Answered step by step

Verified Expert Solution

Question

1 Approved Answer

PLEASE SOLVE USING EXCEL AND SHOW FORMULA TEXT OR SHOW SOLVER PAGE Question 2: Suppose there are two risky assets: SKI Corp and JER Inc,

PLEASE SOLVE USING EXCEL AND SHOW FORMULA TEXT OR SHOW SOLVER PAGE

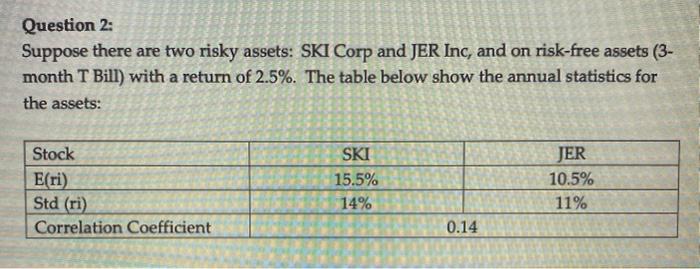

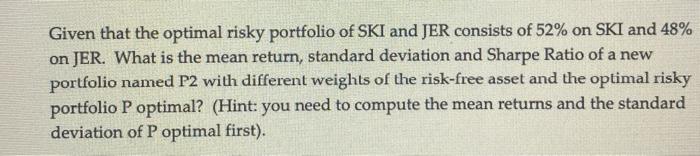

Question 2: Suppose there are two risky assets: SKI Corp and JER Inc, and on risk-free assets (3- month T Bill) with a return of 2.5%. The table below show the annual statistics for the assets: Stock E(ri) Std (ri) Correlation Coefficient SKI 15.5% 14% JER 10.5% 11% 0.14 Given that the optimal risky portfolio of SKI and JER consists of 52% on SKI and 48% on JER. What is the mean return, standard deviation and Sharpe Ratio of a new portfolio named P2 with different weights of the risk-free asset and the optimal risky portfolio P optimal? (Hint: you need to compute the mean returns and the standard deviation of P optimal first) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Multinational Finance

Authors: Michael H. Moffett, Arthur I. Stonehill, David K. Eiteman

4th Edition

9780132138079