Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Please upload all calculations formatted in Excel that support answers given, write-up in Word. Marks are awarded for the final answers, supporting calculations, and depth

Please upload all calculations formatted in Excel that support answers given, write-up in Word. Marks are awarded for the final answers, supporting calculations, and depth of detailed discussion.

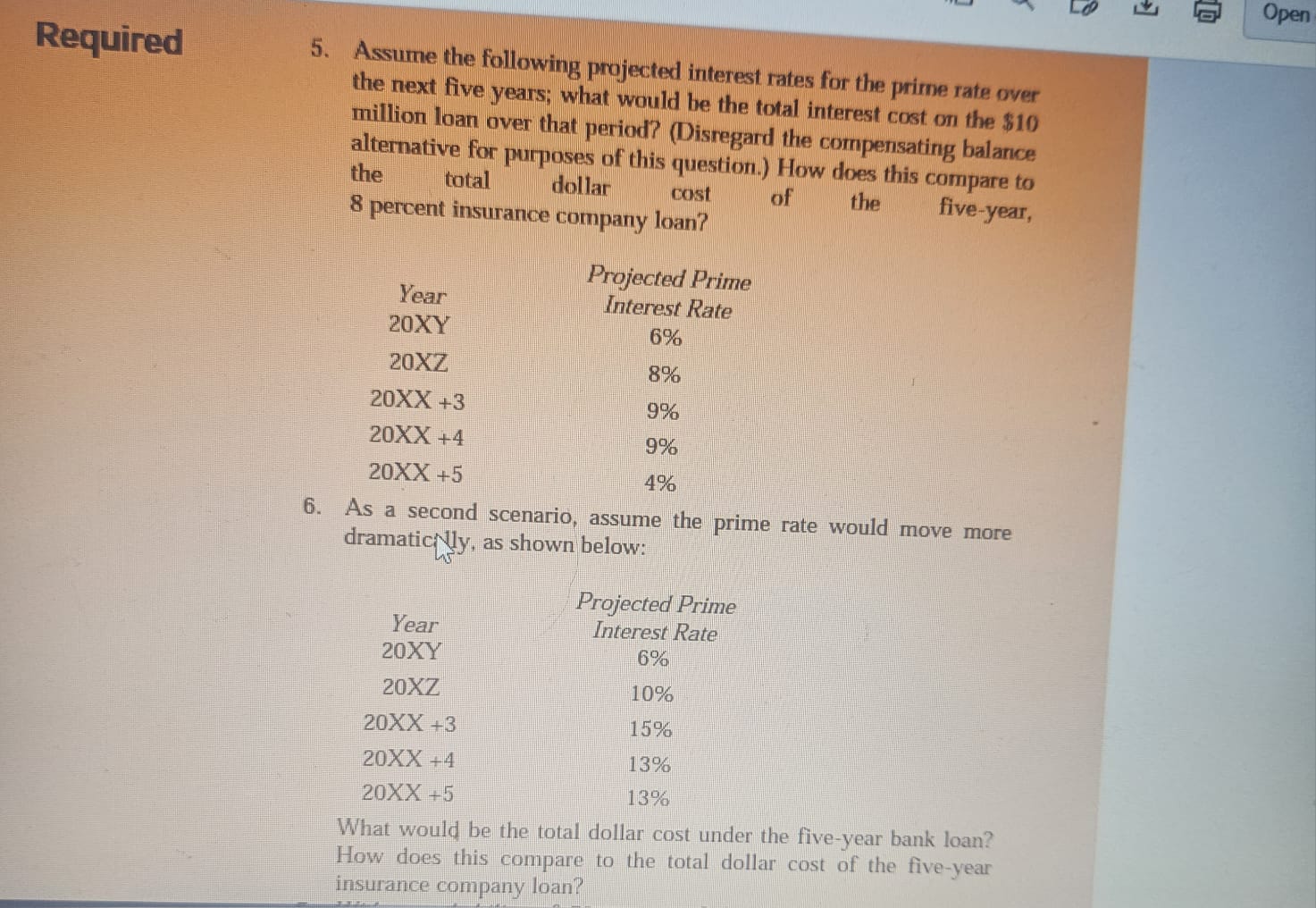

bank always floats the interest rate on its loans with the prime interest rate. Right now, the prime interest rate was 6 percent or a full 2 percent less than the rate Sam would have to pay on the longer-term insurance company loan. Furthermore, if Sam maintained compensating balances on 10 percent of the loan outstanding, the interest rate charge would be reduced to 1/2 percent below prime, or to 5k/2 percent. Clearly, there appeared to be a financial advantage to borrowing the money short term, but Sam also remembered that the prime interest rate could be quite volatile and had reached 20 percent back in 1981 . He would look pretty foolish to his boss, William Pierce III, if he were being forced to pay that kind of interest at some point in the future. Sam Fenton was also-concerned about the danger of a future credit crunch in the economy, as was witnessed in 2007 and 2008. At times banks become very hesitant to make loans because of an overabundance of bad loans already on their books and fears of federal regulators criticizing them. This is particularly true when the economy is in a recession and bank loan officers are fearful about future business conditions. What would be the total dollar cost under the five-year bank loan? How does this compare to the total dollar cost of the five-year insurance company loan? 7. With a probability of 70 percent of the interest rate scenario in question 5 and a 30 percent probability of the interest rate scenario in question 6 , what is the expected value of the dollar interest costs of short-term borrowing? Is this higher or lower than the total dollar interest cost of the five-year insurance company loan? 8. At what relative probability between the two scenarios would the firm be indifferent between short-term and long-term borrowing? 9. Briefly explain how hedging can help the firm reduce the risk associated with the short-term borrowing arrangement. 1. Based on the 10 percent compensating balance requirement, how much would Pierce Control Systems have to borrow to acquire $10 million in needed funds? 2. Would the cost of the bank loan with the 10 percent compensating balance requirement and a 521 percent rate applied to the total loan outstanding be more or less than the 6 percent prime rate loan on $10 million? Work this in terms of total dollar interest payments and compare the two answers. 3. What if 4 persent interest could be earned on all funds kept in excess of the $10 million under the compensating balance loan arrangement? What would be the net dollar interest cost of the compensating balance loan arrangement? How does this compare to the 6 percent prime interest rate loan total dollar cost? 4. Based on the difference between the 6 percent prime (short-term) interest rate charged by the bank and the 8 percent longer-term interest rate charged by the insurance company, what does this tell you about the likely current shape of the term structure of interest rates? Based on the expectations hypothesis, what might you infer is the next most likely move in interest rates? 5. Assume the following projected interest rates for the prime rate over the next five years; what would be the total interest cost on the $10 million loan over that period? (Disregard the compensating balance alternative for purposes of this question.) How does this compare to the total dollar cost 8 percent insurance company loan? of the five-year, 6. As a second scenario, assume the prime rate would move more dramatic Nly, as shown below: What would be the total dollar cost under the five-year bank loan? How does this compare to the total dollar cost of the five-year insurance company loan? bank always floats the interest rate on its loans with the prime interest rate. Right now, the prime interest rate was 6 percent or a full 2 percent less than the rate Sam would have to pay on the longer-term insurance company loan. Furthermore, if Sam maintained compensating balances on 10 percent of the loan outstanding, the interest rate charge would be reduced to 1/2 percent below prime, or to 5k/2 percent. Clearly, there appeared to be a financial advantage to borrowing the money short term, but Sam also remembered that the prime interest rate could be quite volatile and had reached 20 percent back in 1981 . He would look pretty foolish to his boss, William Pierce III, if he were being forced to pay that kind of interest at some point in the future. Sam Fenton was also-concerned about the danger of a future credit crunch in the economy, as was witnessed in 2007 and 2008. At times banks become very hesitant to make loans because of an overabundance of bad loans already on their books and fears of federal regulators criticizing them. This is particularly true when the economy is in a recession and bank loan officers are fearful about future business conditions. What would be the total dollar cost under the five-year bank loan? How does this compare to the total dollar cost of the five-year insurance company loan? 7. With a probability of 70 percent of the interest rate scenario in question 5 and a 30 percent probability of the interest rate scenario in question 6 , what is the expected value of the dollar interest costs of short-term borrowing? Is this higher or lower than the total dollar interest cost of the five-year insurance company loan? 8. At what relative probability between the two scenarios would the firm be indifferent between short-term and long-term borrowing? 9. Briefly explain how hedging can help the firm reduce the risk associated with the short-term borrowing arrangement. 1. Based on the 10 percent compensating balance requirement, how much would Pierce Control Systems have to borrow to acquire $10 million in needed funds? 2. Would the cost of the bank loan with the 10 percent compensating balance requirement and a 521 percent rate applied to the total loan outstanding be more or less than the 6 percent prime rate loan on $10 million? Work this in terms of total dollar interest payments and compare the two answers. 3. What if 4 persent interest could be earned on all funds kept in excess of the $10 million under the compensating balance loan arrangement? What would be the net dollar interest cost of the compensating balance loan arrangement? How does this compare to the 6 percent prime interest rate loan total dollar cost? 4. Based on the difference between the 6 percent prime (short-term) interest rate charged by the bank and the 8 percent longer-term interest rate charged by the insurance company, what does this tell you about the likely current shape of the term structure of interest rates? Based on the expectations hypothesis, what might you infer is the next most likely move in interest rates? 5. Assume the following projected interest rates for the prime rate over the next five years; what would be the total interest cost on the $10 million loan over that period? (Disregard the compensating balance alternative for purposes of this question.) How does this compare to the total dollar cost 8 percent insurance company loan? of the five-year, 6. As a second scenario, assume the prime rate would move more dramatic Nly, as shown below: What would be the total dollar cost under the five-year bank loan? How does this compare to the total dollar cost of the five-year insurance company loan

bank always floats the interest rate on its loans with the prime interest rate. Right now, the prime interest rate was 6 percent or a full 2 percent less than the rate Sam would have to pay on the longer-term insurance company loan. Furthermore, if Sam maintained compensating balances on 10 percent of the loan outstanding, the interest rate charge would be reduced to 1/2 percent below prime, or to 5k/2 percent. Clearly, there appeared to be a financial advantage to borrowing the money short term, but Sam also remembered that the prime interest rate could be quite volatile and had reached 20 percent back in 1981 . He would look pretty foolish to his boss, William Pierce III, if he were being forced to pay that kind of interest at some point in the future. Sam Fenton was also-concerned about the danger of a future credit crunch in the economy, as was witnessed in 2007 and 2008. At times banks become very hesitant to make loans because of an overabundance of bad loans already on their books and fears of federal regulators criticizing them. This is particularly true when the economy is in a recession and bank loan officers are fearful about future business conditions. What would be the total dollar cost under the five-year bank loan? How does this compare to the total dollar cost of the five-year insurance company loan? 7. With a probability of 70 percent of the interest rate scenario in question 5 and a 30 percent probability of the interest rate scenario in question 6 , what is the expected value of the dollar interest costs of short-term borrowing? Is this higher or lower than the total dollar interest cost of the five-year insurance company loan? 8. At what relative probability between the two scenarios would the firm be indifferent between short-term and long-term borrowing? 9. Briefly explain how hedging can help the firm reduce the risk associated with the short-term borrowing arrangement. 1. Based on the 10 percent compensating balance requirement, how much would Pierce Control Systems have to borrow to acquire $10 million in needed funds? 2. Would the cost of the bank loan with the 10 percent compensating balance requirement and a 521 percent rate applied to the total loan outstanding be more or less than the 6 percent prime rate loan on $10 million? Work this in terms of total dollar interest payments and compare the two answers. 3. What if 4 persent interest could be earned on all funds kept in excess of the $10 million under the compensating balance loan arrangement? What would be the net dollar interest cost of the compensating balance loan arrangement? How does this compare to the 6 percent prime interest rate loan total dollar cost? 4. Based on the difference between the 6 percent prime (short-term) interest rate charged by the bank and the 8 percent longer-term interest rate charged by the insurance company, what does this tell you about the likely current shape of the term structure of interest rates? Based on the expectations hypothesis, what might you infer is the next most likely move in interest rates? 5. Assume the following projected interest rates for the prime rate over the next five years; what would be the total interest cost on the $10 million loan over that period? (Disregard the compensating balance alternative for purposes of this question.) How does this compare to the total dollar cost 8 percent insurance company loan? of the five-year, 6. As a second scenario, assume the prime rate would move more dramatic Nly, as shown below: What would be the total dollar cost under the five-year bank loan? How does this compare to the total dollar cost of the five-year insurance company loan? bank always floats the interest rate on its loans with the prime interest rate. Right now, the prime interest rate was 6 percent or a full 2 percent less than the rate Sam would have to pay on the longer-term insurance company loan. Furthermore, if Sam maintained compensating balances on 10 percent of the loan outstanding, the interest rate charge would be reduced to 1/2 percent below prime, or to 5k/2 percent. Clearly, there appeared to be a financial advantage to borrowing the money short term, but Sam also remembered that the prime interest rate could be quite volatile and had reached 20 percent back in 1981 . He would look pretty foolish to his boss, William Pierce III, if he were being forced to pay that kind of interest at some point in the future. Sam Fenton was also-concerned about the danger of a future credit crunch in the economy, as was witnessed in 2007 and 2008. At times banks become very hesitant to make loans because of an overabundance of bad loans already on their books and fears of federal regulators criticizing them. This is particularly true when the economy is in a recession and bank loan officers are fearful about future business conditions. What would be the total dollar cost under the five-year bank loan? How does this compare to the total dollar cost of the five-year insurance company loan? 7. With a probability of 70 percent of the interest rate scenario in question 5 and a 30 percent probability of the interest rate scenario in question 6 , what is the expected value of the dollar interest costs of short-term borrowing? Is this higher or lower than the total dollar interest cost of the five-year insurance company loan? 8. At what relative probability between the two scenarios would the firm be indifferent between short-term and long-term borrowing? 9. Briefly explain how hedging can help the firm reduce the risk associated with the short-term borrowing arrangement. 1. Based on the 10 percent compensating balance requirement, how much would Pierce Control Systems have to borrow to acquire $10 million in needed funds? 2. Would the cost of the bank loan with the 10 percent compensating balance requirement and a 521 percent rate applied to the total loan outstanding be more or less than the 6 percent prime rate loan on $10 million? Work this in terms of total dollar interest payments and compare the two answers. 3. What if 4 persent interest could be earned on all funds kept in excess of the $10 million under the compensating balance loan arrangement? What would be the net dollar interest cost of the compensating balance loan arrangement? How does this compare to the 6 percent prime interest rate loan total dollar cost? 4. Based on the difference between the 6 percent prime (short-term) interest rate charged by the bank and the 8 percent longer-term interest rate charged by the insurance company, what does this tell you about the likely current shape of the term structure of interest rates? Based on the expectations hypothesis, what might you infer is the next most likely move in interest rates? 5. Assume the following projected interest rates for the prime rate over the next five years; what would be the total interest cost on the $10 million loan over that period? (Disregard the compensating balance alternative for purposes of this question.) How does this compare to the total dollar cost 8 percent insurance company loan? of the five-year, 6. As a second scenario, assume the prime rate would move more dramatic Nly, as shown below: What would be the total dollar cost under the five-year bank loan? How does this compare to the total dollar cost of the five-year insurance company loan Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Bitcoin A Beginner S Guide

Authors: Benjamin Hart

1st Edition

0578389533, 978-0578389530