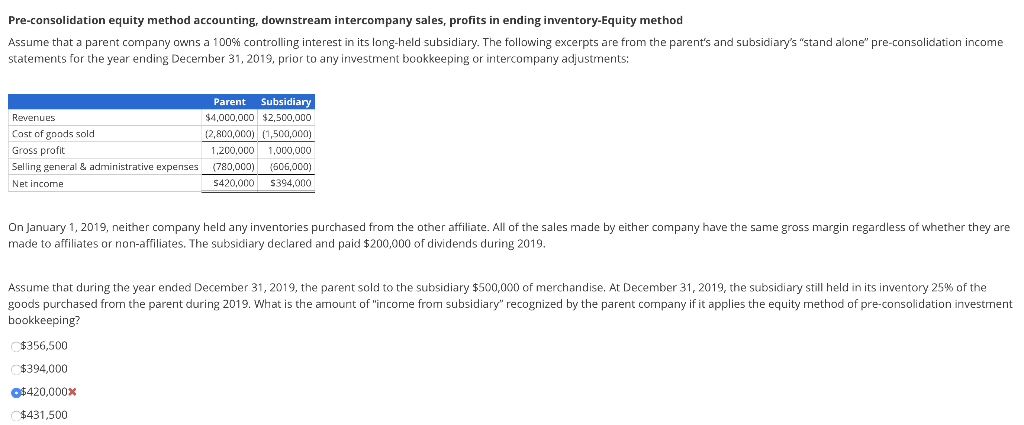

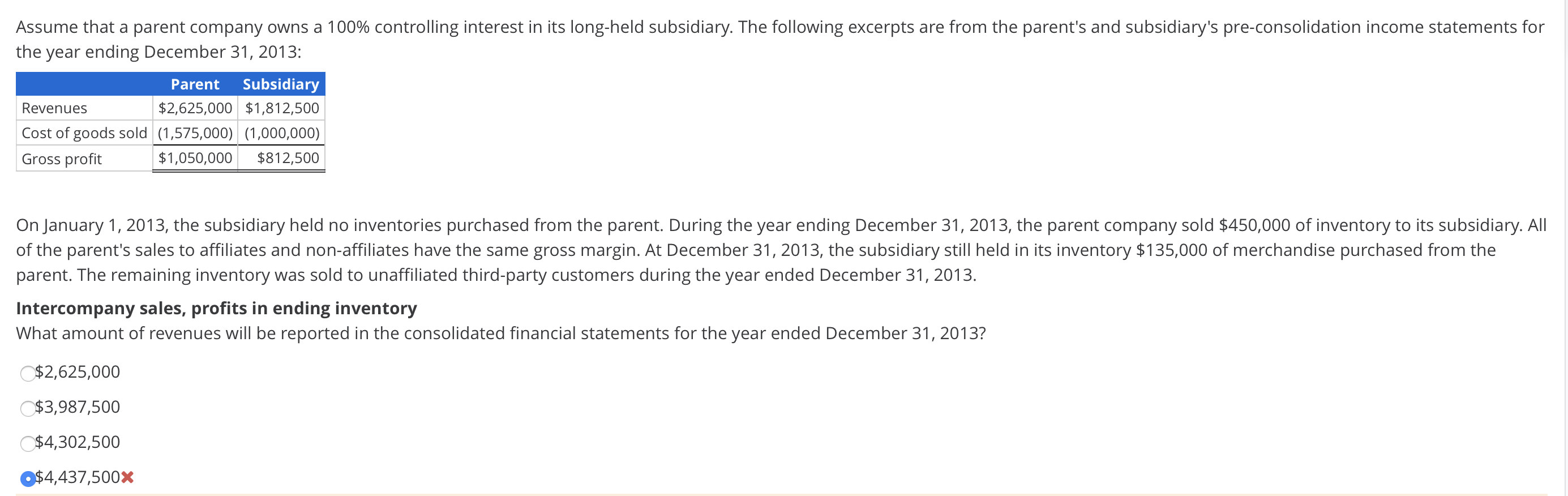

Pre-consolidation equity method accounting, downstream intercompany sales, profits in ending inventory-Equity method Assume that a parent company owns a 100% controlling interest in its long-held subsidiary. The following excerpts are from the parent's and subsidiary's "stand alone" pre-consolidation income statements for the year ending December 31, 2019, prior to any investment bookkeeping or intercompany adjustments: Revenues Cost of goods sold Gross profit Selling general & administrative expenses Net income Parent Subsidiary $4,000,000 $2,500,000 (2,800,000) (1,500,000) 1,200,000 1,000,000 (780,000) (606,000) 5420,000 $394,000 On January 1, 2019, neither company held any inventories purchased from the other affiliate. All of the sales made by either company have the same gross margin regardless of whether they are made to affiliates or non-affiliates. The subsidiary declared and paid $200,000 of dividends during 2019, Assume that during the year ended December 31, 2019, the parent sold to the subsidiary $500,000 of merchandise. At December 31, 2019, the subsidiary still held in its inventory 25% of the goods purchased from the parent during 2019. What is the amount of "income from subsidiary" recognized by the parent company if it applies the equity method of pre-consolidation investment bookkeeping? $356,500 $394,000 $420,000x $431,500 Assume that a parent company owns a 100% controlling interest in its long-held subsidiary. The following excerpts are from the parent's and subsidiary's pre-consolidation income statements for the year ending December 31, 2013: Parent Subsidiary Revenues $2,625,000 $1,812,500 Cost of goods sold (1,575,000) (1,000,000) Gross profit $1,050,000 $812,500 On January 1, 2013, the subsidiary held no inventories purchased from the parent. During the year ending December 31, 2013, the parent company sold $450,000 of inventory to its subsidiary. All of the parent's sales to affiliates and non-affiliates have the same gross margin. At December 31, 2013, the subsidiary still held in its inventory $135,000 of merchandise purchased from the parent. The remaining inventory was sold to unaffiliated third-party customers during the year ended December 31, 2013. Intercompany sales, profits in ending inventory What amount of revenues will be reported in the consolidated financial statements for the year ended December 31, 2013? $2,625,000 $3,987,500 $4,302,500 O$4,437,500X Pre-consolidation equity method accounting, downstream intercompany sales, profits in ending inventory-Equity method Assume that a parent company owns a 100% controlling interest in its long-held subsidiary. The following excerpts are from the parent's and subsidiary's "stand alone" pre-consolidation income statements for the year ending December 31, 2019, prior to any investment bookkeeping or intercompany adjustments: Revenues Cost of goods sold Gross profit Selling general & administrative expenses Net income Parent Subsidiary $4,000,000 $2,500,000 (2,800,000) (1,500,000) 1,200,000 1,000,000 (780,000) (606,000) 5420,000 $394,000 On January 1, 2019, neither company held any inventories purchased from the other affiliate. All of the sales made by either company have the same gross margin regardless of whether they are made to affiliates or non-affiliates. The subsidiary declared and paid $200,000 of dividends during 2019, Assume that during the year ended December 31, 2019, the parent sold to the subsidiary $500,000 of merchandise. At December 31, 2019, the subsidiary still held in its inventory 25% of the goods purchased from the parent during 2019. What is the amount of "income from subsidiary" recognized by the parent company if it applies the equity method of pre-consolidation investment bookkeeping? $356,500 $394,000 $420,000x $431,500 Assume that a parent company owns a 100% controlling interest in its long-held subsidiary. The following excerpts are from the parent's and subsidiary's pre-consolidation income statements for the year ending December 31, 2013: Parent Subsidiary Revenues $2,625,000 $1,812,500 Cost of goods sold (1,575,000) (1,000,000) Gross profit $1,050,000 $812,500 On January 1, 2013, the subsidiary held no inventories purchased from the parent. During the year ending December 31, 2013, the parent company sold $450,000 of inventory to its subsidiary. All of the parent's sales to affiliates and non-affiliates have the same gross margin. At December 31, 2013, the subsidiary still held in its inventory $135,000 of merchandise purchased from the parent. The remaining inventory was sold to unaffiliated third-party customers during the year ended December 31, 2013. Intercompany sales, profits in ending inventory What amount of revenues will be reported in the consolidated financial statements for the year ended December 31, 2013? $2,625,000 $3,987,500 $4,302,500 O$4,437,500X