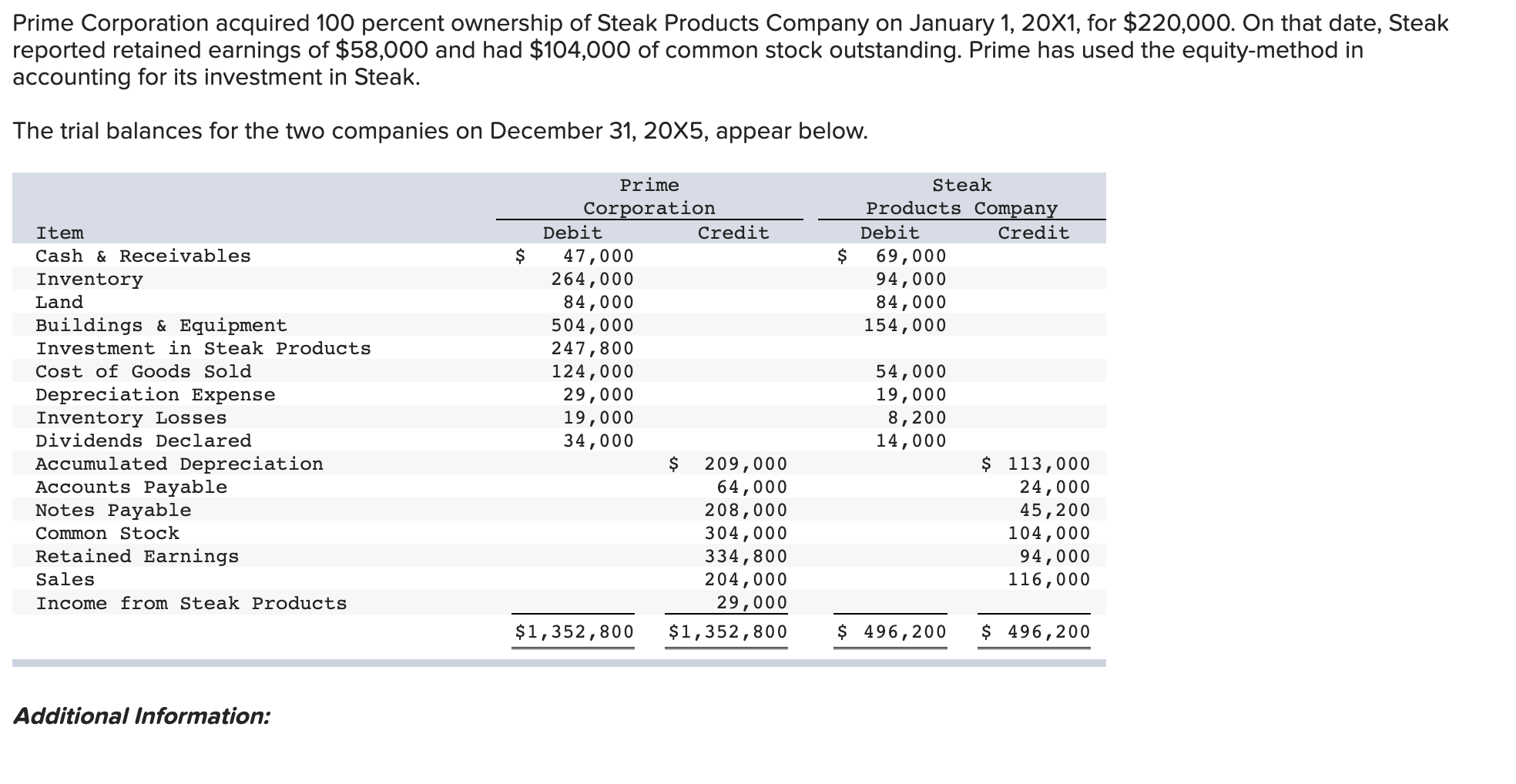

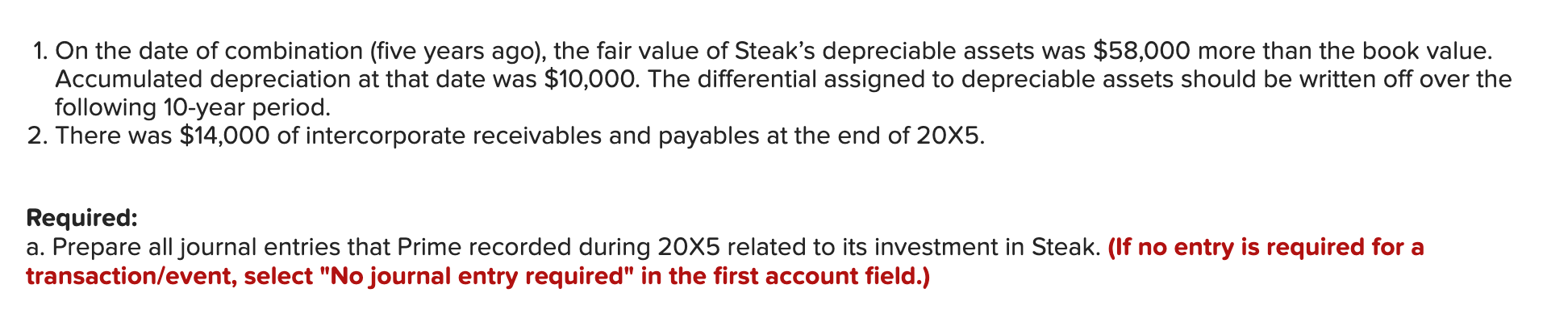

Prime Corporation acquired 100 percent ownership of Steak Products Company on January 1, 20x1, for $220,000. On that date, Steak reported retained earnings of $58,000 and had $104,000 of common stock outstanding. Prime has used the equity-method in accounting for its investment in Steak. The trial balances for the two companies on December 31, 20X5, appear below. $ Steak Products Company Debit Credit 69,000 94,000 84,000 154,000 Item Cash & Receivables Inventory Land Buildings & Equipment Investment in Steak Products Cost of Goods Sold Depreciation Expense Inventory Losses Dividends Declared Accumulated Depreciation Accounts Payable Notes Payable Common Stock Retained Earnings Sales Income from Steak Products Prime Corporation Debit Credit $ 47,000 264,000 84,000 504,000 247,800 124,000 29,000 19,000 34,000 $ 209,000 64,000 208,000 304,000 334,800 204,000 29,000 $1,352,800 $1,352,800 54,000 19,000 8, 200 14,000 $ 113,000 24,000 45,200 104,000 94,000 116,000 $ 496,200 $ 496,200 Additional Information: 1. On the date of combination (five years ago), the fair value of Steak's depreciable assets was $58,000 more than the book value. Accumulated depreciation at that date was $10,000. The differential assigned to depreciable assets should be written off over the following 10-year period. 2. There was $14,000 of intercorporate receivables and payables at the end of 20X5. Required: a. Prepare all journal entries that Prime recorded during 20x5 related to its investment in Steak. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.) b. Prepare all consolidating entries needed to prepare consolidated statements for 20X5. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.) c. Prepare a three-part worksheet as of December 31, 20X5. (Values in the first two columns (the "parent" and "subsidiary" balances) that are to be deducted should be indicated with a minus sign, while all values in the "Consolidation Entries" columns should be entered as positive values. For accounts where multiple adjusting entries are required, combine all debit entries into one amount and enter this amount in the debit column of the worksheet. Similarly, combine all credit entries into one amount and enter this amount in the credit column of the worksheet.) Prime Corporation acquired 100 percent ownership of Steak Products Company on January 1, 20x1, for $220,000. On that date, Steak reported retained earnings of $58,000 and had $104,000 of common stock outstanding. Prime has used the equity-method in accounting for its investment in Steak. The trial balances for the two companies on December 31, 20X5, appear below. $ Steak Products Company Debit Credit 69,000 94,000 84,000 154,000 Item Cash & Receivables Inventory Land Buildings & Equipment Investment in Steak Products Cost of Goods Sold Depreciation Expense Inventory Losses Dividends Declared Accumulated Depreciation Accounts Payable Notes Payable Common Stock Retained Earnings Sales Income from Steak Products Prime Corporation Debit Credit $ 47,000 264,000 84,000 504,000 247,800 124,000 29,000 19,000 34,000 $ 209,000 64,000 208,000 304,000 334,800 204,000 29,000 $1,352,800 $1,352,800 54,000 19,000 8, 200 14,000 $ 113,000 24,000 45,200 104,000 94,000 116,000 $ 496,200 $ 496,200 Additional Information: 1. On the date of combination (five years ago), the fair value of Steak's depreciable assets was $58,000 more than the book value. Accumulated depreciation at that date was $10,000. The differential assigned to depreciable assets should be written off over the following 10-year period. 2. There was $14,000 of intercorporate receivables and payables at the end of 20X5. Required: a. Prepare all journal entries that Prime recorded during 20x5 related to its investment in Steak. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.) b. Prepare all consolidating entries needed to prepare consolidated statements for 20X5. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.) c. Prepare a three-part worksheet as of December 31, 20X5. (Values in the first two columns (the "parent" and "subsidiary" balances) that are to be deducted should be indicated with a minus sign, while all values in the "Consolidation Entries" columns should be entered as positive values. For accounts where multiple adjusting entries are required, combine all debit entries into one amount and enter this amount in the debit column of the worksheet. Similarly, combine all credit entries into one amount and enter this amount in the credit column of the worksheet.)