pls answers 10-18 tysm

income taxation

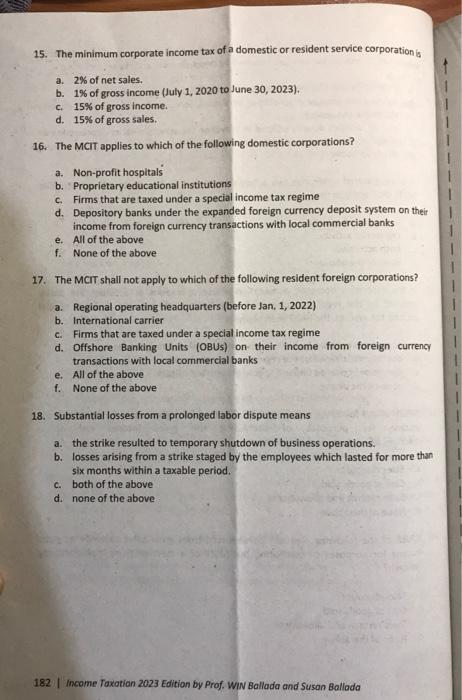

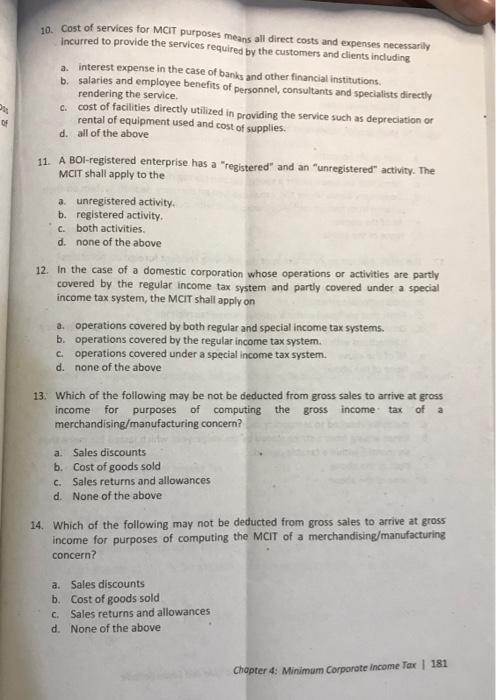

10. Cost of services for MCIT purposes means all direct costs and expenses necessarily incurred to provide the services required by the customers and clients including. a. interest expense in the case of banks and other financial institutions. b. salaries and employee benefits of personnel, consultants and specialists directly rendering the service. c. cost of facilities directly utilized in providing the service such as depreciation or rental of equipment used and cost of supplies. d. all of the above 11. A BOI-registered enterprise has a "registered" and an "unregistered" activity. The MCIT shall apply to the 3. unregistered activity. b. registered activity. c. both activities. d. none of the above 12. In the case of a domestic corporation whose operations or activities are partly covered by the regular income tax system and partly covered under a special income tax system, the MCIT shall apply on a. operations covered by both regular and special income tax systems. b. operations covered by the regular income tax system. c. operations covered under a special income tax system. d. none of the above 13. Which of the following may be not be deducted from gross sales to arrive at gross income for purposes of computing the gross income tax of a merchandising/manufacturing concern? a. Sales discounts b. Cost of goods sold c. Sales returns and allowances d. None of the above 14. Which of the following may not be deducted from gross sales to arrive at gross income for purposes of computing the MCiT of a merchandising/manufacturing concern? a. Sales discounts b. Cost of goods sold c. Sales returns and allowances d. None of the above 15. The minimum corporate income tax of a domestic or resident service corporation is a. 2% of net sales. b. 1% of gross income (July 1, 2020 to June 30,2023 ). c. 15% of gross income. d. 15% of gross sales. 16. The MCIT applies to which of the following domestic corporations? a. Non-profit hospitals b. Proprietary educational institutions c. Firms that are taxed under a special income tax regime d. Depository banks under the expanded foreign currency deposit system on their income from foreign currency transactions with local commercial banks e. All of the above f. None of the above 17. The MCIT shall not apply to which of the following resident foreign corporations? a. Regional operating headquarters (before Jan, 1, 2022) b. International carrier c. Firms that are taxed under a special income tax regime d. Offshore Banking Units (OBUs) on their income from foreign currency transactions with local commercial banks e. All of the above f. None of the above 18. Substantial losses from a prolonged labor dispute means a. the strike resulted to temporary shutdown of business operations. b. losses arising from a strike staged by the employees which lasted for more than six months within a taxable period. c. both of the above d. none of the above 182 I Income Taxatian 2023 Edition by Prof. WIN Ballada and Susan Ballada 10. Cost of services for MCIT purposes means all direct costs and expenses necessarily incurred to provide the services required by the customers and clients including. a. interest expense in the case of banks and other financial institutions. b. salaries and employee benefits of personnel, consultants and specialists directly rendering the service. c. cost of facilities directly utilized in providing the service such as depreciation or rental of equipment used and cost of supplies. d. all of the above 11. A BOI-registered enterprise has a "registered" and an "unregistered" activity. The MCIT shall apply to the 3. unregistered activity. b. registered activity. c. both activities. d. none of the above 12. In the case of a domestic corporation whose operations or activities are partly covered by the regular income tax system and partly covered under a special income tax system, the MCIT shall apply on a. operations covered by both regular and special income tax systems. b. operations covered by the regular income tax system. c. operations covered under a special income tax system. d. none of the above 13. Which of the following may be not be deducted from gross sales to arrive at gross income for purposes of computing the gross income tax of a merchandising/manufacturing concern? a. Sales discounts b. Cost of goods sold c. Sales returns and allowances d. None of the above 14. Which of the following may not be deducted from gross sales to arrive at gross income for purposes of computing the MCiT of a merchandising/manufacturing concern? a. Sales discounts b. Cost of goods sold c. Sales returns and allowances d. None of the above 15. The minimum corporate income tax of a domestic or resident service corporation is a. 2% of net sales. b. 1% of gross income (July 1, 2020 to June 30,2023 ). c. 15% of gross income. d. 15% of gross sales. 16. The MCIT applies to which of the following domestic corporations? a. Non-profit hospitals b. Proprietary educational institutions c. Firms that are taxed under a special income tax regime d. Depository banks under the expanded foreign currency deposit system on their income from foreign currency transactions with local commercial banks e. All of the above f. None of the above 17. The MCIT shall not apply to which of the following resident foreign corporations? a. Regional operating headquarters (before Jan, 1, 2022) b. International carrier c. Firms that are taxed under a special income tax regime d. Offshore Banking Units (OBUs) on their income from foreign currency transactions with local commercial banks e. All of the above f. None of the above 18. Substantial losses from a prolonged labor dispute means a. the strike resulted to temporary shutdown of business operations. b. losses arising from a strike staged by the employees which lasted for more than six months within a taxable period. c. both of the above d. none of the above 182 I Income Taxatian 2023 Edition by Prof. WIN Ballada and Susan Ballada