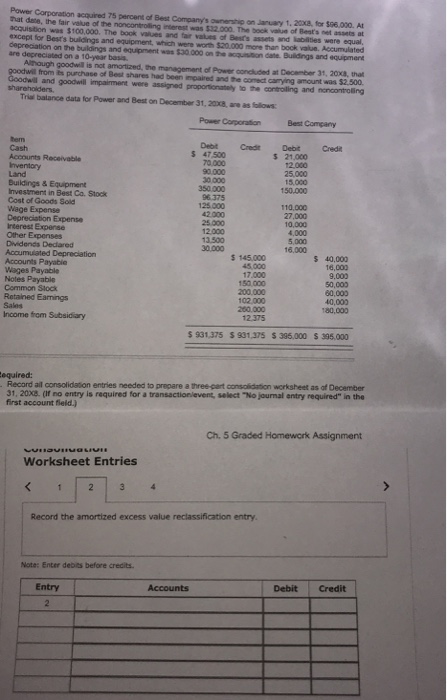

Power Corporation acquired 75 percent of Best Company's ownership on January 1. 20ox8, for $96.000. A hat date, the fair value of the noncontroling interest was $32000. The book value of Beat's net assets at acquisition was $100,000. The book values and fair values of Bests assets and labilites were equal, except for Best's buldings and equipment, which were worth $20.000 more than book value. Accumulated Geprecation on the buildings and equipment was $30.000 on the qusition cate Buildings and equipment are depreciated on a 10-year basa Although goodwill is not amortized, the management of Power concluded at Cecmber 31, 2oxa, that from its purchase of Best shares had been impaired and the comect carying amount was $2.500 and goodwill impairment were assigned proportionately to the controlling and ncncontroling Trial balance data for Power and Best on December 31, 20x8, are as follows Power CorporationBest Company S 47.500 70.000 90.000 0,000 350.000 96 375 125.000 42.000 s 21,000 12.000 25,000 15,000 150.000 Accounts Receivable Inventory Buildings & Equipment Investment in Best Co. Stock Cost of Goods Sold Wage Expense Depreciation Expense Interest Expense Other Expenses Dividends Dedared 110,000 27,000 10,000 4,000 5,000 16.000 13.500 Accounts Payable Wages Payable Notes Payable Common Slock Retained Eanings $ 145000 45,000 17.000 150 000 200.000 102.000 200.000 12.375 5 40,000 16,000 9.000 50,000 60,000 40,000 Income from Subsidiary $ 931 375 $ 931 375 $ 395,000 $ 395.000 Record all consolidation entries needed to prepare a three-part consolidation worksheet as of December 31, 20x3. (If no entry is required for a transactionlevent, select "No journal antry required" in the first account field.) C. 5 Graded Homework Assignment Worksheet Entries Record the amortized excess value reclassification entry Note: Enter debits before crecits. Entry Accounts Debit Credit Power Corporation acquired 75 percent of Best Company's ownership on January 1. 20ox8, for $96.000. A hat date, the fair value of the noncontroling interest was $32000. The book value of Beat's net assets at acquisition was $100,000. The book values and fair values of Bests assets and labilites were equal, except for Best's buldings and equipment, which were worth $20.000 more than book value. Accumulated Geprecation on the buildings and equipment was $30.000 on the qusition cate Buildings and equipment are depreciated on a 10-year basa Although goodwill is not amortized, the management of Power concluded at Cecmber 31, 2oxa, that from its purchase of Best shares had been impaired and the comect carying amount was $2.500 and goodwill impairment were assigned proportionately to the controlling and ncncontroling Trial balance data for Power and Best on December 31, 20x8, are as follows Power CorporationBest Company S 47.500 70.000 90.000 0,000 350.000 96 375 125.000 42.000 s 21,000 12.000 25,000 15,000 150.000 Accounts Receivable Inventory Buildings & Equipment Investment in Best Co. Stock Cost of Goods Sold Wage Expense Depreciation Expense Interest Expense Other Expenses Dividends Dedared 110,000 27,000 10,000 4,000 5,000 16.000 13.500 Accounts Payable Wages Payable Notes Payable Common Slock Retained Eanings $ 145000 45,000 17.000 150 000 200.000 102.000 200.000 12.375 5 40,000 16,000 9.000 50,000 60,000 40,000 Income from Subsidiary $ 931 375 $ 931 375 $ 395,000 $ 395.000 Record all consolidation entries needed to prepare a three-part consolidation worksheet as of December 31, 20x3. (If no entry is required for a transactionlevent, select "No journal antry required" in the first account field.) C. 5 Graded Homework Assignment Worksheet Entries Record the amortized excess value reclassification entry Note: Enter debits before crecits. Entry Accounts Debit Credit