Answered step by step

Verified Expert Solution

Question

1 Approved Answer

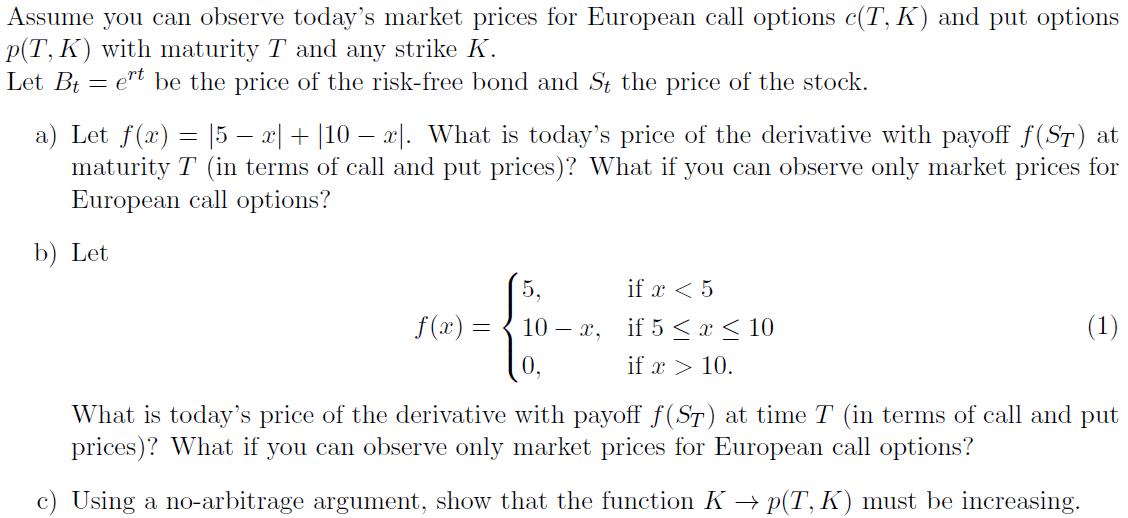

Assume you can observe today's market prices for European call options c(T, K) and put options p(T, K) with maturity T and any strike

Assume you can observe today's market prices for European call options c(T, K) and put options p(T, K) with maturity T and any strike K. Let Bt ert be the price of the risk-free bond and St the price of the stock. - - a) Let f(x) = |5 x| + |10 x]. What is today's price of the derivative with payoff (ST) at maturity T (in terms of call and put prices)? What if you can observe only market prices for European call options? b) Let 5, if x < 5 f(x) = 10-x, if 5 x 10 if x > 10. (1) What is today's price of the derivative with payoff f(ST) at time T (in terms of call and put prices)? What if you can observe only market prices for European call options? c) Using a no-arbitrage argument, show that the function K p(T, K) must be increasing.

Step by Step Solution

★★★★★

3.42 Rating (171 Votes )

There are 3 Steps involved in it

Step: 1

Solution Let Br e be the price of the risk free ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles of Managerial Finance

Authors: Lawrence J. Gitman, Chad J. Zutter

14th edition

133507696, 978-0133507690