Answered step by step

Verified Expert Solution

Question

1 Approved Answer

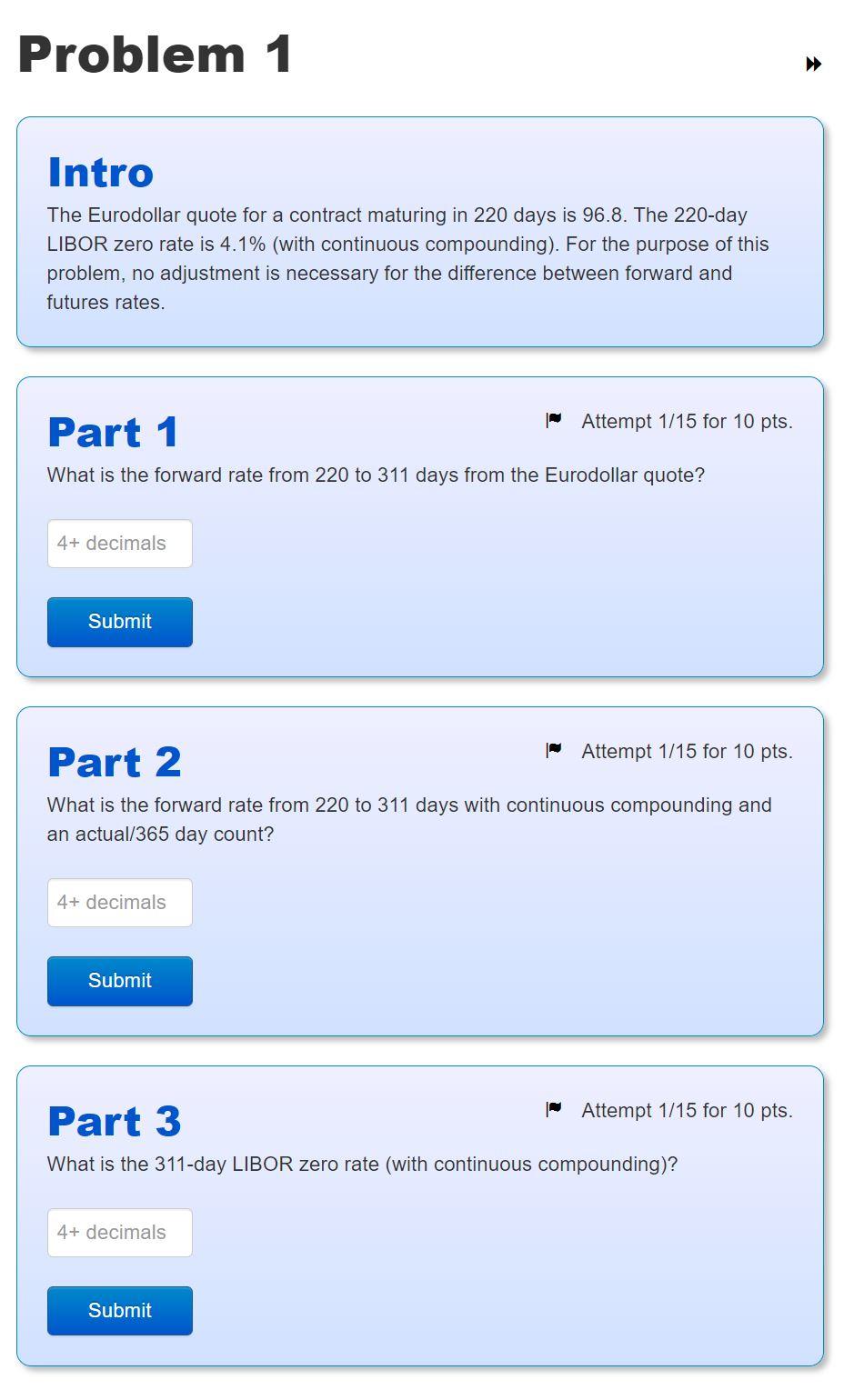

Problem 1 Intro The Eurodollar quote for a contract maturing in 220 days is 96.8. The 220-day LIBOR zero rate is 4.1% (with continuous compounding).

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Investing Revolutionaries How The Worlds Greatest Investors Take On Wall Street And Win In Any Market

Authors: James N. Whiddon , Nikki Knotts

1st Edition

0071623949,0071700560