Answered step by step

Verified Expert Solution

Question

1 Approved Answer

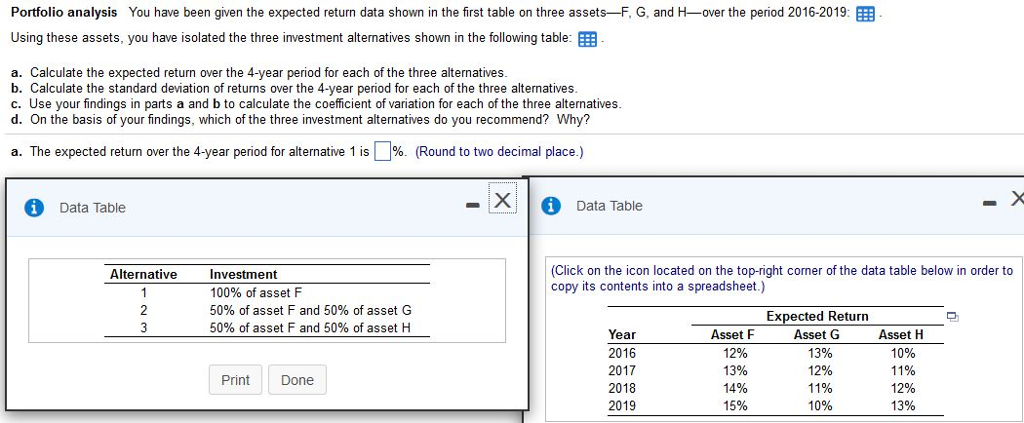

Portfolio analysis You have been given the expected return data shown in the first table on three assets-F, G. and H-over the period 2016-2019: Using

Portfolio analysis You have been given the expected return data shown in the first table on three assets-F, G. and H-over the period 2016-2019: Using these assets, you have isolated the three investment alternatives shown in the following table: EEB a. Calculate the expected return over the 4-year period for each of the three alternatives b. Calculate the standard deviation of returns over the 4-year period for each of the three alternatives c. Use your findings in parts a and b to calculate the coefficient of variation for each of the three alternatives d. On the basis of your findings, which of the three investment alternatives do you recommend? Why? %. (Round to two decimal place.) a. The expected return over the 4-year period for alternative 1 is X?O Data Table i Data Table (Click on the icon located on the top-right cormer of the data table below in order to copy its contents into a spreadsheet.) Investment 100% of asset F 50% of asset F and 50% of asset G 50% of asset F and 50% of asset H Alternative Year 2016 2017 2018 2019 Asset F 12% 1396 14% 15% Expected Return Asset G 13% 1296 11% 10% Asset H 10% 11% 12% 13% Print Done

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Bitcoin

Authors: Robert P. Murphy ,Silas Barta

1st Edition

1505819784, 978-1505819786