Answered step by step

Verified Expert Solution

Question

1 Approved Answer

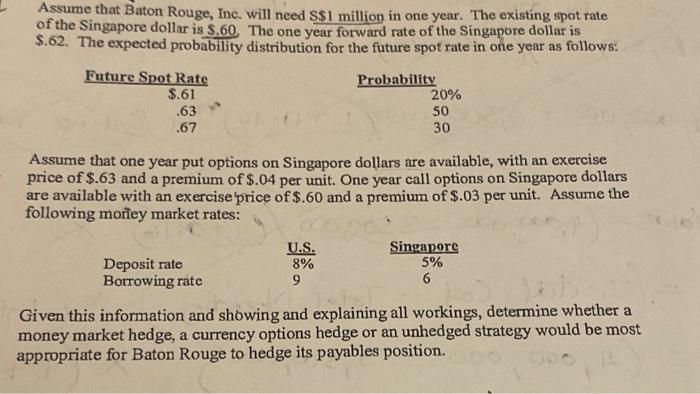

Please to show all workings especially for the put option. Assume that Baton Rouge, Inc. will need $1 million in one year. The existing spot

Please to show all workings especially for the put option.

Assume that Baton Rouge, Inc. will need $1 million in one year. The existing spot rate of the Singapore dollar is $,60. The one year forward rate of the Singapore dollar is \$.62. The expected probability distribution for the future spot rate in one year as follows: Assume that one year put options on Singapore dollars are available, with an exercise price of $.63 and a premium of $.04 per unit. One year call options on Singapore dollars are available with an exercise price of $.60 and a premium of $.03 per unit. Assume the following moriey market rates: Given this information and showing and explaining all workings, determine whether a money market hedge, a currency options hedge or an unhedged strategy would be most appropriate for Baton Rouge to hedge its payables position Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Family Inc Using Business Principles To Maximize Your Familys Wealth

Authors: Douglas P. McCormick

1st Edition

1119577411, 978-1119577416