Answered step by step

Verified Expert Solution

Question

1 Approved Answer

PLEASE WRITE IT BY WORD NOT HAND T Save Pen Eraser Text Undo Redo Question 4) There are three securities in a portfolio. For each

PLEASE WRITE IT BY WORD NOT HAND

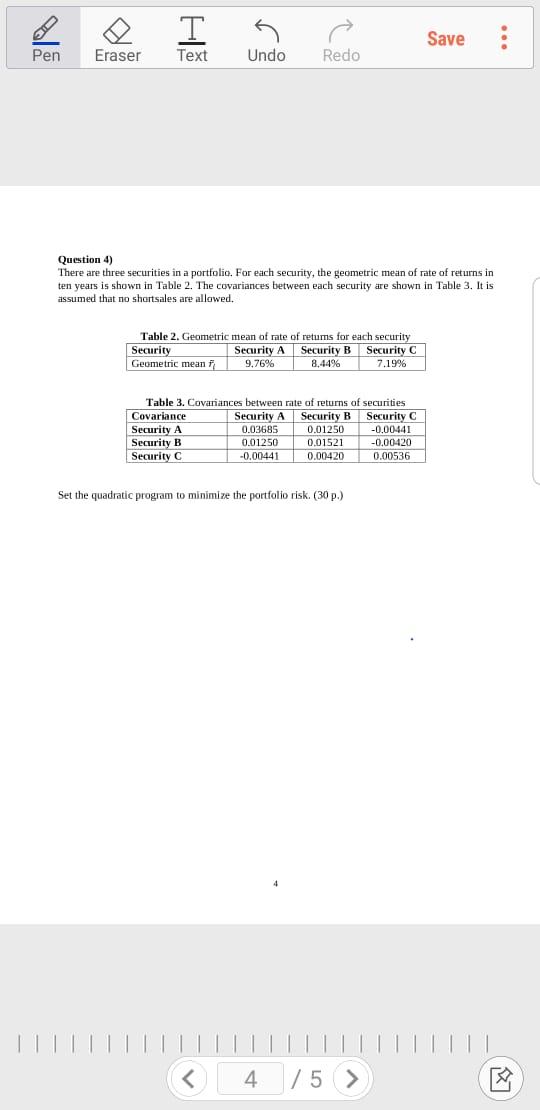

T Save Pen Eraser Text Undo Redo Question 4) There are three securities in a portfolio. For each security, the geometric mean of rate of returns in ten years is shown in Table 2. The covariances between each security are shown in Table 3. It is assumed that no shortsales are allowed. Table 2. Geometric mean of rate of retums for each security Security Security A Security B Security C Geometric mean 9,76% 8,44% 7.19% Table 3. Covariances between rate of returns of securities Covariance Security A Security B Security C Security A 0.03685 0.01250 -0.00441 Security B 0.01250 0.01521 -0.00420 Security C -0.00441 0.00420 0.00536 Set the quadratic program to minimize the portfolio risk. (30 p.) T Save Pen Eraser Text Undo Redo Question 4) There are three securities in a portfolio. For each security, the geometric mean of rate of returns in ten years is shown in Table 2. The covariances between each security are shown in Table 3. It is assumed that no shortsales are allowed. Table 2. Geometric mean of rate of retums for each security Security Security A Security B Security C Geometric mean 9,76% 8,44% 7.19% Table 3. Covariances between rate of returns of securities Covariance Security A Security B Security C Security A 0.03685 0.01250 -0.00441 Security B 0.01250 0.01521 -0.00420 Security C -0.00441 0.00420 0.00536 Set the quadratic program to minimize the portfolio risk. (30 p.)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Corporate Finance

Authors: David W Blackwell, Robert Parrino, David S Kidwell

1st Edition

0471270563, 9780471270560