Answered step by step

Verified Expert Solution

Question

1 Approved Answer

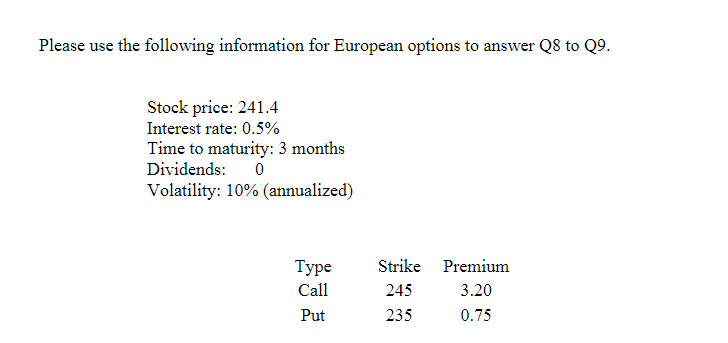

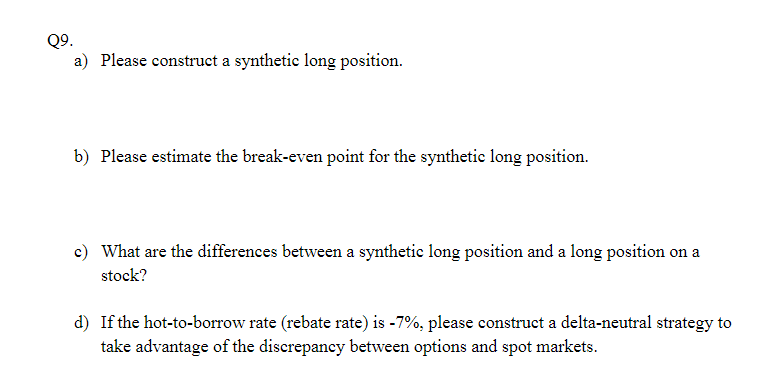

Please use the following information for European options to answer Q8 to 29. Stock price: 241.4 Interest rate: 0.5% Time to maturity: 3 months Dividends:

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

How To Be A Good Accountant A Comprehensive Guide To Developing Professional Accounting Qualities

Authors: WILLIAM S. CUSSON

1st Edition

979-8366157773