Question

Please write type the answer by computer, so that i can see this clearly, thank you An investment manager forecasts the 1 year Treasury bill

Please write type the answer by computer, so that i can see this clearly, thank you

An investment manager forecasts the 1 year Treasury bill rate (short-term rate) for the next four years in the following table:

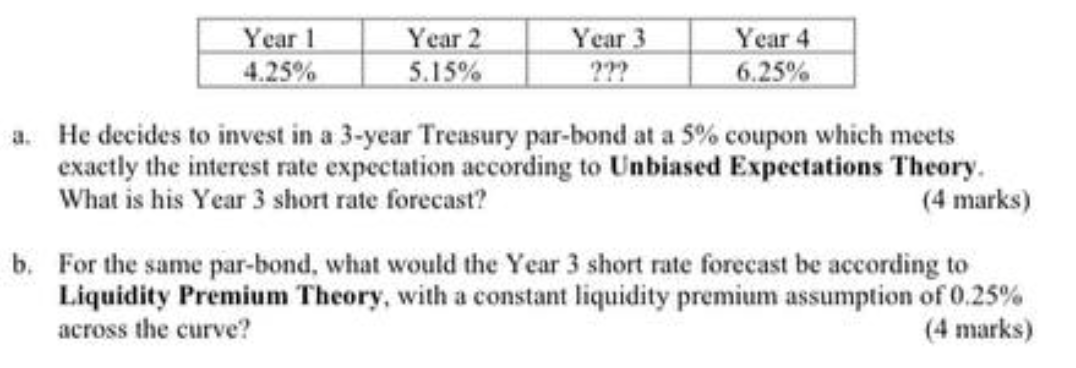

Year 3 Year 1 4.25% Year 2 5.15% Year 4 6.25% a. He decides to invest in a 3-year Treasury par-bond at a 5% coupon which meets exactly the interest rate expectation according to Unbiased Expectations Theory. What is his Year 3 short rate forecast? (4 marks) b. For the same par-bond, what would the Year 3 short rate forecast be according to Liquidity Premium Theory, with a constant liquidity premium assumption of 0.25% across the curve? (4 marks) Year 3 Year 1 4.25% Year 2 5.15% Year 4 6.25% a. He decides to invest in a 3-year Treasury par-bond at a 5% coupon which meets exactly the interest rate expectation according to Unbiased Expectations Theory. What is his Year 3 short rate forecast? (4 marks) b. For the same par-bond, what would the Year 3 short rate forecast be according to Liquidity Premium Theory, with a constant liquidity premium assumption of 0.25% across the curve? (4 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance

Authors: E. Thomas Garman, Raymond Forgue

9th Edition

0618938737, 978-0618938735