Answered step by step

Verified Expert Solution

Question

1 Approved Answer

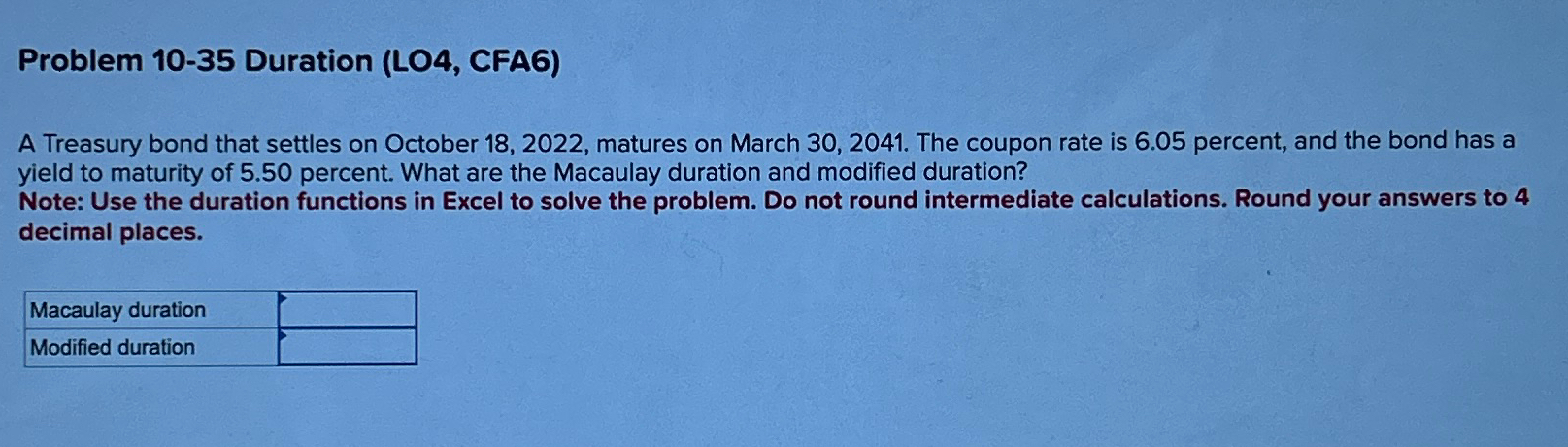

Problem 1 0 - 3 5 Duration ( LO 4 , CFA 6 ) A Treasury bond that settles on October 1 8 , 2

Problem Duration LO CFA

A Treasury bond that settles on October matures on March The coupon rate is percent, and the bond has a yield to maturity of percent. What are the Macaulay duration and modified duration?

Note: Use the duration functions in Excel to solve the problem. Do not round intermediate calculations. Round your answers to decimal places.

Macaulay duration

Modified duration

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

All About Options

Authors: Thomas McCafferty

3rd Edition

0071484795, 978-0071484794