Answered step by step

Verified Expert Solution

Question

1 Approved Answer

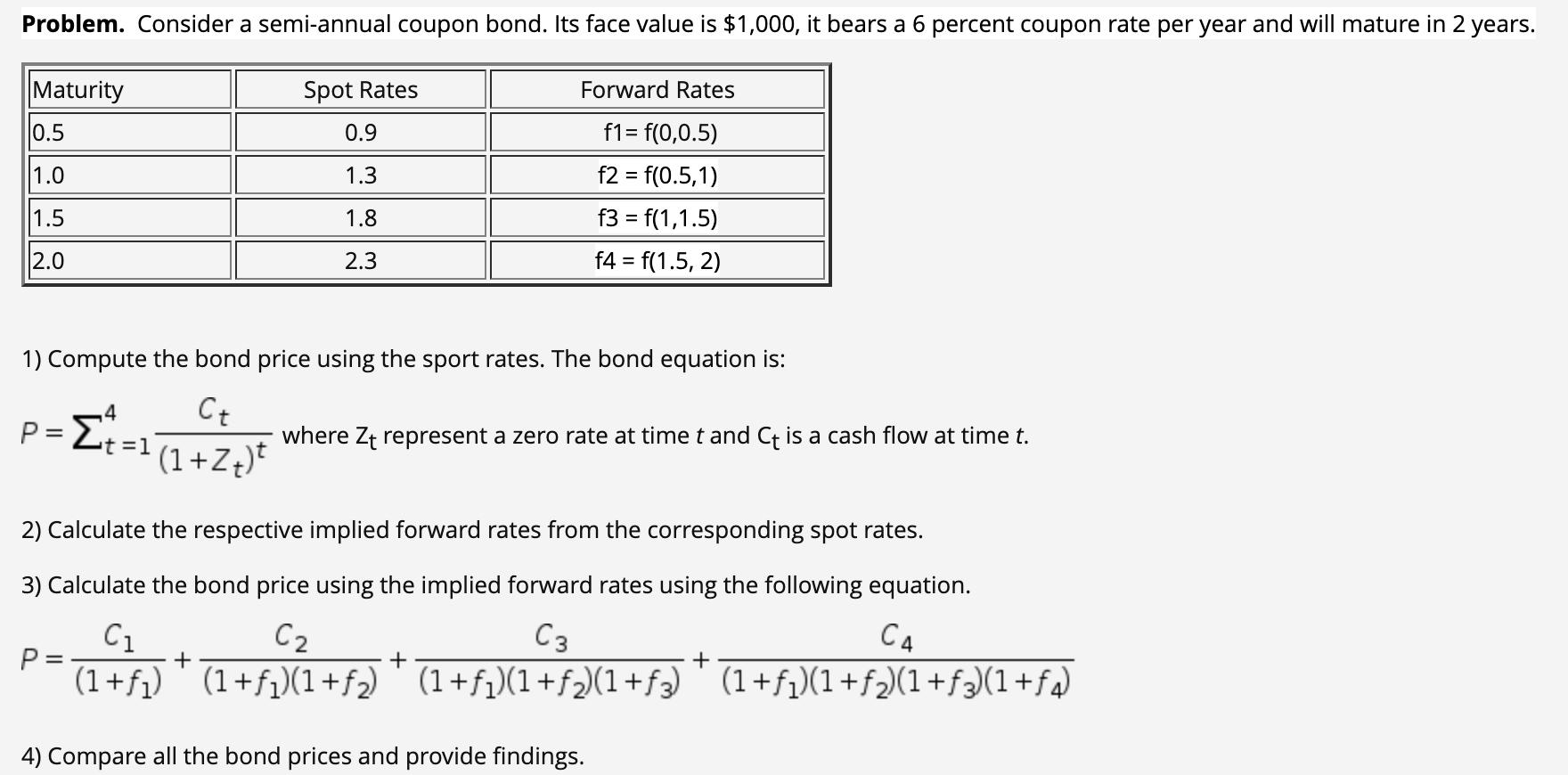

Problem. Consider a semi-annual coupon bond. Its face value is $1,000, it bears a 6 percent coupon rate per year and will mature in

Problem. Consider a semi-annual coupon bond. Its face value is $1,000, it bears a 6 percent coupon rate per year and will mature in 2 years. Maturity 0.5 1.0 1.5 2.0 Spot Rates 0.9 1.3 1.8 2.3 Forward Rates f1= f(0,0.5) f2 = f(0.5,1) f3 = f(1,1.5) f4 = f(1.5, 2) 1) Compute the bond price using the sport rates. The bond equation is: 4 Ct P = t = 1 (1 + Z) where Zt represent a zero rate at time t and Ct is a cash flow at time t. t P= 2) Calculate the respective implied forward rates from the corresponding spot rates. 3) Calculate the bond price using the implied forward rates using the following equation. C C3 C4 (1+f)(1+f) (1+f)(1+f)(1+f3) (1+f)(1 + f)(1+f3)(1+fa) C * * * + (1+f) 4) Compare all the bond prices and provide findings.

Step by Step Solution

★★★★★

3.42 Rating (152 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Project Management A Managerial Approach

Authors: Jack R. Meredith, Samuel J. Mantel,

7th Edition

470226218, 978-0470226216