Prepare an adjusted income statement for AOL, after taking out unusual items, purchased R&D, and adjusting the accruals for customer acquisition costs and product development costs. Ignore taxes Is there any evidence that AOL benefited from operating leverage? (use the adjusted numbers to determine whether AOL benefitted from operating leverage) Compare the inferences that you make from the original and adjusted statements If you were the partner in charge of the AOL audit and AOL pitched to you it In years 8 and beyond (until the merger with Time Warner), AOL was highly profitable on a conventional accounting basis. What does the AOL story tell you about the difficulty that accounting has with businesses that are driven by the internal development of intangible assets?

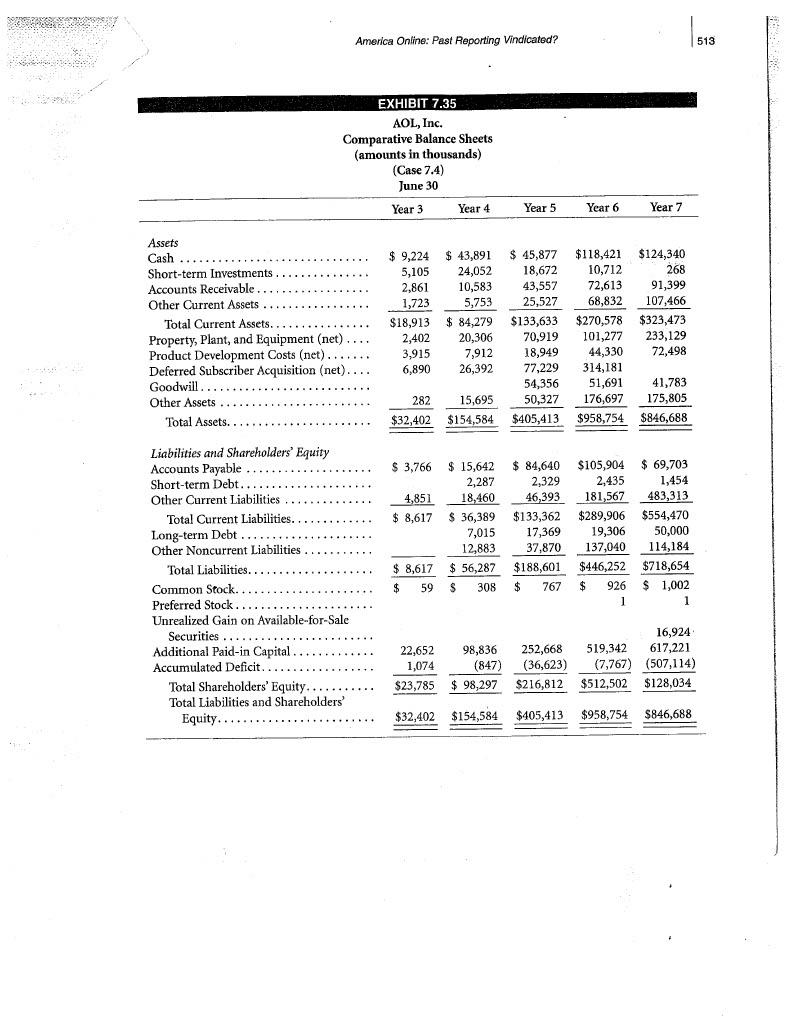

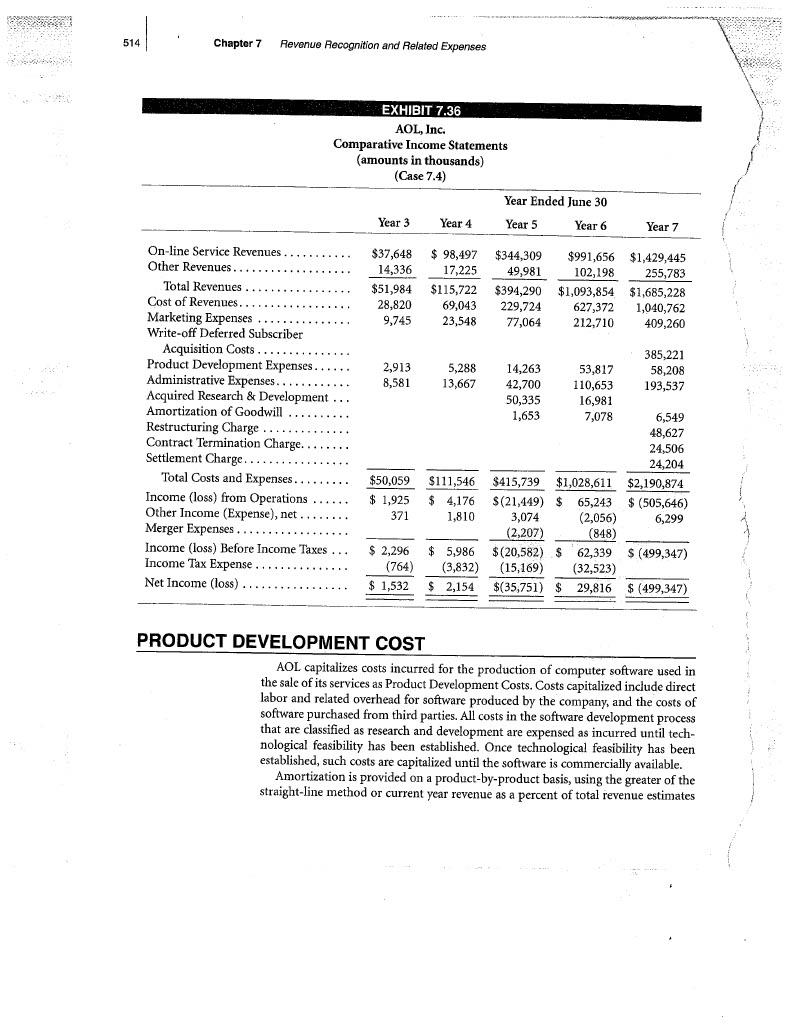

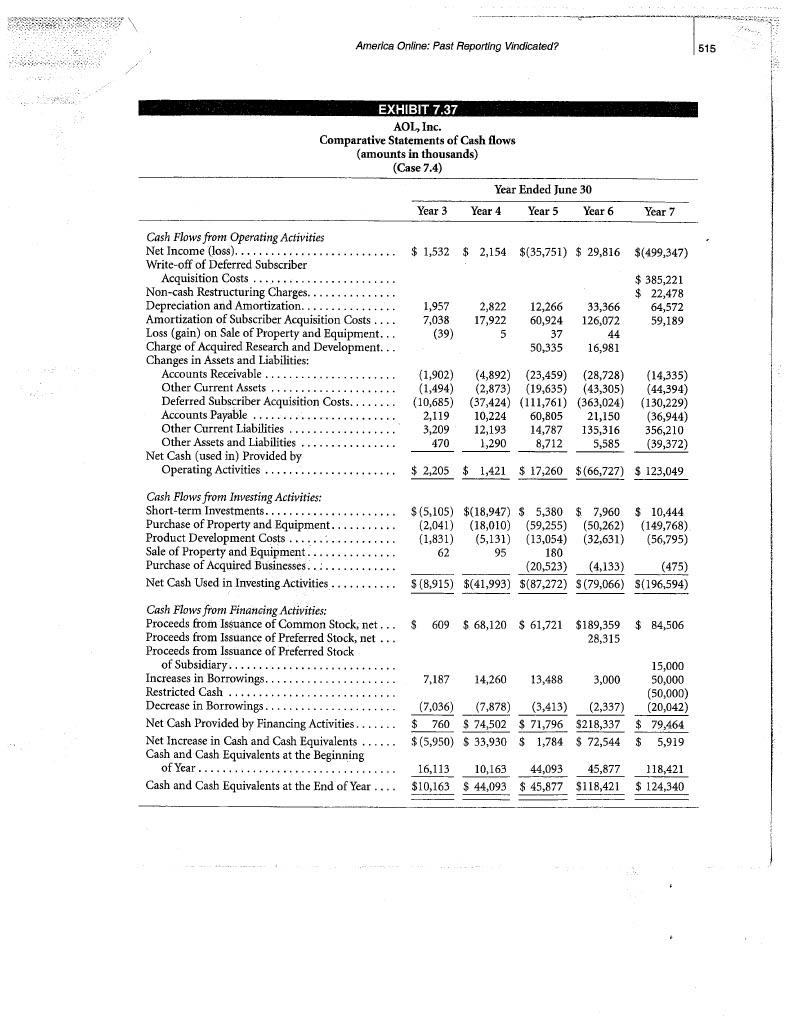

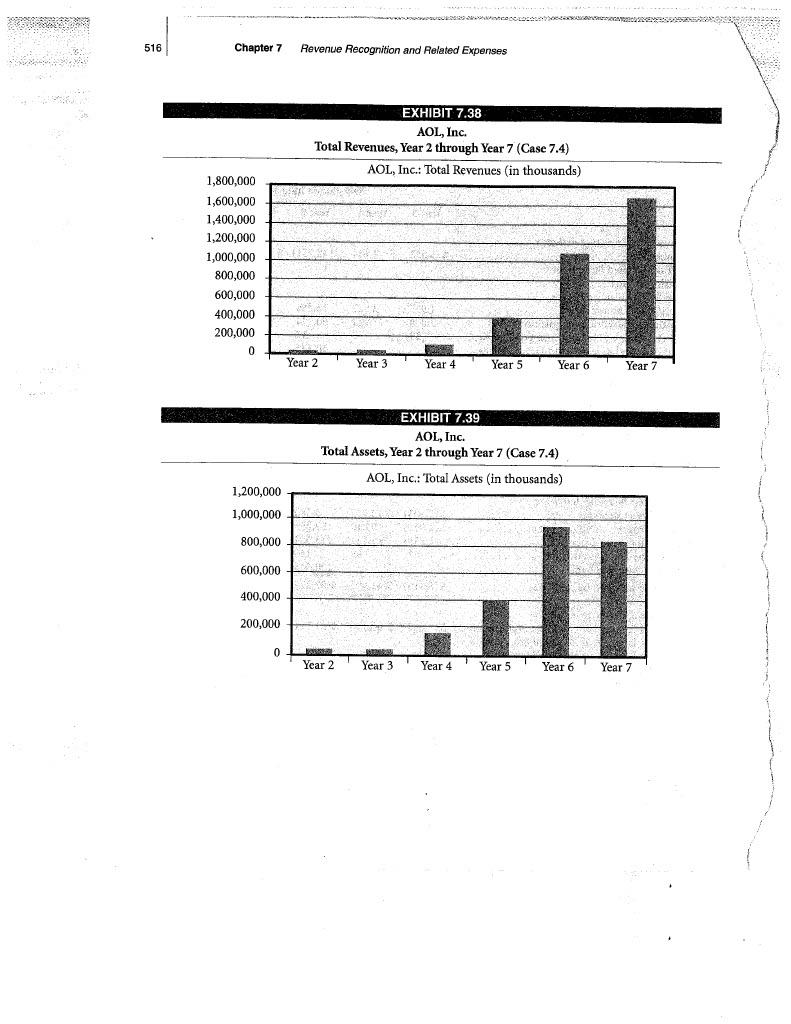

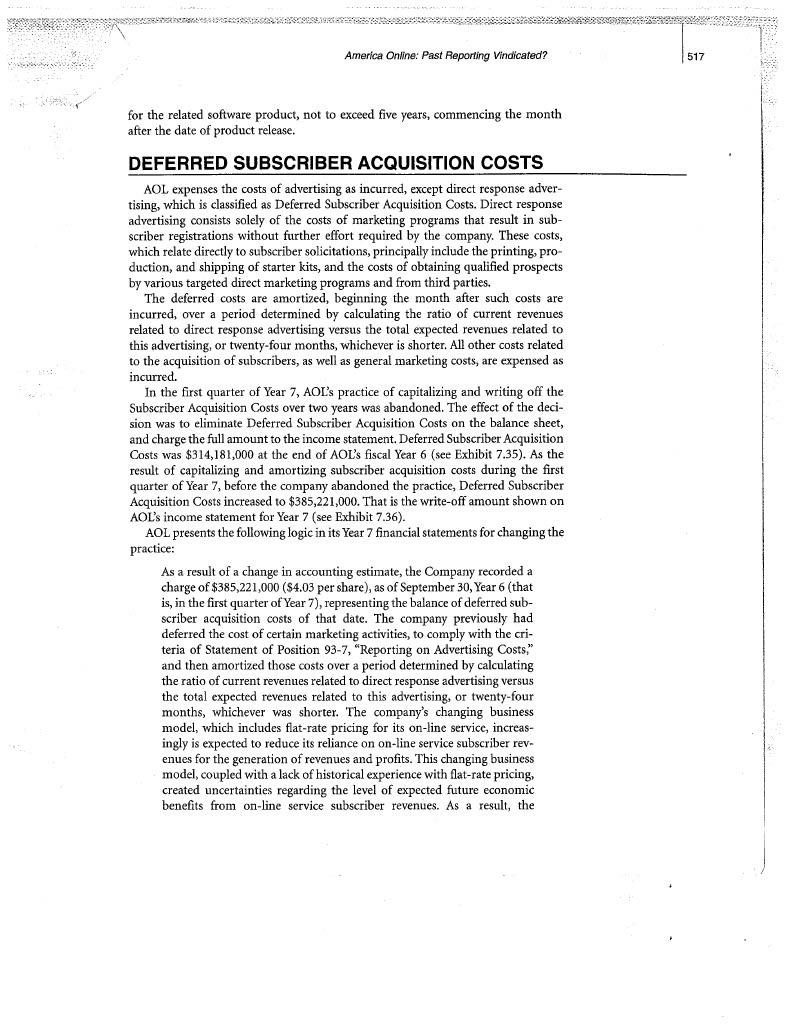

c. What is the likely explanation for Sanluis' recognition of a purchasing power gain on its monetary items during Year 8 ? d. Did Sanluis experience a holding gain or a holding loss on its nonmonetary items (that is, inventories, fixed assets) during Year 8 ? What is the interpretation of this gain or loss? e. How well has Sanluis coped with changing prices during Year 7 and Year 8 ? Note: Mexico's consumer price index increased 18.8 percent in Year 7 and 11.9 percent in Year 8. CASE 7.4 AMERICA ONLINE: PAST REPORTING VINDICATED? America Online, Inc. (AOL) is currently the world's largest Internet service provider. At the time of the merger of AOL and Time Warner in Year 11, AOL had one of the largest subscriber bases in the world. Over 40 million individuals subscribed to AOL in a recent year, and the firm continually adjusts its strategic plan in an attempt to reach even a larger set of Internet users. Synergies with Time Warner, such as exclusive access to the film and television content of the Time Warner libraries, and bandwidth benefits provided by the extensive cable system of Time Warner for Internet access and content delivery, garner tremendous advantages to AOL over its competitors. The industry is a competitive one, however, and it is unclear whether AOL can continue to dominate in the future. AOL subscriptions grew at a tremendous pace in its early years of existence. After only five fully operational years, AOL subscribers reached 8 million, making the firm substantially larger than any of its direct competitors. By end of Year 7, AOL reached its goal of 10 million subscribers worldwide. PRICING POLICY AOL's main source of revenue is on-line Internet service fees generated through customer subscriptions. In its early years of existence, AOL generated revenues from subscribers paying both (1) a monthly membership fee and (2) hourly charges based on usage in excess of the number of hours of usage provided as part of the monthly fee. In the last quarter of Year 6 , however, AOL launched its unlimited-use pricing policy. During the quarter ended December 31 , Year 6 , both AOL membership and system usage showed record growth. Membership climbed 1.2 million to a total 7.8 million with a record 546,000 new members added in December alone. This included 7.4 million members in North America and approximately 400,000 in Europe. Industry analysts praised AOL's move to flat-rate pricing but the move also caused the company major problems. The network became so crowded that users were blocked from dialing in because there weren't enough open lines. State regulatory officials who had complained to AOL on behalf of their customers reached a settlement whereby AOL agreed to give customer refunds. As part of the settlement, AOL also said it would sharply reduce marketing and advertising efforts, temporarily scale back its efforts to attract new members, and, for the time being, stop airing its television advertising as well as sharply reduce the distribution of free trial disks. On January 16, Year 7,AOL announced that membership in its on-line Internet network has surpassed 8 million and also said it would increase investment in system expansion to address the extraordinary demand for its service. The increased investment in system expansion included increasing its previously announced investment to expand system capacity from $250 million to $350 million, increasing the current total of 200,000-plus modems by 75 percent to improve connectivity, and promoting and supporting alternative ways to get AOL through work or school connections. But only months after a national controversy about its jammed networks, AOL. started to recruit members again. Word of AOL's plans came from Chief Executive Steve Case in his April, Year 7, monthly letter to subscribers. On September 2, Year 7 , AOL announced the company had more than 9 million subscribers worldwide, including more than 400,000 net new members since the quarter ending June 30 . CIAL REPORTING POLICIES The financial statements of AOL are presented in Exhibits 7.35, 7.36, and 7.37. The statements presented are prior to the merger of AOL and Time Warner, which took place in Year 11. As Exhibit 7.38 illustrates, total revenues grew along with AOL's membership. AOL's total revenues increased from $115.7 million in Year 4 to $394.3 million in Year 5 , or a 241 percent growth. The increase was primarily attributable to a 233 percent increase in the number of AOL subscribers, which contributed 250 percent growth of on-line service revenues. For fiscal Year 6 , total revenues increased to $1.1 billion, or 177 percent over fiscal Year 5 . On-line service revenues increased 188 percent to $991.7 million, which was primarily attributable to 93 percent growth in the number of AOL subscribers. For Year 7 , on-line service revenues increased to $1.4 billion, or 44 percent over Year 6 . This increase was primarily attributable to a 53 percent increase in the quarterly average number of AOL North American subscribers for Year 7. Total revenues in Year 7 were $1.7 billion, or 54 percent over Year 6 . As Exhibit 7.39 illustrates, AOL's total assets increased from $155.2 million in Year 4 to $405.4 million in Year 5 , a 161 percent growth. In Year 6 , the company's total assets increased to $958.8 million, or 136 percent over Year 5. Due to the $385.2mil lion write-off of Deferred Subscriber Acquisition Costs in Year 7, AOL's total assets decreased to $846.7 million, a 12 percent decrease compared to Year 6 . Two categories of AOL costs are central to analyzing the quality of the accounting information provided by AOL during this period: product development costs and deferred subscriber acquisition costs. America Online: Past Reporting Vindicated? EXHIBIT 7.35 EXHIBIT 7.36 AOL, Inc. Comparative Income Statements (amounte in thomeando) EVELOPMENT COST AOL capitalizes costs incurred for the production of computer software used in the sale of its services as Product Development Costs. Costs capitalized include direct labor and related overhead for software produced by the company, and the costs of software purchased from third parties. All costs in the software development process that are classified as research and development are expensed as incurred until technological feasibility has been established. Once technological feasibility has been established, such costs are capitalized until the software is commercially available. Amortization is provided on a product-by-product basis, using the greater of the straight-line method or current year revenue as a percent of total revenue estimates America Online: Past Reporting Vindicated? EXHIBIT 7.37 AOL, Inc. Comparative Statements of Cash flows Chapter 7 Revenue Recognition and Related Expenses EXHIBIT 7.38 AOL, Inc. EXHIBIT 7.39 AOL, Inc. Total Assets, Year 2 through Year 7 (Case 7.4) for the related software product, not to exceed five years, commencing the month after the date of product release. DEFERRED SUBSCRIBER ACQUISITION COSTS AOL expenses the costs of advertising as incurred, except direct response advertising, which is classified as Deferred Subscriber Acquisition Costs. Direct response advertising consists solely of the costs of marketing programs that result in subscriber registrations without further effort required by the company. These costs, which relate directly to subscriber solicitations, principally include the printing, production, and shipping of starter kits, and the costs of obtaining qualified prospects by various targeted direct marketing programs and from third parties. The deferred costs are amortized, beginning the month after such costs are incurred, over a period determined by calculating the ratio of current revenues related to direct response advertising versus the total expected revenues related to this advertising, or twenty-four months, whichever is shorter. All other costs related to the acquisition of subscribers, as well as general marketing costs, are expensed as incurred. In the first quarter of Year 7, AOL's practice of capitalizing and writing off the Subscriber Acquisition Costs over two years was abandoned. The effect of the decision was to eliminate Deferred Subscriber Acquisition Costs on the balance sheet, and charge the full amount to the income statement. Deferred Subscriber Acquisition Costs was $314,181,000 at the end of AOL's fiscal Year 6 (see Exhibit 7.35). As the result of capitalizing and amortizing subscriber acquisition costs during the first quarter of Year 7 , before the company abandoned the practice, Deferred Subscriber Acquisition Costs increased to $385,221,000. That is the write-off amount shown on AOL's income statement for Year 7 (see Exhibit 7.36). AOL presents the following logic in its Year 7 financial statements for changing the practice: As a result of a change in accounting estimate, the Company recorded a charge of $385,221,000 ( $4.03 per share), as of September 30, Year 6 (that is, in the first quarter of Year 7), representing the balance of deferred subscriber acquisition costs of that date. The company previously had deferred the cost of certain marketing activities, to comply with the criteria of Statement of Position 93-7, "Reporting on Advertising Costs," and then amortized those costs over a period determined by calculating the ratio of current revenues related to direct response advertising versus the total expected revenues related to this advertising, or twenty-four months, whichever was shorter. The company's changing business model, which includes flat-rate pricing for its on-line service, increasingly is expected to reduce its reliance on on-line service subscriber revenues for the generation of revenues and profits. This changing business model, coupled with a lack of historical experience with flat-rate pricing, created uncertainties regarding the level of expected future economic benefits from on-line service subscriber revenues. As a result, the company believed it no longer had an adequate accounting basis to support recognizing deferred subscriber acquisition costs as an asset. Required a. Prepare an analysis that accounts for the change in the Deferred Subscriber Acquisition Costs account on the balance sheet for each of the fiscal years from Year 4 through Year 7 by using Amortization of Subscriber Acquisition Costs and Deferred Subscriber Acquisition Costs accounts from the Statements of Cash Flows. b. Compare the Subscriber Acquisition Costs amortized from part a with total Marketing Expenses on the Income Statement. Calculate the percentage that this amortization bears to total Marketing Expenses for each of the fiscal years from Year 3 to Year 7. c. Prepare an analysis of the change in the Product Development Costs on the Balance Sheet account for each of the fiscal years from Year 4 to Year 7 , given that the costs capitalized were $5,131,000,$13,054,000,$32,735,000, and $55,363,000, respectively, and cost amortized were $1,134,000,$2,017,000, $7,354,000, and $27,195,000, respectively. d. Compare Amortization of Product Development Costs with Total Product Development Expenses in the Income Statement. Calculate the percentage that amortization bears to Total Product Development Expenses for each of the fiscal years from Year 3 to Year 7. e. Recompute the Income (Loss) from Operations in the Income Statements for AOL for each of the fiscal years Year 4 to Year 7 assuming that (a) the company expensed Subscriber Acquisition Costs and Product Development Costs in the year incurred instead of capitalizing, then amortizing the costs, or (b) excludes Acquired Research \& Development Costs and the Write-off of Subscriber Acquisition Costs from the Income from Operations because of its materiality and nonrecurring nature. f. In May, Year 10, eight months prior to the merger of AOL and Time Warner, AOL was fined $3.5 million by the Securities and Exchange Commission to settle charges that it mislead investors by following the policy of capitalizing and amortizing subscriber acquisition costs. Comment on both the (1) timing of the settlement and (2) SEC requirement that AOL restate earnings during the periods that the firm capitalized subscriber acquisition costs. c. What is the likely explanation for Sanluis' recognition of a purchasing power gain on its monetary items during Year 8 ? d. Did Sanluis experience a holding gain or a holding loss on its nonmonetary items (that is, inventories, fixed assets) during Year 8 ? What is the interpretation of this gain or loss? e. How well has Sanluis coped with changing prices during Year 7 and Year 8 ? Note: Mexico's consumer price index increased 18.8 percent in Year 7 and 11.9 percent in Year 8. CASE 7.4 AMERICA ONLINE: PAST REPORTING VINDICATED? America Online, Inc. (AOL) is currently the world's largest Internet service provider. At the time of the merger of AOL and Time Warner in Year 11, AOL had one of the largest subscriber bases in the world. Over 40 million individuals subscribed to AOL in a recent year, and the firm continually adjusts its strategic plan in an attempt to reach even a larger set of Internet users. Synergies with Time Warner, such as exclusive access to the film and television content of the Time Warner libraries, and bandwidth benefits provided by the extensive cable system of Time Warner for Internet access and content delivery, garner tremendous advantages to AOL over its competitors. The industry is a competitive one, however, and it is unclear whether AOL can continue to dominate in the future. AOL subscriptions grew at a tremendous pace in its early years of existence. After only five fully operational years, AOL subscribers reached 8 million, making the firm substantially larger than any of its direct competitors. By end of Year 7, AOL reached its goal of 10 million subscribers worldwide. PRICING POLICY AOL's main source of revenue is on-line Internet service fees generated through customer subscriptions. In its early years of existence, AOL generated revenues from subscribers paying both (1) a monthly membership fee and (2) hourly charges based on usage in excess of the number of hours of usage provided as part of the monthly fee. In the last quarter of Year 6 , however, AOL launched its unlimited-use pricing policy. During the quarter ended December 31 , Year 6 , both AOL membership and system usage showed record growth. Membership climbed 1.2 million to a total 7.8 million with a record 546,000 new members added in December alone. This included 7.4 million members in North America and approximately 400,000 in Europe. Industry analysts praised AOL's move to flat-rate pricing but the move also caused the company major problems. The network became so crowded that users were blocked from dialing in because there weren't enough open lines. State regulatory officials who had complained to AOL on behalf of their customers reached a settlement whereby AOL agreed to give customer refunds. As part of the settlement, AOL also said it would sharply reduce marketing and advertising efforts, temporarily scale back its efforts to attract new members, and, for the time being, stop airing its television advertising as well as sharply reduce the distribution of free trial disks. On January 16, Year 7,AOL announced that membership in its on-line Internet network has surpassed 8 million and also said it would increase investment in system expansion to address the extraordinary demand for its service. The increased investment in system expansion included increasing its previously announced investment to expand system capacity from $250 million to $350 million, increasing the current total of 200,000-plus modems by 75 percent to improve connectivity, and promoting and supporting alternative ways to get AOL through work or school connections. But only months after a national controversy about its jammed networks, AOL. started to recruit members again. Word of AOL's plans came from Chief Executive Steve Case in his April, Year 7, monthly letter to subscribers. On September 2, Year 7 , AOL announced the company had more than 9 million subscribers worldwide, including more than 400,000 net new members since the quarter ending June 30 . CIAL REPORTING POLICIES The financial statements of AOL are presented in Exhibits 7.35, 7.36, and 7.37. The statements presented are prior to the merger of AOL and Time Warner, which took place in Year 11. As Exhibit 7.38 illustrates, total revenues grew along with AOL's membership. AOL's total revenues increased from $115.7 million in Year 4 to $394.3 million in Year 5 , or a 241 percent growth. The increase was primarily attributable to a 233 percent increase in the number of AOL subscribers, which contributed 250 percent growth of on-line service revenues. For fiscal Year 6 , total revenues increased to $1.1 billion, or 177 percent over fiscal Year 5 . On-line service revenues increased 188 percent to $991.7 million, which was primarily attributable to 93 percent growth in the number of AOL subscribers. For Year 7 , on-line service revenues increased to $1.4 billion, or 44 percent over Year 6 . This increase was primarily attributable to a 53 percent increase in the quarterly average number of AOL North American subscribers for Year 7. Total revenues in Year 7 were $1.7 billion, or 54 percent over Year 6 . As Exhibit 7.39 illustrates, AOL's total assets increased from $155.2 million in Year 4 to $405.4 million in Year 5 , a 161 percent growth. In Year 6 , the company's total assets increased to $958.8 million, or 136 percent over Year 5. Due to the $385.2mil lion write-off of Deferred Subscriber Acquisition Costs in Year 7, AOL's total assets decreased to $846.7 million, a 12 percent decrease compared to Year 6 . Two categories of AOL costs are central to analyzing the quality of the accounting information provided by AOL during this period: product development costs and deferred subscriber acquisition costs. America Online: Past Reporting Vindicated? EXHIBIT 7.35 EXHIBIT 7.36 AOL, Inc. Comparative Income Statements (amounte in thomeando) EVELOPMENT COST AOL capitalizes costs incurred for the production of computer software used in the sale of its services as Product Development Costs. Costs capitalized include direct labor and related overhead for software produced by the company, and the costs of software purchased from third parties. All costs in the software development process that are classified as research and development are expensed as incurred until technological feasibility has been established. Once technological feasibility has been established, such costs are capitalized until the software is commercially available. Amortization is provided on a product-by-product basis, using the greater of the straight-line method or current year revenue as a percent of total revenue estimates America Online: Past Reporting Vindicated? EXHIBIT 7.37 AOL, Inc. Comparative Statements of Cash flows Chapter 7 Revenue Recognition and Related Expenses EXHIBIT 7.38 AOL, Inc. EXHIBIT 7.39 AOL, Inc. Total Assets, Year 2 through Year 7 (Case 7.4) for the related software product, not to exceed five years, commencing the month after the date of product release. DEFERRED SUBSCRIBER ACQUISITION COSTS AOL expenses the costs of advertising as incurred, except direct response advertising, which is classified as Deferred Subscriber Acquisition Costs. Direct response advertising consists solely of the costs of marketing programs that result in subscriber registrations without further effort required by the company. These costs, which relate directly to subscriber solicitations, principally include the printing, production, and shipping of starter kits, and the costs of obtaining qualified prospects by various targeted direct marketing programs and from third parties. The deferred costs are amortized, beginning the month after such costs are incurred, over a period determined by calculating the ratio of current revenues related to direct response advertising versus the total expected revenues related to this advertising, or twenty-four months, whichever is shorter. All other costs related to the acquisition of subscribers, as well as general marketing costs, are expensed as incurred. In the first quarter of Year 7, AOL's practice of capitalizing and writing off the Subscriber Acquisition Costs over two years was abandoned. The effect of the decision was to eliminate Deferred Subscriber Acquisition Costs on the balance sheet, and charge the full amount to the income statement. Deferred Subscriber Acquisition Costs was $314,181,000 at the end of AOL's fiscal Year 6 (see Exhibit 7.35). As the result of capitalizing and amortizing subscriber acquisition costs during the first quarter of Year 7 , before the company abandoned the practice, Deferred Subscriber Acquisition Costs increased to $385,221,000. That is the write-off amount shown on AOL's income statement for Year 7 (see Exhibit 7.36). AOL presents the following logic in its Year 7 financial statements for changing the practice: As a result of a change in accounting estimate, the Company recorded a charge of $385,221,000 ( $4.03 per share), as of September 30, Year 6 (that is, in the first quarter of Year 7), representing the balance of deferred subscriber acquisition costs of that date. The company previously had deferred the cost of certain marketing activities, to comply with the criteria of Statement of Position 93-7, "Reporting on Advertising Costs," and then amortized those costs over a period determined by calculating the ratio of current revenues related to direct response advertising versus the total expected revenues related to this advertising, or twenty-four months, whichever was shorter. The company's changing business model, which includes flat-rate pricing for its on-line service, increasingly is expected to reduce its reliance on on-line service subscriber revenues for the generation of revenues and profits. This changing business model, coupled with a lack of historical experience with flat-rate pricing, created uncertainties regarding the level of expected future economic benefits from on-line service subscriber revenues. As a result, the company believed it no longer had an adequate accounting basis to support recognizing deferred subscriber acquisition costs as an asset. Required a. Prepare an analysis that accounts for the change in the Deferred Subscriber Acquisition Costs account on the balance sheet for each of the fiscal years from Year 4 through Year 7 by using Amortization of Subscriber Acquisition Costs and Deferred Subscriber Acquisition Costs accounts from the Statements of Cash Flows. b. Compare the Subscriber Acquisition Costs amortized from part a with total Marketing Expenses on the Income Statement. Calculate the percentage that this amortization bears to total Marketing Expenses for each of the fiscal years from Year 3 to Year 7. c. Prepare an analysis of the change in the Product Development Costs on the Balance Sheet account for each of the fiscal years from Year 4 to Year 7 , given that the costs capitalized were $5,131,000,$13,054,000,$32,735,000, and $55,363,000, respectively, and cost amortized were $1,134,000,$2,017,000, $7,354,000, and $27,195,000, respectively. d. Compare Amortization of Product Development Costs with Total Product Development Expenses in the Income Statement. Calculate the percentage that amortization bears to Total Product Development Expenses for each of the fiscal years from Year 3 to Year 7. e. Recompute the Income (Loss) from Operations in the Income Statements for AOL for each of the fiscal years Year 4 to Year 7 assuming that (a) the company expensed Subscriber Acquisition Costs and Product Development Costs in the year incurred instead of capitalizing, then amortizing the costs, or (b) excludes Acquired Research \& Development Costs and the Write-off of Subscriber Acquisition Costs from the Income from Operations because of its materiality and nonrecurring nature. f. In May, Year 10, eight months prior to the merger of AOL and Time Warner, AOL was fined $3.5 million by the Securities and Exchange Commission to settle charges that it mislead investors by following the policy of capitalizing and amortizing subscriber acquisition costs. Comment on both the (1) timing of the settlement and (2) SEC requirement that AOL restate earnings during the periods that the firm capitalized subscriber acquisition costs