please show your work this is one probelm thank you

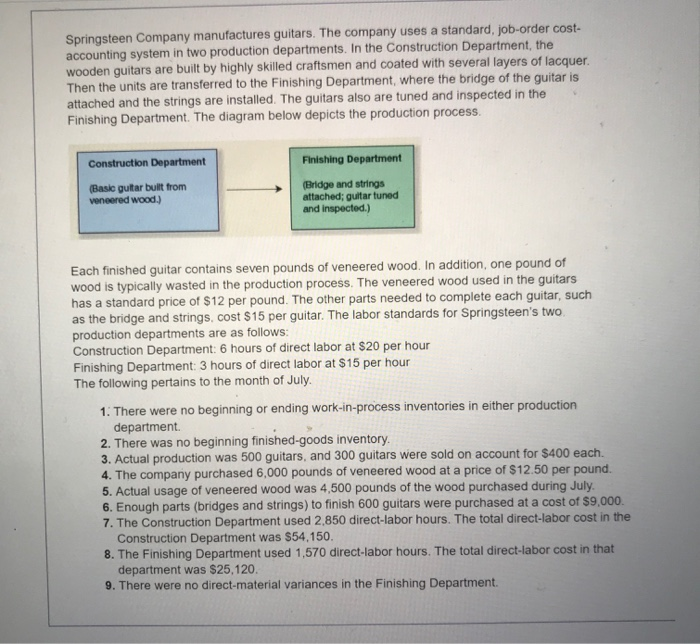

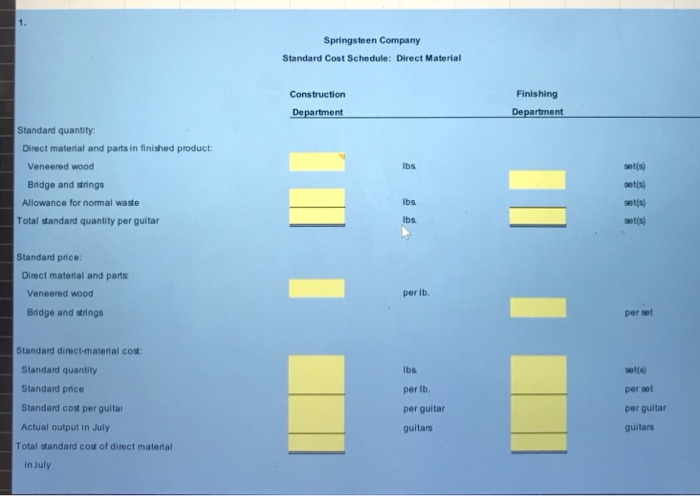

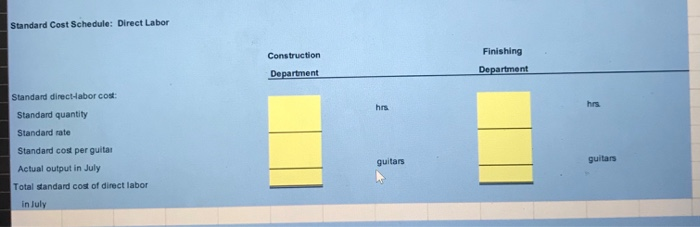

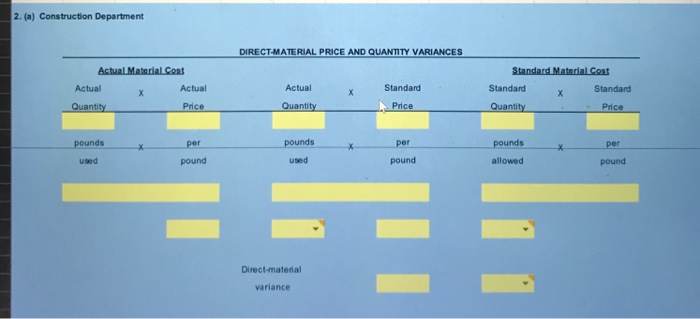

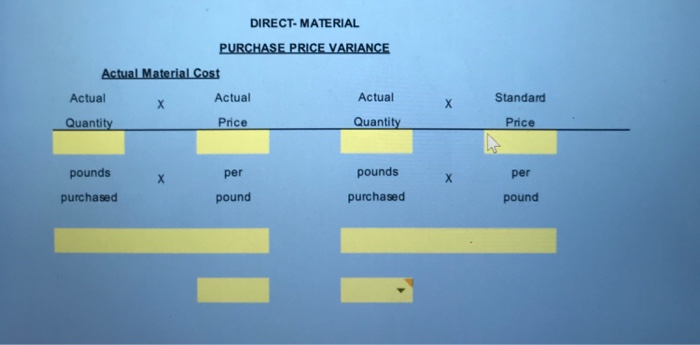

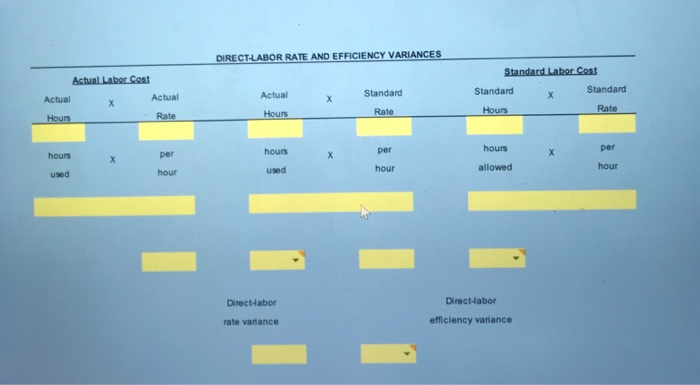

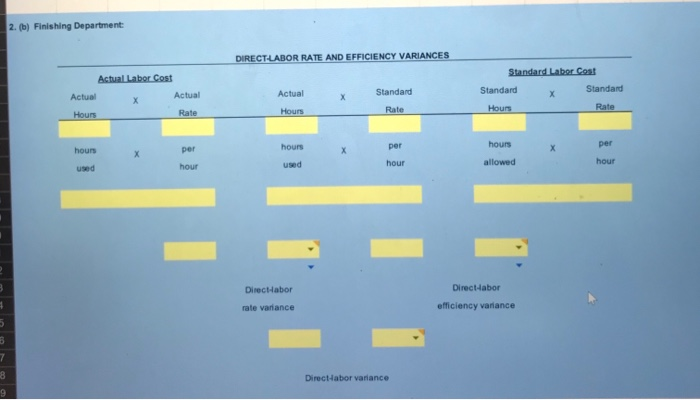

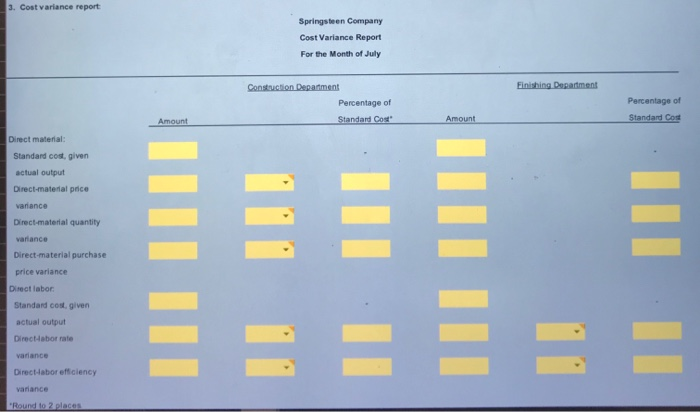

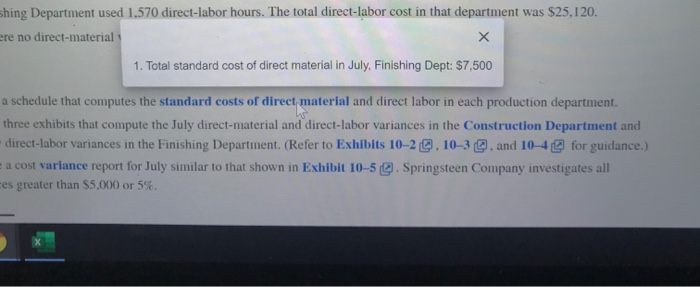

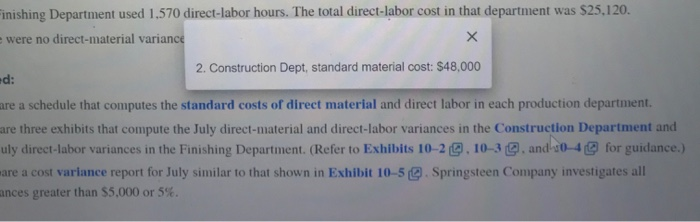

Springsteen Company manufactures guitars. The company uses a standard, job-order cost- accounting system in two production departments. In the Construction Department, the wooden guitars are built by highly skilled craftsmen and coated with several layers of lacquer. Then the units are transferred to the Finishing Department, where the bridge of the guitar is attached and the strings are installed. The guitars also are tuned and inspected in the Finishing Department. The diagram below depicts the production process. Construction Department Finishing Department (Basic guitar bult from veneered wood.) (Bridge and strings attached; guitar tuned and inspected.) Each finished guitar contains seven pounds of veneered wood. In addition, one pound of wood is typically wasted in the production process. The veneered wood used in the guitars has a standard price of $12 per pound. The other parts needed to complete each guitar, such as the bridge and strings, cost $15 per guitar. The labor standards for Springsteen's two production departments are as follows: Construction Department: 6 hours of direct labor at $20 per hour Finishing Department: 3 hours of direct labor at $15 per hour The following pertains to the month of July. 1. There were no beginning or ending work-in-process inventories in either production department 2. There was no beginning finished-goods inventory. 3. Actual production was 500 guitars, and 300 guitars were sold on account for $400 each. 4. The company purchased 6,000 pounds of veneered wood at a price of $12.50 per pound. 5. Actual usage of veneered wood was 4,500 pounds of the wood purchased during July 6. Enough parts (bridges and strings) to finish 600 guitars were purchased at a cost of $9,000. 7. The Construction Department used 2,850 direct-labor hours. The total direct-labor cost in the Construction Department was $54,150. 8. The Finishing Department used 1,570 direct-labor hours. The total direct-labor cost in that department was $25,120. 9. There were no direct-material variances in the Finishing Department. Springsteen Company Standard Cost Schedule: Direct Material Finishing Construction Department Department Standard quantity Direct material and parts in finished product: Veneered wood Bridge and strings Allowance for normal waste Total standard quantity per guitar sets Standard price: Direct material and parts Veneered wood Bridge and strings per Ib. per set Standard direct material cost Standard quantity Standard price per lb per set per guitar per guitar guitars guitars Standard cost per guitar Actual output in July Total standard cost of direct material in July Standard Cost Schedule: Direct Labor Construction Department Finishing Department Standard directabor cost Standard quantity Standard rate Standard cost per guitar Actual output in July Total standard cost of direct labor in July guitars guitar 2. (a) Construction Department DIRECT-MATERIAL PRICE AND QUANTITY VARIANCES Actual Material Cost X Actual Quantity Price Standard Material Cost Standard X Standard Actual Standard Quantity Price Quantity Price pounds pounds per pounds per per pound used used pound allowed pound Direct-material variance DIRECT- MATERIAL PURCHASE PRICE VARIANCE Actual Material Cost Actual Actual Quantity Price Actual Standard Price Quantity per pounds per pounds purchased pound purchased pound DIRECT-LABOR RATE AND EFFICIENCY VARIANCES Actual Laber Cost Actual X Actual Actual Standard Standard Labor Cost Standard Standard Hours Hous Rate Hours Rate Rate houng hours per hour hours used per hour per hour allowed Direct-abor Direct-abor efficiency variance rate variance 3. Cost variance report Springsteen Company Cost Variance Report For the Month of July Finishing Department Construction Department Percentage of Standard Cost Percentage of Standard Cos Direct material: Standard cost, given actual output Direct-material price variance Direct-material quantity variance Direct-material purchase price variance Dolabor Standard cost. given actual output Directorate variance Director efficiency variance R eplaces Required: 1. Prepare a schedule that computes the standard costs of direct material and direct labor in each production department, 2. Prepare three exhibits that compute the July direct-material and direct-labor variances in the Construction Department and the July direct labor variances in the Finishing Department. (Refer to Exhibits 10-20. 10-3 and 10-4 for guidance.) 3. Prepare a cost variance report for July similar to that shown in Exhibit 10-5 . Springsteen Company investigates all variances greater than $5,000 or 5%. shing Department used 1.570 direct-labor hours. The total direct-labor cost in that department was $25.120. ere no direct-material 1. Total standard cost of direct material in July, Finishing Dept: $7,500 a schedule that computes the standard costs or direct material and direct labor in each production department. three exhibits that compute the July direct-material and direct-labor variances in the Construction Department and direct-labor variances in the Finishing Department. (Refer to Exhibits 10-20 10-30 and 10-49 for guidance.) a cost variance report for July similar to that shown in Exhibit 10-5). Springsteen Company investigates all es greater than $5,000 or 5%. inishing Department used 1.570 direct-labor hours. The total direct-labor cost in that department was $25.120. were no direct-material variance 2. Construction Dept, standard material cost: $48,000 d: are a schedule that computes the standard costs of direct material and direct labor in each production department. are three exhibits that compute the July direct-material and direct-labor variances in the Construction Department and uly direct labor variances in the Finishing Department. (Refer to Exhibits 10-20. 10-3 C. and 0-4 for guidance.) are a cost variance report for July similar to that shown in Exhibit 10-50. Springsteen Company investigates all ances greater than $5,000 or 5%. onstruction Department was 5. Actual usage of veneered wood was 4,500 pounds of the wood purchased during July 6. Enough parts (bridges and strings) to finish 600 guitars were purchased at a cost of $9.000. 7. The Construction Department $54,150. 8. The Finishing Department used 3. Direct-material quantity variance, Construction Dept: $6,000 U 9. There were no direct-material variances in the Finishing Department, rtment was $25.120. Required: 1. Prepare a schedule that computes the standard costs of direct material and direct labor in each production department. 2. Prepare three exhibits that compute the July direct-material and direct-labor variances in the Construction Department and the July direct-labor variances in the Finishing Department. (Refer to Exhibits 10-20. 10-3 and 10-4 @ for guidance.) 3. Prepare a cost variance report for July similar to that shown in Exhibit 10-5 . Springsteen Company investigates all variances greater than $5,000 or 55 Springsteen Company manufactures guitars. The company uses a standard, job-order cost- accounting system in two production departments. In the Construction Department, the wooden guitars are built by highly skilled craftsmen and coated with several layers of lacquer. Then the units are transferred to the Finishing Department, where the bridge of the guitar is attached and the strings are installed. The guitars also are tuned and inspected in the Finishing Department. The diagram below depicts the production process. Construction Department Finishing Department (Basic guitar bult from veneered wood.) (Bridge and strings attached; guitar tuned and inspected.) Each finished guitar contains seven pounds of veneered wood. In addition, one pound of wood is typically wasted in the production process. The veneered wood used in the guitars has a standard price of $12 per pound. The other parts needed to complete each guitar, such as the bridge and strings, cost $15 per guitar. The labor standards for Springsteen's two production departments are as follows: Construction Department: 6 hours of direct labor at $20 per hour Finishing Department: 3 hours of direct labor at $15 per hour The following pertains to the month of July. 1. There were no beginning or ending work-in-process inventories in either production department 2. There was no beginning finished-goods inventory. 3. Actual production was 500 guitars, and 300 guitars were sold on account for $400 each. 4. The company purchased 6,000 pounds of veneered wood at a price of $12.50 per pound. 5. Actual usage of veneered wood was 4,500 pounds of the wood purchased during July 6. Enough parts (bridges and strings) to finish 600 guitars were purchased at a cost of $9,000. 7. The Construction Department used 2,850 direct-labor hours. The total direct-labor cost in the Construction Department was $54,150. 8. The Finishing Department used 1,570 direct-labor hours. The total direct-labor cost in that department was $25,120. 9. There were no direct-material variances in the Finishing Department. Springsteen Company Standard Cost Schedule: Direct Material Finishing Construction Department Department Standard quantity Direct material and parts in finished product: Veneered wood Bridge and strings Allowance for normal waste Total standard quantity per guitar sets Standard price: Direct material and parts Veneered wood Bridge and strings per Ib. per set Standard direct material cost Standard quantity Standard price per lb per set per guitar per guitar guitars guitars Standard cost per guitar Actual output in July Total standard cost of direct material in July Standard Cost Schedule: Direct Labor Construction Department Finishing Department Standard directabor cost Standard quantity Standard rate Standard cost per guitar Actual output in July Total standard cost of direct labor in July guitars guitar 2. (a) Construction Department DIRECT-MATERIAL PRICE AND QUANTITY VARIANCES Actual Material Cost X Actual Quantity Price Standard Material Cost Standard X Standard Actual Standard Quantity Price Quantity Price pounds pounds per pounds per per pound used used pound allowed pound Direct-material variance DIRECT- MATERIAL PURCHASE PRICE VARIANCE Actual Material Cost Actual Actual Quantity Price Actual Standard Price Quantity per pounds per pounds purchased pound purchased pound DIRECT-LABOR RATE AND EFFICIENCY VARIANCES Actual Laber Cost Actual X Actual Actual Standard Standard Labor Cost Standard Standard Hours Hous Rate Hours Rate Rate houng hours per hour hours used per hour per hour allowed Direct-abor Direct-abor efficiency variance rate variance 3. Cost variance report Springsteen Company Cost Variance Report For the Month of July Finishing Department Construction Department Percentage of Standard Cost Percentage of Standard Cos Direct material: Standard cost, given actual output Direct-material price variance Direct-material quantity variance Direct-material purchase price variance Dolabor Standard cost. given actual output Directorate variance Director efficiency variance R eplaces Required: 1. Prepare a schedule that computes the standard costs of direct material and direct labor in each production department, 2. Prepare three exhibits that compute the July direct-material and direct-labor variances in the Construction Department and the July direct labor variances in the Finishing Department. (Refer to Exhibits 10-20. 10-3 and 10-4 for guidance.) 3. Prepare a cost variance report for July similar to that shown in Exhibit 10-5 . Springsteen Company investigates all variances greater than $5,000 or 5%. shing Department used 1.570 direct-labor hours. The total direct-labor cost in that department was $25.120. ere no direct-material 1. Total standard cost of direct material in July, Finishing Dept: $7,500 a schedule that computes the standard costs or direct material and direct labor in each production department. three exhibits that compute the July direct-material and direct-labor variances in the Construction Department and direct-labor variances in the Finishing Department. (Refer to Exhibits 10-20 10-30 and 10-49 for guidance.) a cost variance report for July similar to that shown in Exhibit 10-5). Springsteen Company investigates all es greater than $5,000 or 5%. inishing Department used 1.570 direct-labor hours. The total direct-labor cost in that department was $25.120. were no direct-material variance 2. Construction Dept, standard material cost: $48,000 d: are a schedule that computes the standard costs of direct material and direct labor in each production department. are three exhibits that compute the July direct-material and direct-labor variances in the Construction Department and uly direct labor variances in the Finishing Department. (Refer to Exhibits 10-20. 10-3 C. and 0-4 for guidance.) are a cost variance report for July similar to that shown in Exhibit 10-50. Springsteen Company investigates all ances greater than $5,000 or 5%. onstruction Department was 5. Actual usage of veneered wood was 4,500 pounds of the wood purchased during July 6. Enough parts (bridges and strings) to finish 600 guitars were purchased at a cost of $9.000. 7. The Construction Department $54,150. 8. The Finishing Department used 3. Direct-material quantity variance, Construction Dept: $6,000 U 9. There were no direct-material variances in the Finishing Department, rtment was $25.120. Required: 1. Prepare a schedule that computes the standard costs of direct material and direct labor in each production department. 2. Prepare three exhibits that compute the July direct-material and direct-labor variances in the Construction Department and the July direct-labor variances in the Finishing Department. (Refer to Exhibits 10-20. 10-3 and 10-4 @ for guidance.) 3. Prepare a cost variance report for July similar to that shown in Exhibit 10-5 . Springsteen Company investigates all variances greater than $5,000 or 55