pls help me the steps to calculate these question !

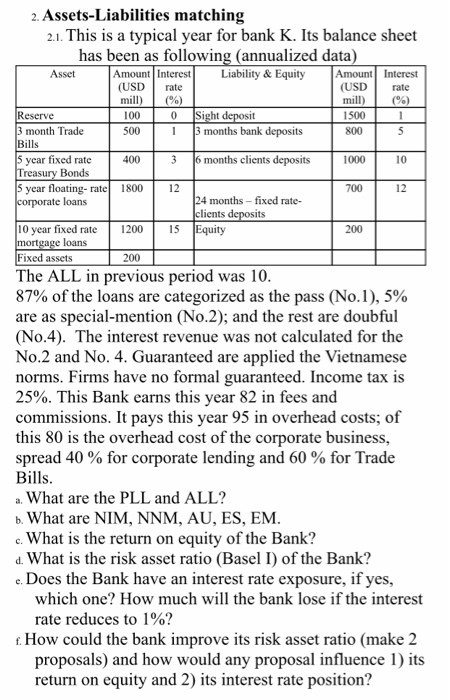

mill) (%) Reserve 31 31 2. Assets-Liabilities matching 2.1. This is a typical year for bank K. Its balance sheet has been as following (annualized data) Asset Amount Interest Liability & Equity Amount Interest (USD rate (USD rate mill) (9) 1000 Sight deposit 1500 3 month Trade 500 months bank deposits 800 Bills 5 year fixed rate 400 3 6 months clients deposits 1000 Treasury Bonds s year floating-rate 1800 corporate loans 24 months - fixed rate- clients deposits 10 year fixed rate 1200 15 Equity mortgage loans Fixed assets 1200 The ALL in previous period was 10. 87% of the loans are categorized as the pass (No.1), 5% are as special mention (No.2); and the rest are doubful (No.4). The interest revenue was not calculated for the No.2 and No. 4. Guaranteed are applied the Vietnamese norms. Firms have no formal guaranteed. Income tax is 25%. This Bank earns this year 82 in fees and commissions. It pays this year 95 in overhead costs; of this 80 is the overhead cost of the corporate business, spread 40 % for corporate lending and 60 % for Trade Bills. a. What are the PLL and ALL? b. What are NIM, NNM, AU, ES, EM. c. What is the return on equity of the Bank? d. What is the risk asset ratio (Basel I) of the Bank? c. Does the Bank have an interest rate exposure, if yes, which one? How much will the bank lose if the interest rate reduces to 1%? How could the bank improve its risk asset ratio (make 2 proposals) and how would any proposal influence 1) its return on equity and 2) its interest rate position? mill) (%) Reserve 31 31 2. Assets-Liabilities matching 2.1. This is a typical year for bank K. Its balance sheet has been as following (annualized data) Asset Amount Interest Liability & Equity Amount Interest (USD rate (USD rate mill) (9) 1000 Sight deposit 1500 3 month Trade 500 months bank deposits 800 Bills 5 year fixed rate 400 3 6 months clients deposits 1000 Treasury Bonds s year floating-rate 1800 corporate loans 24 months - fixed rate- clients deposits 10 year fixed rate 1200 15 Equity mortgage loans Fixed assets 1200 The ALL in previous period was 10. 87% of the loans are categorized as the pass (No.1), 5% are as special mention (No.2); and the rest are doubful (No.4). The interest revenue was not calculated for the No.2 and No. 4. Guaranteed are applied the Vietnamese norms. Firms have no formal guaranteed. Income tax is 25%. This Bank earns this year 82 in fees and commissions. It pays this year 95 in overhead costs; of this 80 is the overhead cost of the corporate business, spread 40 % for corporate lending and 60 % for Trade Bills. a. What are the PLL and ALL? b. What are NIM, NNM, AU, ES, EM. c. What is the return on equity of the Bank? d. What is the risk asset ratio (Basel I) of the Bank? c. Does the Bank have an interest rate exposure, if yes, which one? How much will the bank lose if the interest rate reduces to 1%? How could the bank improve its risk asset ratio (make 2 proposals) and how would any proposal influence 1) its return on equity and 2) its interest rate position