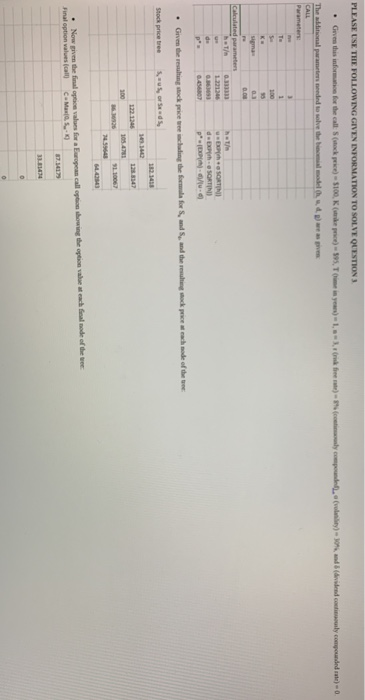

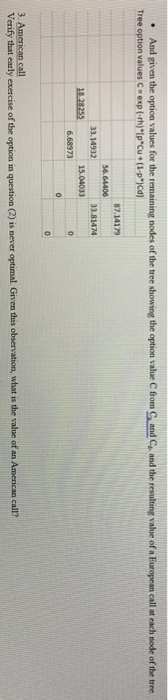

PLEASE USE THE FOLLOWING GIVEN INFORMATION TO SOLVE QUESTION 3 Grven this infomation for the call: s (tock price) $100, K (ke price)-S5, T e in year)-1,-3,ik fee ate)-% (cotily compounde, o (volatlity)-30% and & (dividend costiouly conpounded rate)0 The additional parameters aeeded to solve de bincmial model , dp) are as gives CALL Parameters Te 1 S 100 K sigma 03 0.0 Calculated parameters hT/ 1221246 0863693 0456807 usEXpph SORTIN dEXPh-SQRTIN p(E /u- ue de Given the resulting stock price ree inclading the formala for S, and S and the resuhting ock price at each node of the toee Stock price tree u or Sed 182.148 1.3442 122.1246 128.8347 300 105.4781 6326 110067 74.55648 6442543 Now given the final opticn values for a European call option showing the option value at each fieal node of the tee Final option values (call) C Max(0 S K 87.34179 33.81434 0 0 And given the option values for the remaining nodes of the tree showing the option value C from C, and C and the resulting value of a European call at each node of the tree Tree option values C exp (-rh)*(p*Cu + (1-p* )Cd) 87.14179 56.64406 33.14932 33.81474 18.28255 15.04033 6.68973 0 3. American call Verify that early exercise of the option in question (2) is never optimal Grven this observation, what is the value of an American call? PLEASE USE THE FOLLOWING GIVEN INFORMATION TO SOLVE QUESTION 3 Grven this infomation for the call: s (tock price) $100, K (ke price)-S5, T e in year)-1,-3,ik fee ate)-% (cotily compounde, o (volatlity)-30% and & (dividend costiouly conpounded rate)0 The additional parameters aeeded to solve de bincmial model , dp) are as gives CALL Parameters Te 1 S 100 K sigma 03 0.0 Calculated parameters hT/ 1221246 0863693 0456807 usEXpph SORTIN dEXPh-SQRTIN p(E /u- ue de Given the resulting stock price ree inclading the formala for S, and S and the resuhting ock price at each node of the toee Stock price tree u or Sed 182.148 1.3442 122.1246 128.8347 300 105.4781 6326 110067 74.55648 6442543 Now given the final opticn values for a European call option showing the option value at each fieal node of the tee Final option values (call) C Max(0 S K 87.34179 33.81434 0 0 And given the option values for the remaining nodes of the tree showing the option value C from C, and C and the resulting value of a European call at each node of the tree Tree option values C exp (-rh)*(p*Cu + (1-p* )Cd) 87.14179 56.64406 33.14932 33.81474 18.28255 15.04033 6.68973 0 3. American call Verify that early exercise of the option in question (2) is never optimal Grven this observation, what is the value of an American call