Answered step by step

Verified Expert Solution

Question

1 Approved Answer

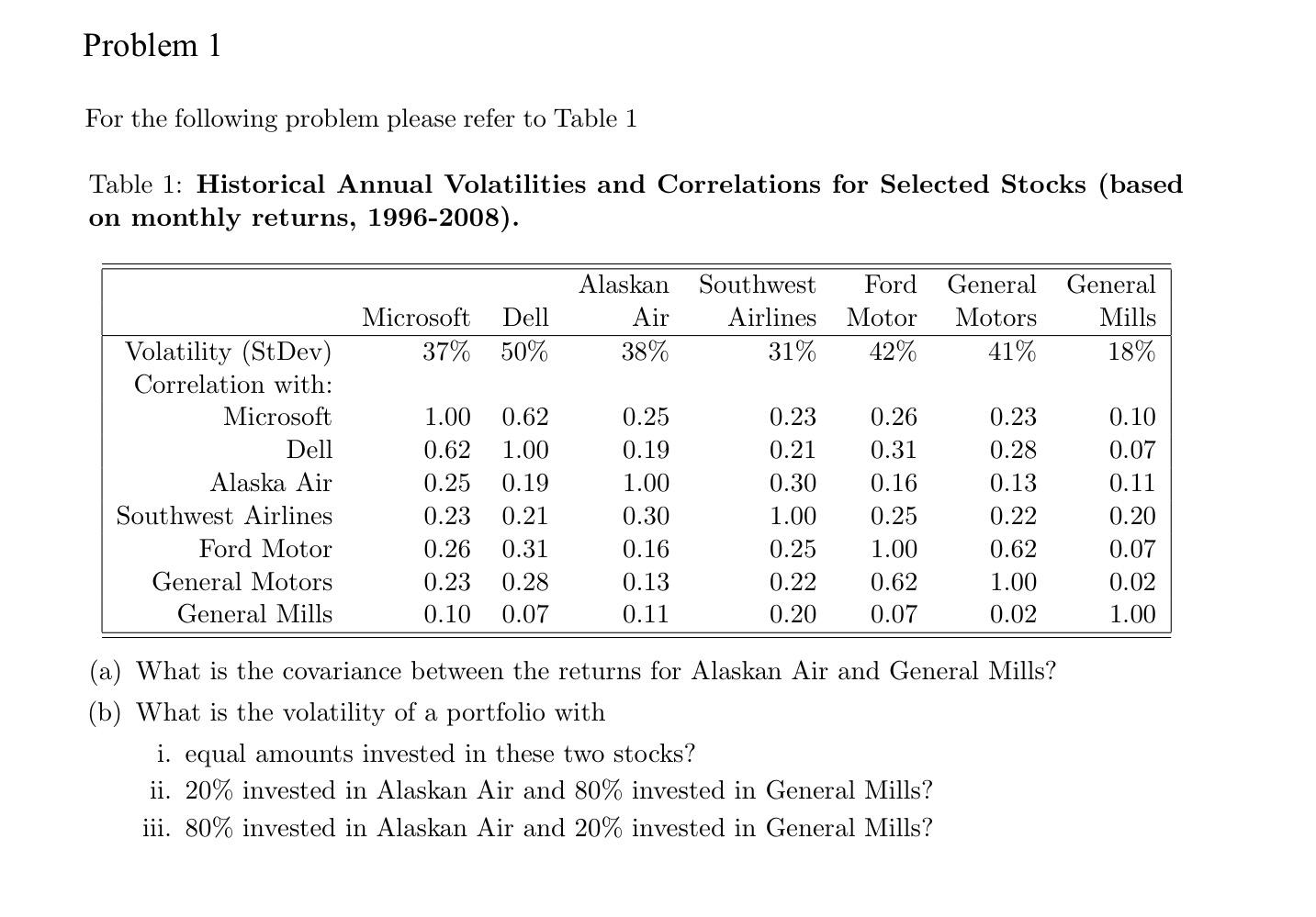

Problem 1 For the following problem please refer to Table 1 Table 1: Historical Annual Volatilities and Correlations for Selected Stocks (based on monthly returns,

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Practical Financial Management

Authors: William R. Lasher

7th edition

128560721X, 9781133593669, 1133593682, 9781285607214, 978-1133593683