Answered step by step

Verified Expert Solution

Question

1 Approved Answer

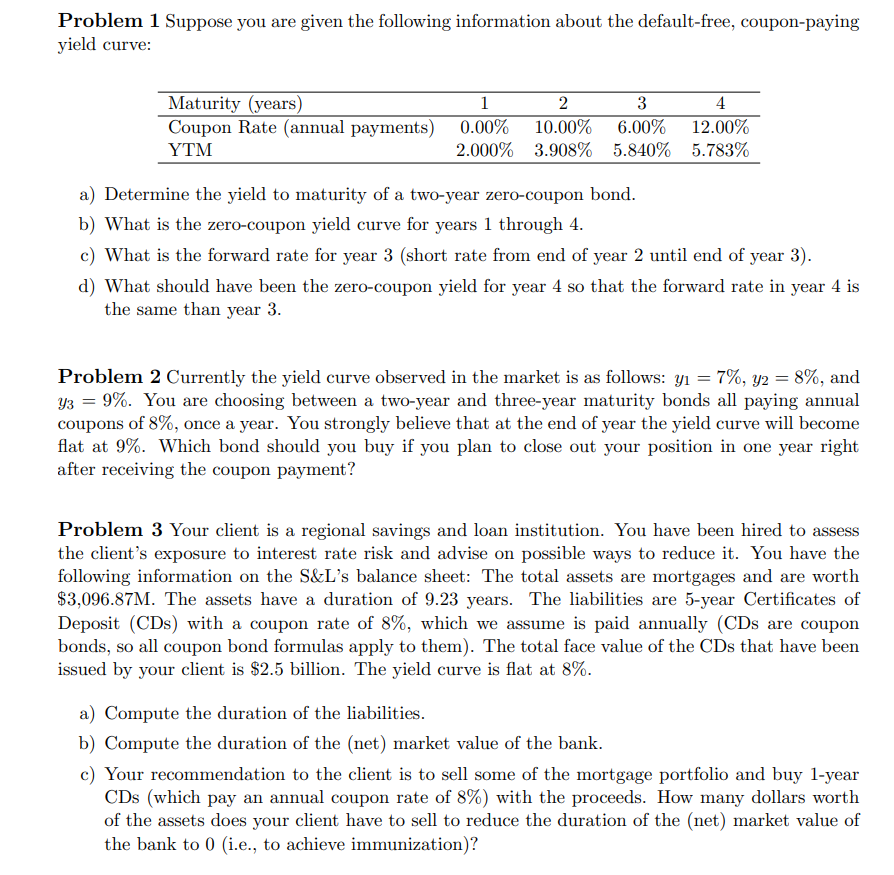

Problem 1 Suppose you are given the following information about the default-free, coupon-paying yield curve: Maturity (years) Coupon Rate (annual payments) YTM 1 2 3

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles of Auditing and Other Assurance Services

Authors: Ray Whittington, Kurt Pany

20th edition

77729145, 978-1259295430, 1259295435, 978-0077729141