Preparing for the annual healthcare facility audit is a major undertaking. It consumes a considerable portion of the CFOs time and energy each year. Review the items presented in Exhibit 1.3 of your textbook, and consider which of these areas might be most susceptible to adjustments by the auditors. What can the facilitys management team do to reduce audit adjustments in these areas?

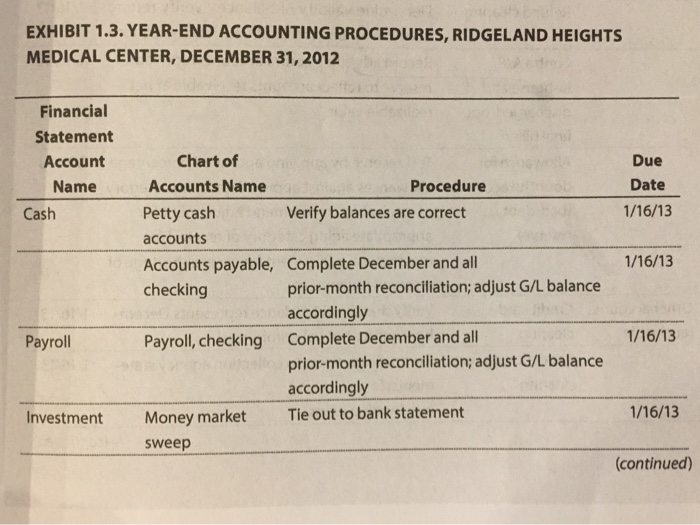

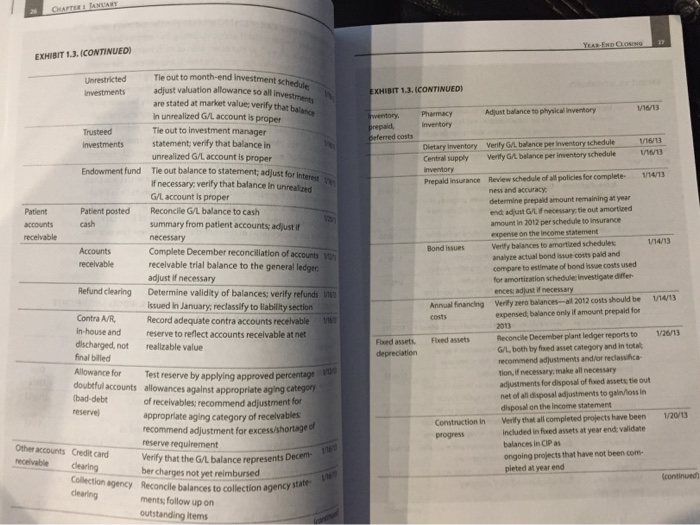

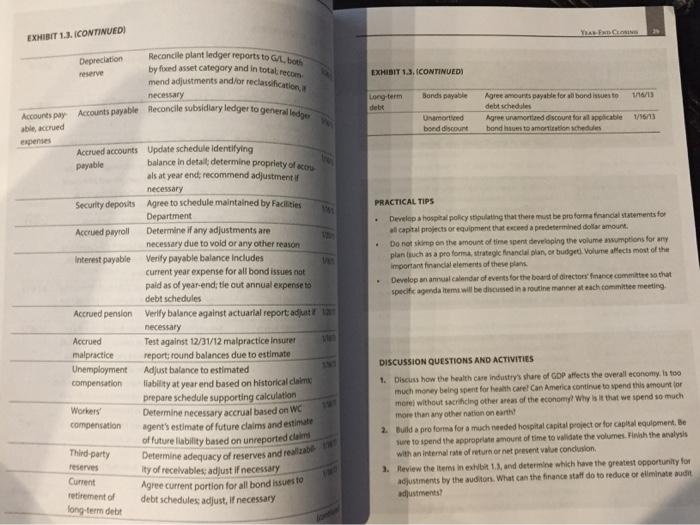

EXHIBIT 1.3. YEAR-END ACCOUNTING PROCEDURES, RIDGELAND HEIGHTS MEDICAL CENTER, DECEMBER 31, 2012 Financial Statement Account Name Cash Due Date 1/16/13 1/16/13 Chart of Accounts Name Procedure Petty cash V erify balances are correct accounts Accounts payable, Complete December and all checking prior-month reconciliation; adjust G/L balance accordingly Payroll, checking Complete December and all prior-month reconciliation; adjust G/L balance accordingly Money market Tie out to bank statement sweep Payroll 1/16/13 Investment 1/16/13 (continued) CARTEANUARY EXHIBIT 1.3. CONTINUED) EXHIBIT 1.3. CONTINUED) 116/13 Pharmacy Adjust balance to physical inventory Inventory prepaid, Deferred costs Dietary inventory Central supply Verify G/L balance per inventory schedule Verify GAL balance per inventory schedule 116/13 63 cash Tle out to month-end investment sche Unrestricted Investments adiust valuation allowance so all invece are stated at market values verify that in unrealized G/L account is proper Trusteed Tle out to investment manager Investments statement; verify that balance in unrealized G/L account is proper Endowment fund Tle out balance to statement; adjust for inte If necessary, verify that balance in unrealized G/L account is proper Patient Patient posted Reconcile G/L balance to cash accounts summary from patient accounts, adjust if receivable necessary Accounts Complete December reconciliation of accounts receivable receivable trial balance to the general ledger adjust if necessary Refund clearing Determine validity of balances; verify refunds Issued in January, reclassify to liability section Contra A/R Record adequate contra accounts recevable in-house and reserve to reflect accounts receivable at net discharged, not realizable value final billed Test reserve by applying approved percentage doubtful accounts allowances against appropriate aging category (bad-debt of receivables; recommend adjustment for reserve) appropriate aging category of receivables recommend adjustment for excess/shortaged reserve requirement Other accounts Credit Card Verify that the G/L balance represents Decem receivable ber charges not yet reimbursed Collection agency Reconcile balances to collection agency clearing ments: follow up on outstanding items VW Prepaid insurance Review schedule of all policies for complete. 114/13 ness and accuracy determine prepaid amount remaining at year end adjust G/L necessary the out amortid amount in 2012 per schedule to insurance expense on the income statement Bond issues Verify balances to amortized schedules 114/13 analyze actual bond we costs paid and compare to estimate of bond we costs used for amortization schedules investigate differ ences adjust if necessary Annual financing Verity zero balances-all 2012 costs should be 1/14/13 costs expensed, balance only if amount prepaid for 2013 Freed assets Reconcile December plant ledger reports to 1/26/13 G/L, both by foxed asset Category and in total recommend adjustments and/or reclassifica tion, if necessary, make all necessary adjustments for disposal offed assets te out net of all disposal adjustments to gainossin disposal on the income statement Construction in Verify that all completed projects have been 120/13 progress included in foued assets at year end validate balances in CIP as ongoing projects that have not been com pleted at year end continued Fixed assets. depreciation dearing ents Decem citate EXHIBIT 1.3. CONTINUEDI EXHIBIT 1.3. (CONTINUED) Bonds payable 176/13 general ledger Long-term debt Agree amounts payable for all bond issues to debt schedules Agree un amortized discount for all applicable bond issues to amortization schedules 1/16/13 Unamortired bond discount Reconcile plant ledger reports to G/L Depreciation reserve by fixed asset category and in total recom mend adjustments and/or reclassificati necessary Accounts pay Accounts payable Reconcile subsidiary ledgerton able, accrued expenses Accrued accounts Update schedule identifying payable balance in detail; determine propriety of als at year end; recommend adjustment if necessary Security deposits Agree to schedule maintained by Facilities Department Accrued payroll Determine if any adjustments are necessary due to void or any other reason Interest payable Verify payable balance includes current year expense for all bond issues not paid as of year-end; tle out annual expense to debt schedules Accrued pension Verify balance against actuarial reports adjust necessary Accrued Test against 12/31/12 malpractice insurer malpractice report: round balances due to estimate Unemployment Adjust balance to estimated compensation liability at year end based on historical claims prepare schedule supporting calculation Determine necessary accrual based on WC compensation agent's estimate of future claims and estimate of future liability based on unreported claim Third-party Determine adequacy of reserves and realita reserves ity of receivables; adjust if necessary Agree current portion for all bond issues to retirement of debt schedules adjust, if necessary long-term debt PRACTICAL TIPS Develop a hospital policy stipulating that there must be pro forma financial statements for all capital projects or equipment that exceed a predetermined dollar amount. Do not skimp on the amount of time spent developing the volume assumptions for any plan Guch as a proforma strategic financial plan, or budget. Volume afects most of the Important financial elements of these plans Develop an annual calendar of events for the board of directory' finance committee so that specific agenda Items will be discussed in a routine manner at each committee meeting. DISCUSSION QUESTIONS AND ACTIVITIES 1. Discuss how the health care industry's share of GDP affects the overall economy is too much money being spent for health care! Can America continue to spend this amount or more without sacrificing other areas of the economy? Why is it that we spend so much more than any other nation on earth? 2. Build a proforma for a much needed hospital capital projector for capital equipment. Be sure to spend the appropriate amount of time to validate the volumes. Finish the analysis with an internal rate of return or net present value conclusion 3. Review the items in exhibit 1.3, and determine which have the greatest opportunity for adjustments by the auditors. What can the finance staff do to reduce or eliminate audit adjustments? ferves and reallab Current EXHIBIT 1.3. YEAR-END ACCOUNTING PROCEDURES, RIDGELAND HEIGHTS MEDICAL CENTER, DECEMBER 31, 2012 Financial Statement Account Name Cash Due Date 1/16/13 1/16/13 Chart of Accounts Name Procedure Petty cash V erify balances are correct accounts Accounts payable, Complete December and all checking prior-month reconciliation; adjust G/L balance accordingly Payroll, checking Complete December and all prior-month reconciliation; adjust G/L balance accordingly Money market Tie out to bank statement sweep Payroll 1/16/13 Investment 1/16/13 (continued) CARTEANUARY EXHIBIT 1.3. CONTINUED) EXHIBIT 1.3. CONTINUED) 116/13 Pharmacy Adjust balance to physical inventory Inventory prepaid, Deferred costs Dietary inventory Central supply Verify G/L balance per inventory schedule Verify GAL balance per inventory schedule 116/13 63 cash Tle out to month-end investment sche Unrestricted Investments adiust valuation allowance so all invece are stated at market values verify that in unrealized G/L account is proper Trusteed Tle out to investment manager Investments statement; verify that balance in unrealized G/L account is proper Endowment fund Tle out balance to statement; adjust for inte If necessary, verify that balance in unrealized G/L account is proper Patient Patient posted Reconcile G/L balance to cash accounts summary from patient accounts, adjust if receivable necessary Accounts Complete December reconciliation of accounts receivable receivable trial balance to the general ledger adjust if necessary Refund clearing Determine validity of balances; verify refunds Issued in January, reclassify to liability section Contra A/R Record adequate contra accounts recevable in-house and reserve to reflect accounts receivable at net discharged, not realizable value final billed Test reserve by applying approved percentage doubtful accounts allowances against appropriate aging category (bad-debt of receivables; recommend adjustment for reserve) appropriate aging category of receivables recommend adjustment for excess/shortaged reserve requirement Other accounts Credit Card Verify that the G/L balance represents Decem receivable ber charges not yet reimbursed Collection agency Reconcile balances to collection agency clearing ments: follow up on outstanding items VW Prepaid insurance Review schedule of all policies for complete. 114/13 ness and accuracy determine prepaid amount remaining at year end adjust G/L necessary the out amortid amount in 2012 per schedule to insurance expense on the income statement Bond issues Verify balances to amortized schedules 114/13 analyze actual bond we costs paid and compare to estimate of bond we costs used for amortization schedules investigate differ ences adjust if necessary Annual financing Verity zero balances-all 2012 costs should be 1/14/13 costs expensed, balance only if amount prepaid for 2013 Freed assets Reconcile December plant ledger reports to 1/26/13 G/L, both by foxed asset Category and in total recommend adjustments and/or reclassifica tion, if necessary, make all necessary adjustments for disposal offed assets te out net of all disposal adjustments to gainossin disposal on the income statement Construction in Verify that all completed projects have been 120/13 progress included in foued assets at year end validate balances in CIP as ongoing projects that have not been com pleted at year end continued Fixed assets. depreciation dearing ents Decem citate EXHIBIT 1.3. CONTINUEDI EXHIBIT 1.3. (CONTINUED) Bonds payable 176/13 general ledger Long-term debt Agree amounts payable for all bond issues to debt schedules Agree un amortized discount for all applicable bond issues to amortization schedules 1/16/13 Unamortired bond discount Reconcile plant ledger reports to G/L Depreciation reserve by fixed asset category and in total recom mend adjustments and/or reclassificati necessary Accounts pay Accounts payable Reconcile subsidiary ledgerton able, accrued expenses Accrued accounts Update schedule identifying payable balance in detail; determine propriety of als at year end; recommend adjustment if necessary Security deposits Agree to schedule maintained by Facilities Department Accrued payroll Determine if any adjustments are necessary due to void or any other reason Interest payable Verify payable balance includes current year expense for all bond issues not paid as of year-end; tle out annual expense to debt schedules Accrued pension Verify balance against actuarial reports adjust necessary Accrued Test against 12/31/12 malpractice insurer malpractice report: round balances due to estimate Unemployment Adjust balance to estimated compensation liability at year end based on historical claims prepare schedule supporting calculation Determine necessary accrual based on WC compensation agent's estimate of future claims and estimate of future liability based on unreported claim Third-party Determine adequacy of reserves and realita reserves ity of receivables; adjust if necessary Agree current portion for all bond issues to retirement of debt schedules adjust, if necessary long-term debt PRACTICAL TIPS Develop a hospital policy stipulating that there must be pro forma financial statements for all capital projects or equipment that exceed a predetermined dollar amount. Do not skimp on the amount of time spent developing the volume assumptions for any plan Guch as a proforma strategic financial plan, or budget. Volume afects most of the Important financial elements of these plans Develop an annual calendar of events for the board of directory' finance committee so that specific agenda Items will be discussed in a routine manner at each committee meeting. DISCUSSION QUESTIONS AND ACTIVITIES 1. Discuss how the health care industry's share of GDP affects the overall economy is too much money being spent for health care! Can America continue to spend this amount or more without sacrificing other areas of the economy? Why is it that we spend so much more than any other nation on earth? 2. Build a proforma for a much needed hospital capital projector for capital equipment. Be sure to spend the appropriate amount of time to validate the volumes. Finish the analysis with an internal rate of return or net present value conclusion 3. Review the items in exhibit 1.3, and determine which have the greatest opportunity for adjustments by the auditors. What can the finance staff do to reduce or eliminate audit adjustments? ferves and reallab Current