Please write part efgh. Part abcd answers are 8.500%, 9.509%, $91.316, and 7.50% respectively. Thank you!

Please write part efgh. Part abcd answers are 8.500%, 9.509%, $91.316, and 7.50% respectively. Thank you!

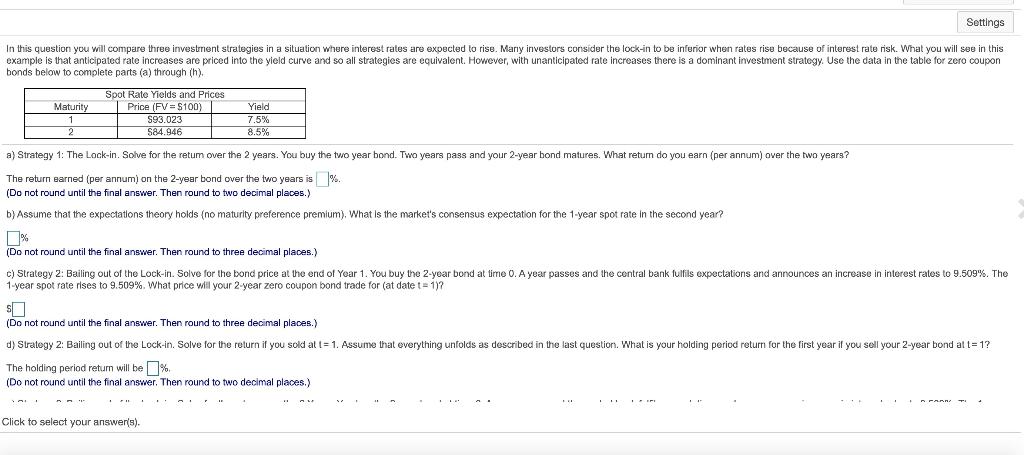

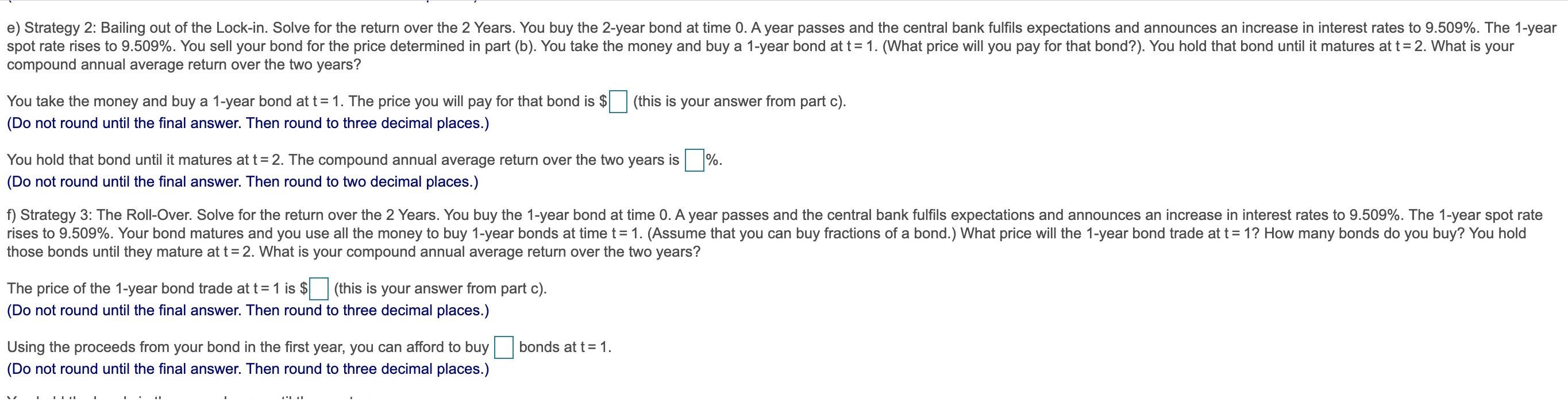

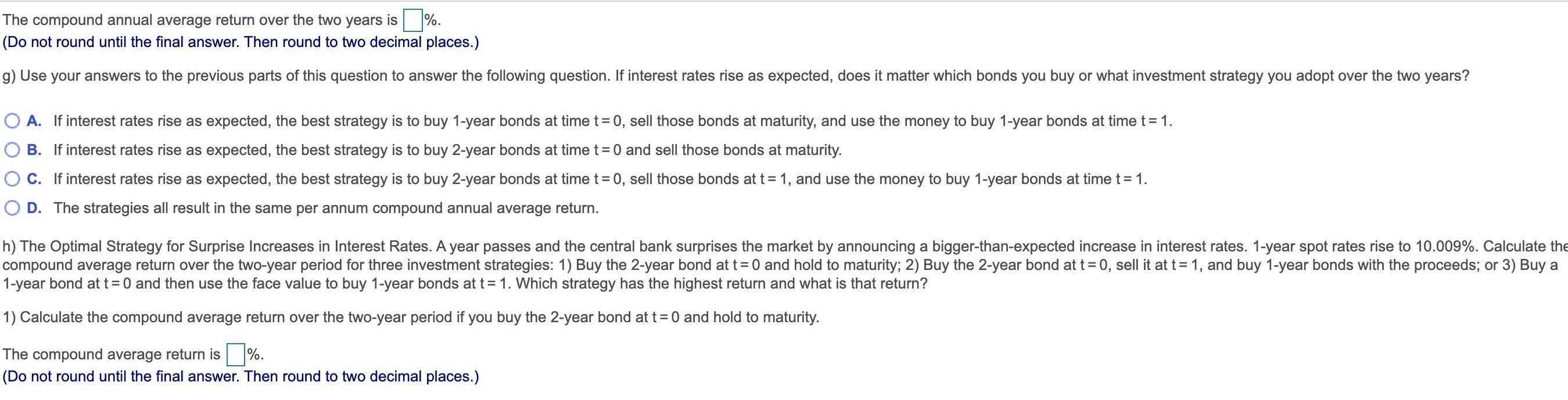

Settings In this question you will compare three investment strategies in a situation where interest rates are expected to rise. Many investors consider lock-in to be inferior when rates rise because of interest rate risk. What you will see in this example is that anticipated rate increases are priced into the yield curve and so all strategies are equivalent. However, with unanticipated rate increases there is a dominant investment strategy. Use the data in the table for zero coupon bonds below to complete parts (a) through (h). Maturity Spot Rate Yields and Prices Price (FV-S100) $93.023 584.946 Yield 7.5% 8.5% a) Strategy 1: The Lock-in. Solve for the retum over the 2 years. You buy the two year bond. Two years pass and your 2-year bond matures. What return do you earn (per annum) over the two years? The return earned (per annum) on the 2-year bond over the two years is % (Do not round until the final answer. Then round to two decimal places.) b) Assume that the expectations theory holds (no maturity preference premium), What is the market's consensus expectation for the 1-year spot rate in the second year? (Do not round until the final answer. Then round to three decimal places.) c) Strategy 2: Bailing out of the Lock-in. Solve for the bond price at the end of Year 1. You buy the 2-year bond at time 0. A year passes and the contral bank fulfils expectations and announces an increase in interest rates to 9.509%. The 1-year spot rate rises to 9.509% What price will your 2-year zero coupon bond trade for (at date t = 1/2 (Do not round until the final answer. Then round to three decimal places.) d) Strategy 2. Bailing out of the Lock-in. Solve for the return if you sold at t= 1. Assume that everything unfolds as described in the last question. What is your holding period return for the first year if you sell your 2-year bond at t= 1? The holding period retum will be % (Do not round until the final answer. Then round to two decimal places.) Click select your answer(s). e) Strategy 2: Bailing out of the Lock-in. Solve for the return over the 2 Years. You buy the 2-year bond at time 0. A year passes and the central bank fulfils expectations and announces an increase in interest rates to 9.509%. The 1-year spot rate rises to 9.509%. You sell your bond for the price determined in part (b). You take the money and buy a 1-year bond at t= 1. (What price will you pay for that bond?). You hold that bond until it matures at t = 2. What is your compound annual average return over the two years? You take the money and buy a 1-year bond at t= 1. The price you will pay for that bond is $ (this is your answer from part c). (Do not round until the final answer. Then round to three decimal places.) You hold that bond until it matures at t=2. The compound annual average return over the two years is %. (Do not round until the final answer. Then round to two decimal places.) f) Strategy 3: The Roll-Over. Solve for the return over the 2 Years. You buy the 1-year bond at time 0. A year passes and the central bank fulfils expectations and announces an increase in interest rates to 9.509%. The 1-year spot rate rises to 9.509%. Your bond matures and you use all the money to buy 1-year bonds at time t= 1. (Assume that you can buy fractions of a bond.) What price will the 1-year bond trade at t = 1? How many bonds do you buy? You hold those bonds until they mature at t = 2. What is your compound annual average return over the two years? The price of the 1-year bond trade at t= 1 is $(this is your answer from part c). (Do not round until the final answer. Then round to three decimal places.) bonds at t= 1. Using the proceeds from your bond in the first year, you can afford to buy (Do not round until the final answer. Then round to three decimal places.) The compound annual average return over the two years is %. (Do not round until the final answer. Then round to two decimal places.) g) Use your answers to the previous parts of this question to answer the following question. If interest rates rise as expected, does it matter which bonds you buy or what investment strategy you adopt over the two years? A. If interest rates rise as expected, the best strategy is to buy 1-year bonds at time t = 0, sell those bonds at maturity, and use the money to buy 1-year bonds at time t = 1. B. If interest rates rise as expected, the best strategy is to buy 2-year bonds at time t = 0 and sell those bonds at maturity. O C. If interest rates rise as expected, the best strategy is to buy 2-year bonds at time t= 0, sell those bonds at t = 1, and use the money to buy 1-year bonds at time t = 1. OD. The strategies all result in the same per annum compound annual average return. h) The Optimal Strategy for Surprise Increases in Interest Rates. A year passes and the central bank surprises the market by announcing a bigger-than-expected increase in interest rates. 1-year spot rates rise to 10.009%. Calculate the compound average return over the two-year period for three investment strategies: 1) Buy the 2-year bond at t= 0 and hold to maturity; 2) Buy the 2-year bond at t=0, sell it at t= 1, and buy 1-year bonds with the proceeds; or 3) Buy a 1-year bond at t= 0 and then use the face value to buy 1-year bonds at t= 1. Which strategy has the highest return and what is that return? 1) Calculate the compound average return over the two-year period if you buy the 2-year bond at t= 0 and hold to maturity. The compound average return is %. (Do not round until the final answer. Then round to two decimal places.) The compound average return is %. (Do not round until the final answer. Then round to two decimal places.) 2) Calculate the compound average return over the two-year period if you buy the 2-year bond at t= 0, sell it at t= 1, and buy 1-year bonds with the proceeds. The compound average return is %. (Do not round until the final answer. Then round to two decimal places.) 3) Calculate the compound average return over the two-year period if you buy a 1-year bond at t= 0 and then use the face value to buy 1-year bonds at t= 1. The compound average return is %. (Do not round until the final answer. Then round to two decimal places.) Which strategy has the highest return? O A. Strategy 1 B. Strategy 2 C. Strategy 3 D. The strategies all result in the same compound annual average return. Settings In this question you will compare three investment strategies in a situation where interest rates are expected to rise. Many investors consider lock-in to be inferior when rates rise because of interest rate risk. What you will see in this example is that anticipated rate increases are priced into the yield curve and so all strategies are equivalent. However, with unanticipated rate increases there is a dominant investment strategy. Use the data in the table for zero coupon bonds below to complete parts (a) through (h). Maturity Spot Rate Yields and Prices Price (FV-S100) $93.023 584.946 Yield 7.5% 8.5% a) Strategy 1: The Lock-in. Solve for the retum over the 2 years. You buy the two year bond. Two years pass and your 2-year bond matures. What return do you earn (per annum) over the two years? The return earned (per annum) on the 2-year bond over the two years is % (Do not round until the final answer. Then round to two decimal places.) b) Assume that the expectations theory holds (no maturity preference premium), What is the market's consensus expectation for the 1-year spot rate in the second year? (Do not round until the final answer. Then round to three decimal places.) c) Strategy 2: Bailing out of the Lock-in. Solve for the bond price at the end of Year 1. You buy the 2-year bond at time 0. A year passes and the contral bank fulfils expectations and announces an increase in interest rates to 9.509%. The 1-year spot rate rises to 9.509% What price will your 2-year zero coupon bond trade for (at date t = 1/2 (Do not round until the final answer. Then round to three decimal places.) d) Strategy 2. Bailing out of the Lock-in. Solve for the return if you sold at t= 1. Assume that everything unfolds as described in the last question. What is your holding period return for the first year if you sell your 2-year bond at t= 1? The holding period retum will be % (Do not round until the final answer. Then round to two decimal places.) Click select your answer(s). e) Strategy 2: Bailing out of the Lock-in. Solve for the return over the 2 Years. You buy the 2-year bond at time 0. A year passes and the central bank fulfils expectations and announces an increase in interest rates to 9.509%. The 1-year spot rate rises to 9.509%. You sell your bond for the price determined in part (b). You take the money and buy a 1-year bond at t= 1. (What price will you pay for that bond?). You hold that bond until it matures at t = 2. What is your compound annual average return over the two years? You take the money and buy a 1-year bond at t= 1. The price you will pay for that bond is $ (this is your answer from part c). (Do not round until the final answer. Then round to three decimal places.) You hold that bond until it matures at t=2. The compound annual average return over the two years is %. (Do not round until the final answer. Then round to two decimal places.) f) Strategy 3: The Roll-Over. Solve for the return over the 2 Years. You buy the 1-year bond at time 0. A year passes and the central bank fulfils expectations and announces an increase in interest rates to 9.509%. The 1-year spot rate rises to 9.509%. Your bond matures and you use all the money to buy 1-year bonds at time t= 1. (Assume that you can buy fractions of a bond.) What price will the 1-year bond trade at t = 1? How many bonds do you buy? You hold those bonds until they mature at t = 2. What is your compound annual average return over the two years? The price of the 1-year bond trade at t= 1 is $(this is your answer from part c). (Do not round until the final answer. Then round to three decimal places.) bonds at t= 1. Using the proceeds from your bond in the first year, you can afford to buy (Do not round until the final answer. Then round to three decimal places.) The compound annual average return over the two years is %. (Do not round until the final answer. Then round to two decimal places.) g) Use your answers to the previous parts of this question to answer the following question. If interest rates rise as expected, does it matter which bonds you buy or what investment strategy you adopt over the two years? A. If interest rates rise as expected, the best strategy is to buy 1-year bonds at time t = 0, sell those bonds at maturity, and use the money to buy 1-year bonds at time t = 1. B. If interest rates rise as expected, the best strategy is to buy 2-year bonds at time t = 0 and sell those bonds at maturity. O C. If interest rates rise as expected, the best strategy is to buy 2-year bonds at time t= 0, sell those bonds at t = 1, and use the money to buy 1-year bonds at time t = 1. OD. The strategies all result in the same per annum compound annual average return. h) The Optimal Strategy for Surprise Increases in Interest Rates. A year passes and the central bank surprises the market by announcing a bigger-than-expected increase in interest rates. 1-year spot rates rise to 10.009%. Calculate the compound average return over the two-year period for three investment strategies: 1) Buy the 2-year bond at t= 0 and hold to maturity; 2) Buy the 2-year bond at t=0, sell it at t= 1, and buy 1-year bonds with the proceeds; or 3) Buy a 1-year bond at t= 0 and then use the face value to buy 1-year bonds at t= 1. Which strategy has the highest return and what is that return? 1) Calculate the compound average return over the two-year period if you buy the 2-year bond at t= 0 and hold to maturity. The compound average return is %. (Do not round until the final answer. Then round to two decimal places.) The compound average return is %. (Do not round until the final answer. Then round to two decimal places.) 2) Calculate the compound average return over the two-year period if you buy the 2-year bond at t= 0, sell it at t= 1, and buy 1-year bonds with the proceeds. The compound average return is %. (Do not round until the final answer. Then round to two decimal places.) 3) Calculate the compound average return over the two-year period if you buy a 1-year bond at t= 0 and then use the face value to buy 1-year bonds at t= 1. The compound average return is %. (Do not round until the final answer. Then round to two decimal places.) Which strategy has the highest return? O A. Strategy 1 B. Strategy 2 C. Strategy 3 D. The strategies all result in the same compound annual average return