Question

Prepare a full process cost reports (including all five steps) for the Finishing Department for the month of April by using the weighted average method.

Prepare a full process cost reports (including all five steps) for the Finishing Department for the month of April by using the weighted average method. You need to calculate the net transferred in units and their related costs at the first inspection point before you start the first stage of process costing. Conversion costs equal direct labour costs plus overhead costs. So, you need to calculate the conversion costs for the period if it is not given.

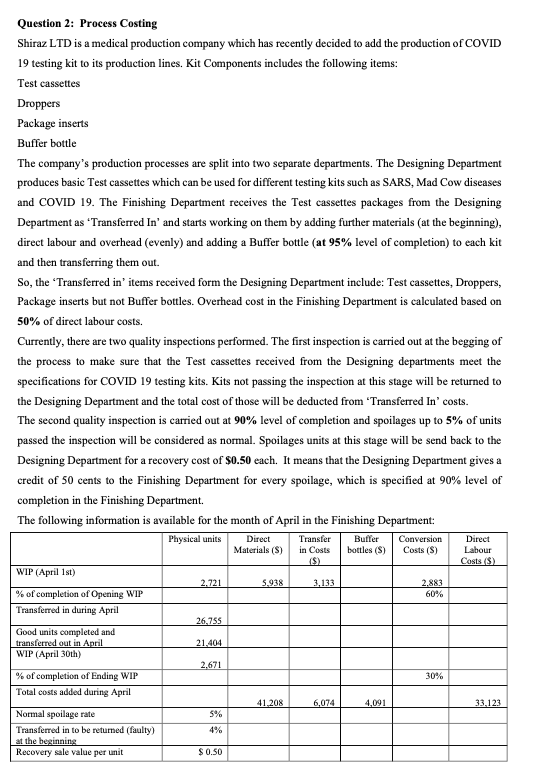

Question 2: Process Costing Shiraz LTD is a medical production company which has recently decided to add the production of COVID 19 testing kit to its production lines. Kit Components includes the following items: Test cassettes Droppers Package inserts Buffer bottle The company's production processes are split into two separate departments. The Designing Department produces basic Test cassettes which can be used for different testing kits such as SARS, Mad Cow diseases and COVID 19. The Finishing Department receives the Test cassettes packages from the Designing Department as 'Transferred In' and starts working on them by adding further materials (at the beginning), direct labour and overhead (evenly) and adding a Buffer bottle (at 95% level of completion) to each kit and then transferring them out. So, the 'Transferred in' items received form the Designing Department include: Test cassettes, Droppers, Package inserts but not Buffer bottles. Overhead cost in the Finishing Department is calculated based on 50% of direct labour costs. Currently, there are two quality inspections performed. The first inspection is carried out at the begging of the process to make sure that the Test cassettes received from the Designing departments meet the specifications for COVID 19 testing kits. Kits not passing the inspection at this stage will be returned to the Designing Department and the total cost of those will be deducted from 'Transferred In' costs. The second quality inspection is carried out at 90% level of completion and spoilages up to 5% of units passed the inspection will be considered as normal. Spoilages units at this stage will be send back to the Designing Department for a recovery cost of $0.50 each. It means that the Designing Department gives a credit of 50 cents to the Finishing Department for every spoilage, which is specified at 90% level of completion in the Finishing Department. The following information is available for the month of April in the Finishing Department: Physical units Direct Materials (S) Transfer in Costs Buffer bottles (S) Conversion Costs (S) Direct Labour Costs ($) 2.721 5.938 3,133 2.883 WIP (April 1st) % of completion of Opening WIP Transferred in during April 60% 26.755 Good units completed and transferred out in WIP (April 30th) 21.404 2.671 30% % of completion of Ending WIP Total costs added during April 41.208 6,074 4,091 33,123 5% Normal spoilage rate Transferred in to be retumed (faulty) at the beginning Recovery sale value per unit $ 0.50 Question 2: Process Costing Shiraz LTD is a medical production company which has recently decided to add the production of COVID 19 testing kit to its production lines. Kit Components includes the following items: Test cassettes Droppers Package inserts Buffer bottle The company's production processes are split into two separate departments. The Designing Department produces basic Test cassettes which can be used for different testing kits such as SARS, Mad Cow diseases and COVID 19. The Finishing Department receives the Test cassettes packages from the Designing Department as 'Transferred In' and starts working on them by adding further materials (at the beginning), direct labour and overhead (evenly) and adding a Buffer bottle (at 95% level of completion) to each kit and then transferring them out. So, the 'Transferred in' items received form the Designing Department include: Test cassettes, Droppers, Package inserts but not Buffer bottles. Overhead cost in the Finishing Department is calculated based on 50% of direct labour costs. Currently, there are two quality inspections performed. The first inspection is carried out at the begging of the process to make sure that the Test cassettes received from the Designing departments meet the specifications for COVID 19 testing kits. Kits not passing the inspection at this stage will be returned to the Designing Department and the total cost of those will be deducted from 'Transferred In' costs. The second quality inspection is carried out at 90% level of completion and spoilages up to 5% of units passed the inspection will be considered as normal. Spoilages units at this stage will be send back to the Designing Department for a recovery cost of $0.50 each. It means that the Designing Department gives a credit of 50 cents to the Finishing Department for every spoilage, which is specified at 90% level of completion in the Finishing Department. The following information is available for the month of April in the Finishing Department: Physical units Direct Materials (S) Transfer in Costs Buffer bottles (S) Conversion Costs (S) Direct Labour Costs ($) 2.721 5.938 3,133 2.883 WIP (April 1st) % of completion of Opening WIP Transferred in during April 60% 26.755 Good units completed and transferred out in WIP (April 30th) 21.404 2.671 30% % of completion of Ending WIP Total costs added during April 41.208 6,074 4,091 33,123 5% Normal spoilage rate Transferred in to be retumed (faulty) at the beginning Recovery sale value per unit $ 0.50Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

IT Auditing Using Controls To Protect Information Assets

Authors: Chris Davis, Mike Schiller, Kevin Wheeler

3rd Edition

1260453227, 978-1260453225