Answered step by step

Verified Expert Solution

Question

1 Approved Answer

please summarize this for me 3. Finance as a digital platform industry: A global financial network perspective Our argument is that technological disruption in finance

please summarize this for me

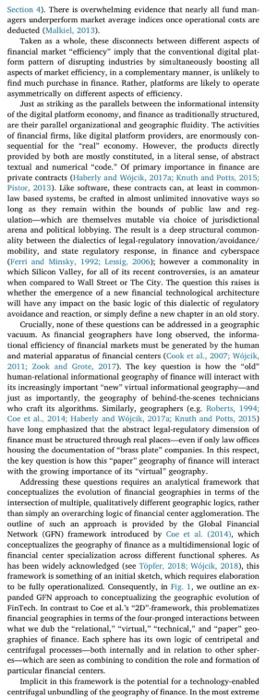

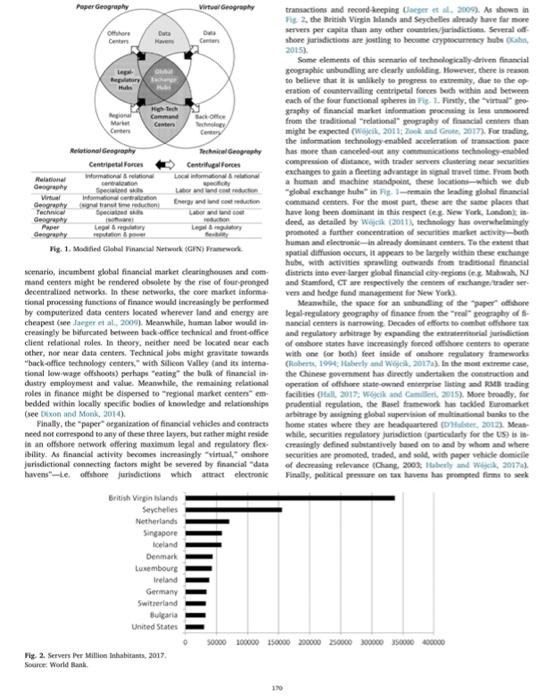

3. Finance as a digital platform industry: A global financial network perspective Our argument is that technological disruption in finance is increasingly converging on the digital platform model. However, finance has unusual characteristics that have caused this to occur in a different manner from other industries. Ironically, these differences stem from the extent to which two key features of the digital platform economy have always been central to finance; namely its informational intensity, and regulatory and organizational fluidity. Firstly, harnessing the power of "big data" to maximize market efficiency is more evolutionary than revolutionary in finance. Indeed, gathering and processing market information has always been the industry's lifeblood (Wjcik, 2011). From the standpoint of digital platform development, what is most important is that the financial sector's massive existing apparatus of information gathering and processing has, as noted by Tobin (1984), long produced a sharply asymmetrical development of different aspects of market "efficiency"-particularly in the securities market. Firstly, from an informational standpoint, financial markets tend to be characterized by much higher "information arbitrage efficiency" than "fundamental valuation efficiency." "Information arbitrage efficiency" is high in the sense that the market is so overcrowded with investors seeking to identify and exploit opportunities for pricing arbitrage, that it becomes difficult for anyone to consistently outsmart the market consensus. However, this does not mean that the consensus itself is particularly good at anticipating and pricing future events-as evidenced by volatility levels far in excess of changes in underlying fundamentals (Schiller, 2003; Tobin, 1994). Indeed, the same liquidity that enables "information arbitrage efficiency" may undermine "fundamental valuation efficiency" by facilitating speculative manias and other pathologies. Also very low, Tobin argues, is the "functional efficiency" of financial markets, as defined by the extent to which their operational costs (salaries, profits, etc.) are justified by the services they perform. From Tobin's standpoint, the key question is value to society. However, finance's "functional efficiency" is arguably also quite low for market participants. Indeed, as for fundamental valuation efficiency, low functional efficiency appears to be a counterintuitive corollary of high information arbitrage efficiency, as the same overcrowding of securities markets that allows for information to be rapidly incorporated into prices undermines the ability of participants to make money (see Section 4). There is overwhelming evidence that nearly all fund managers enderperform market average indices ance operatianal costs are deducted (Malkiel, 2013). Taken as a whole, these divconnects between different aspects of financial market "efficiency" imply that the conventional digital platform pattem of distopeing industries by simaltaneously boosting all aspects of market efficiency, in a complementary manner, is unlikely to find much putchase in finance. Rather, platiorms are likely to operate asymmetrically on differeat aspects of efticiency. Just as striking as the parallels between the informational intensity of the digital platform economy, and finance is traditionally structured, are their parallel organizational and geographic fluidity. The activities of financial firms, tike digital platform providers, are enormously consequential for the "real" economy. However, the producs directly provided by both are mostly constituted, in a literal sense, of abstract textual and numencal "code," of primary importance in finance are private contracts (Haherly and Wojcik, 2017a; Knath and Potis 2015; Fistuc, 2013). Lake softwase, these contracts can, at least in commonlaw based systems, be crafted in almost unlimited insovative ways so long as they remain within the bound of poblic law and reg. arena and political lobbying. The result is a deep structural commonality between the dialectios of lezal. regulatory innovation/avoidance/ mobility, and sate regulatory response, in finance and cyberspace which silican Valley, for all of its receet controversies, is an amateur when coenpared to Wall Street of The City. The questive this naises is whether the emergence of a sew fisancial technological architecture will have any impact on the basic logic of this dialectic of regulatory avoidence and reaction, or simply define a new chapter in an old story. Crucially, none of these questions can be addressed in a geographic vacuum, As financial geographers have long observed, the intormational efficiency of financial markets must be senerated by the human and material apparatus of financial centers (Cook et al, 2007, Wojeik, 2011; Zook and Grote, 2017). The key question is how the "old human-felational informational geograpay of tinasce wil tnteract with its increasingly important "new" virtual informational geography-and just as importantly, the geograptiy of behind-the-stenes technicians Who caft its algorithms, Simitarly, geographers (e) Roberts, 1994) finance mast be tructured through rral places-even if only lavoffice housing the documentation of "lotast plate" companies. In this respect, the key question is how this "paper" geogrophy of finance will interact with the growing importance of its "virtual" geography. Addressing these questions requires an analytical framework that conceptualizes the evolution of financial geographies in terms of the intersection of multiple, qualitatively different geographic logics, rather than simply an overarching logic of financial center agglomeration. The outline of ureh an approach it provided by the Clobal Financial Network (GFN) framework introdured by Coe et al. (2014), which conceptualizes the seography of finasce as a multidimensional logic of financial center specialization across different functional spheres. As has been widely acknowledged (yee ropter, 2015; Wojeli, 2018), this panded GFN approsch to concepeuselizing the geographic evolution of FinTech, In motras to Coe et al,y "2D"- frameirork, thit problematizet financial geographies in terms of the four-pronged interactions between what we dub the "relational," "virtual," "technical," and "paper" geographies of finance. Each sphere has its own logic of centripetal and centrifugal processes-both intemally and in relation to ocher spheres-which are seen as combining to condition the role and formation of particular finandial centers. Implicit in this framework is the potential for a technology-enabled centrifizgal unbuindling of the geography of finance. In the most extreme Fig. 2. Setvern Per Million linhabitants, 2017. Socurce, World Baali. plausible deniability by using larger (es - OE(D) havens (traesumint, 2013a). As shawn in Fig. 1, the paper gnography of finatice the remains anchored by what can be dubbed "legal-regulatory bubs" located within the dominant traditional financial centen-and above all the leading "global exchange hubs." This is not just a prablic regsatatury issue, but also entangled with the role of these centers as hels for private contractual law, whereia jurisdictional seputation and accsmulated legal precedent are of paramount importance. Indeed, the moet influential legul frameworks (e.g. New York) prowide the bosis for globat finandal law expoet industries (kinuth ind hers, 20t I3. Finally, the "technical" and "zelational" geographiles of Atance are entangled with both one another and the "paper" geography of tinance. Regardless of whether bumant are removed from directly perfiarmins activities (e.g. stokk-pickingt, the trehaical side of Enance mate be embedded in higher-order sector-specific saills and stratesy, respocstive to a rapudly changing competitive bendscape it is unclear whether "back-office technology-centers" can, regardilew of soff ware crpertise, compete with established financial centers in these respects. Particularly motable is that financial innavation muse, segarifien of technological content, involve "paper" contractual innevation regairing a deep expertise in relevant aneas of law and regulation (vee liaterify and Wojcik, 2017a. This entails not only fanniliarity with carrmat regulation, but also expertise and investment in the type of aestained political engegement necesary to stape regulation. Notatily, most of the largest Siticoe Valley firms, inclading Google and Amanon, have so far been deterred from entering fiaancial vervices by the anfamiliar and high-risk regulatery complesities this weald entail (Willerer ated Kurbat, 2017). While Faceboek is now breving these waters with its Lbea crypeocurrency project, it appears to be doiag a renarlably poer joh of ravigatieg their regulatory and potitical fimention (wre eanclusion)-particularly if one compares it to, for example, the polinical adeptness of Wall Street invertment banks at promoting firancial is: novation prior to the ylobul financial crisis (see Wojcik, 2012). Meas: nhile, the burgecoing scale of New York's Fintech indurtry underscoees the capacity for the larget tinanciul legal regulatury and exchange hubs to become centers of finance-specific software expertive (Gach and Gotsch, 2016). In the remainder of the paper, we pat the pieces fram the pereioet two sections together to examine the decpening technobopical discup? tion of asset management. As we show, this dieruption dosely fillows the patern sten in other sectors insofar as it exhibits both (1) a digital platform model of undercutting incumbent east structures by boonting various axpects of matket efficiency, and (2) the ausuciated dipital platform economy paradox of centralizetion through denocracitanion. However, the factors outlined in this section have alse resulted in notable divergences of the pattem of techanological distuptiod from that seen in sob-financial sectors Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Dave Ramseys Complete Guide To Money

Authors: Dave Ramsey

1st Edition

1937077209, 978-1937077204