Answered step by step

Verified Expert Solution

Question

1 Approved Answer

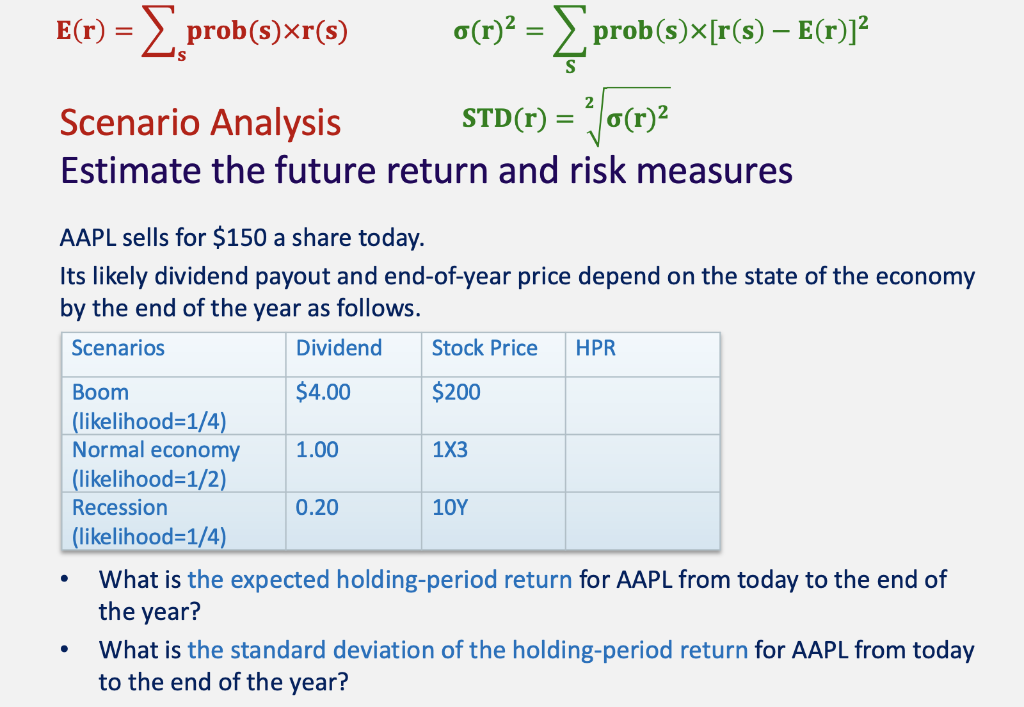

Please solve NOT using excel. E(r) prob(s)xr(s) o(r)2 = prob(s)[r(s) - E(r)]2 x r s S 2 Scenario Analysis Estimate the future return and risk

Please solve NOT using excel.

E(r) prob(s)xr(s) o(r)2 = prob(s)[r(s) - E(r)]2 x r s S 2 Scenario Analysis Estimate the future return and risk measures STD(r) = ? Jo(r)2 = AAPL sells for $150 a share today. Its likely dividend payout and end-of-year price depend on the state of the economy by the end of the year as follows. Scenarios Dividend Stock Price HPR Boom $4.00 $200 (likelihood=1/4) Normal economy 1.00 1X3 (likelihood=1/2) Recession 0.20 10Y (likelihood=1/4) What is the expected holding-period return for AAPL from today to the end of the year? What is the standard deviation of the holding-period return for AAPL from today to the end of the year? . E(r) prob(s)xr(s) o(r)2 = prob(s)[r(s) - E(r)]2 x r s S 2 Scenario Analysis Estimate the future return and risk measures STD(r) = ? Jo(r)2 = AAPL sells for $150 a share today. Its likely dividend payout and end-of-year price depend on the state of the economy by the end of the year as follows. Scenarios Dividend Stock Price HPR Boom $4.00 $200 (likelihood=1/4) Normal economy 1.00 1X3 (likelihood=1/2) Recession 0.20 10Y (likelihood=1/4) What is the expected holding-period return for AAPL from today to the end of the year? What is the standard deviation of the holding-period return for AAPL from today to the end of the yearStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Industrializing Financial Services With DevOps

Authors: Spyridon Maniotis

1st Edition

1804614343, 978-1804614341