Answered step by step

Verified Expert Solution

Question

1 Approved Answer

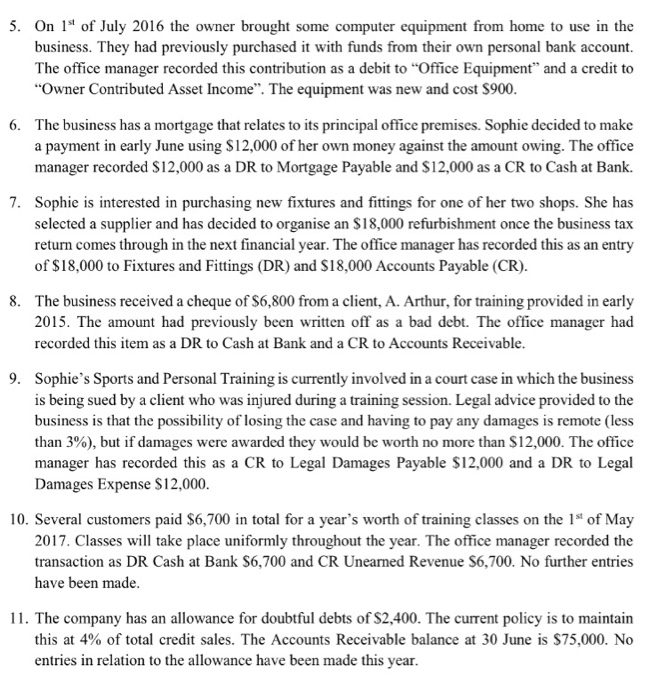

Prepare Journal entries for year ending 30 June 2017 using accrual accounting basis. Disregard all taxes. 5. On 1s of July 2016 the owner brought

Prepare Journal entries for year ending 30 June 2017 using accrual accounting basis. Disregard all taxes.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Alternative Minimum Tax For Individuals IRS Audit Technique Guide ATG

Authors: Internal Revenue Service

1st Edition

1304131556, 978-1304131553