Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please take the first derivative of the bond pricing formula (P = C/(1+y) + C/(1+y)^2 + ...) with respect to y to get this formula

Please take the first derivative of the bond pricing formula (P = C/(1+y) + C/(1+y)^2 + ...) with respect to "y" to get this formula

and then the second derivative to arrive at the convexity formula

Thank you

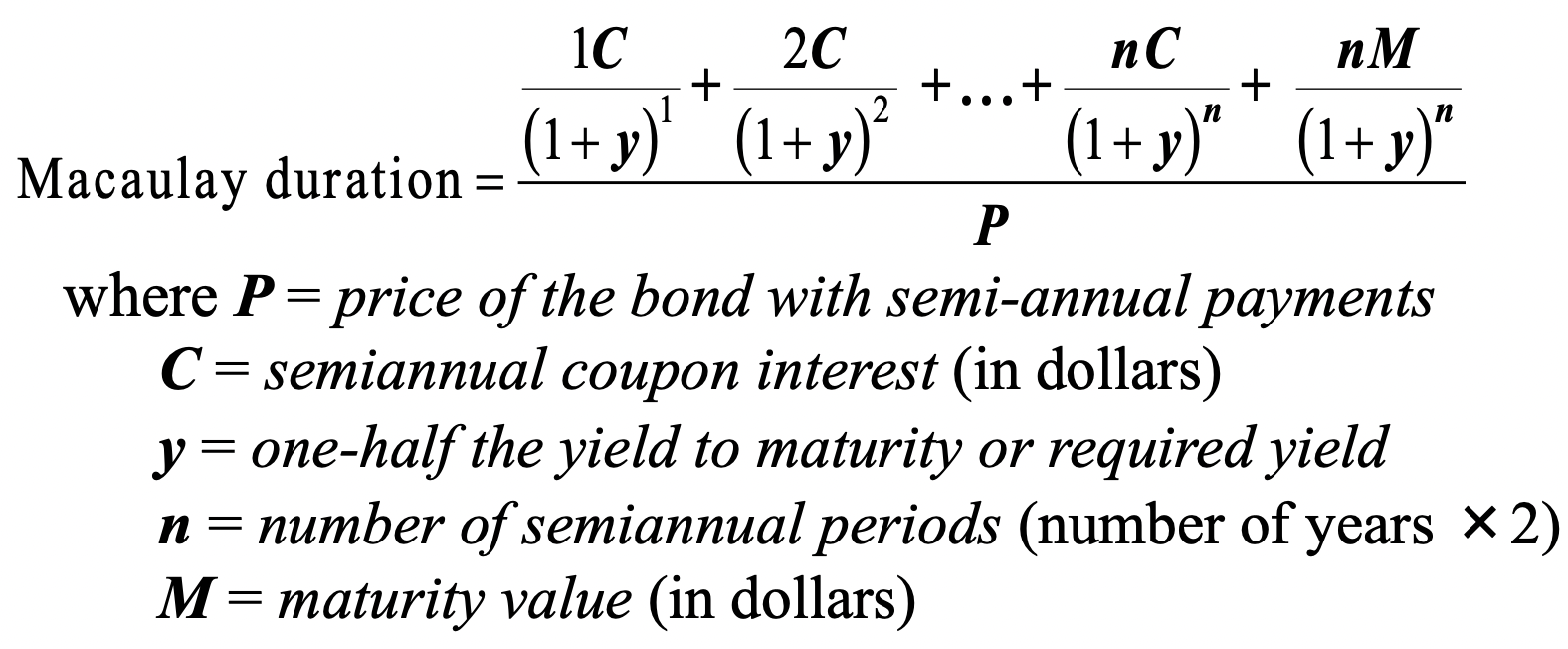

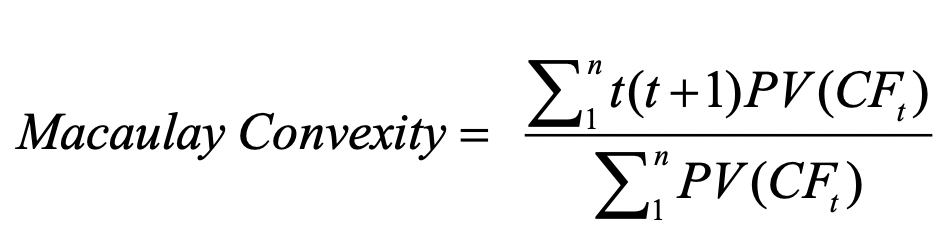

Macaulay duration =P(1+y)11C+(1+y)22C++(1+y)nnC+(1+y)nnM where P= price of the bond with semi-annual payments C= semiannual coupon interest (in dollars) y= one-half the yield to maturity or required yield n= number of semiannual periods (number of years 2, M= maturity value (in dollars) Macaulay Convexity =1nPV(CFt)1nt(t+1)PV(CFt)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial And Insurance Formulas

Authors: Tomas Cipra

2010th Edition

3790829013, 978-3790829013