

Please show work with formulas in excel

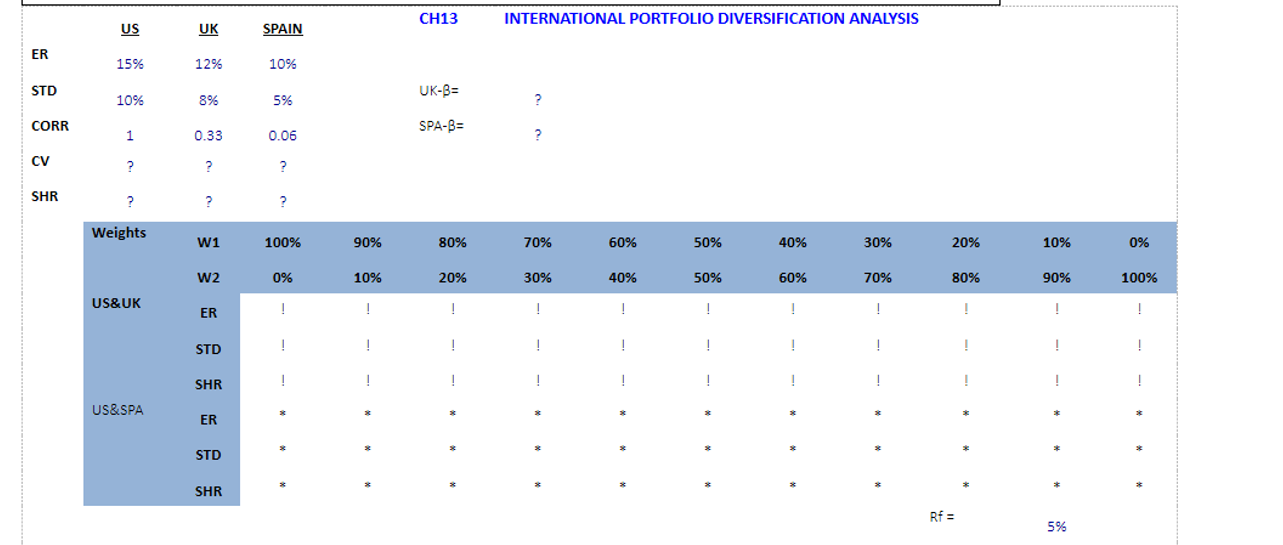

A portfolio manager is considering the benefits of increasing her diversification by investing overseas. She can purchase shares in individual country funds with the expected return (ER), standard deviation (STD) and correlations (CORR) characteristic provided above.

- Initially assume that exchange rate between $ and Pound and $ and Euro is expected to be stable (no change during the year). Assume that risk free rate is 5%.

- What are the expected returns, standard deviations of returns and sharp ratios of US&UK portfolios with different mixes such as 100% invested in US, 0% in UK; 90% invested in US, 10% in UK; 80% invested in US, 20% in UK;; 10% invested in US, 90% in UK; 0% invested in US, 100% in UK? Replace !s with the right info at the above table with the help of Excel formulas.

- What are the expected returns and standard deviations of returns of US & Spain portfolios with different mixes such as 100% invested in US, 0% in Spain; 90% invested in US, 10% in Spain; 80% invested in US, 20% in Spain;; 10% invested in US, 90% in Spain; 0% invested in US, 100% in Spain? Replace *s with the right info at the above table with the help of Excel formulas.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of European Financial Markets And Institutions

Authors: Xavier Freixas, Philipp Hartmann, Colin Mayer

1st Edition

0199229953, 978-0199229956