Answered step by step

Verified Expert Solution

Question

1 Approved Answer

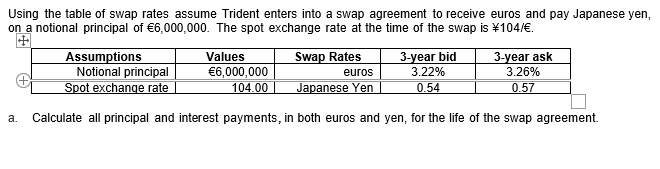

Please show your work thank you! Using the table of swap rates assume Trident enters into a swap agreement to receive euros and pay Japanese

Please show your work thank you!

Using the table of swap rates assume Trident enters into a swap agreement to receive euros and pay Japanese yen, on a notional principal of 6,000,000. The spot exchange rate at the time of the swap is 104/. Assumptions Values Swap Rates 3-year bid 3-year ask Notional principal 6,000,000 euros 3.22% 3.26% Spot exchange rate 104.00 Japanese Yen 0.54 0.57 a. Calculate all principal and interest payments, in both euros and yen, for the life of the swap agreement

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financing Large Projects Using Project Finance Techniques And Practices

Authors: Fouzul Khan, Robert Parra

1st Edition

9780131016347