Answered step by step

Verified Expert Solution

Question

1 Approved Answer

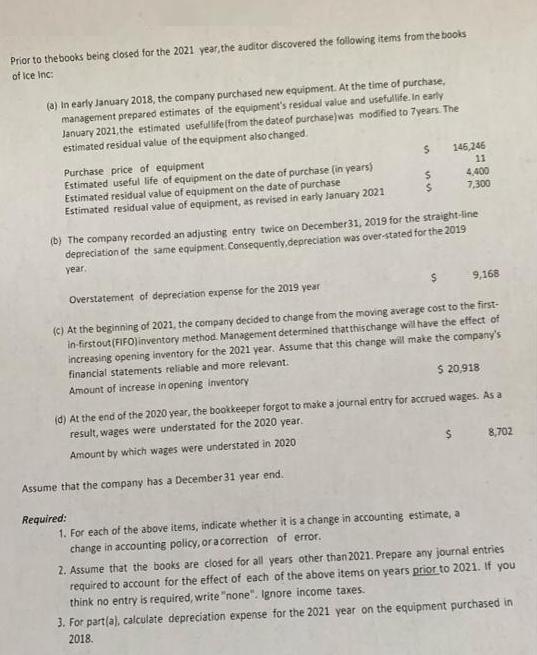

Prior to the books being closed for the 2021 year, the auditor discovered the following items from the books of Ice Inc: (a) In

Prior to the books being closed for the 2021 year, the auditor discovered the following items from the books of Ice Inc: (a) In early January 2018, the company purchased new equipment. At the time of purchase, management prepared estimates of the equipment's residual value and usefullife. In early January 2021, the estimated useful life (from the date of purchase)was modified to 7years. The estimated residual value of the equipment also changed. Purchase price of equipment Estimated useful life of equipment on the date of purchase (in years) Estimated residual value of equipment on the date of purchase Estimated residual value of equipment, as revised in early January 2021 $ $ $ 146,246 11 4,400 7,300 (b) The company recorded an adjusting entry twice on December 31, 2019 for the straight-line depreciation of the same equipment. Consequently,depreciation was over-stated for the 2019 year. Overstatement of depreciation expense for the 2019 year $ 9,168 (c) At the beginning of 2021, the company decided to change from the moving average cost to the first- in-first out (FIFO) inventory method. Management determined that this change will have the effect of increasing opening inventory for the 2021 year. Assume that this change will make the company's financial statements reliable and more relevant. Amount of increase in opening Inventory $ 20,918 (d) At the end of the 2020 year, the bookkeeper forgot to make a journal entry for accrued wages. As a result, wages were understated for the 2020 year. Amount by which wages were understated in 2020 Assume that the company has a December 31 year end. Required: 1. For each of the above items, indicate whether it is a change in accounting estimate, a change in accounting policy, or a correction of error. 8,702 2. Assume that the books are closed for all years other than 2021. Prepare any journal entries required to account for the effect of each of the above items on years prior to 2021. If you think no entry is required, write "none". Ignore income taxes. 3. For part(a), calculate depreciation expense for the 2021 year on the equipment purchased in 2018.

Step by Step Solution

★★★★★

3.50 Rating (163 Votes )

There are 3 Steps involved in it

Step: 1

Requirement 1 a In this case company has revised the useful life and residual value of an equipment ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting IFRS

Authors: Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield

3rd edition

1119372933, 978-1119372936