Answered step by step

Verified Expert Solution

Question

1 Approved Answer

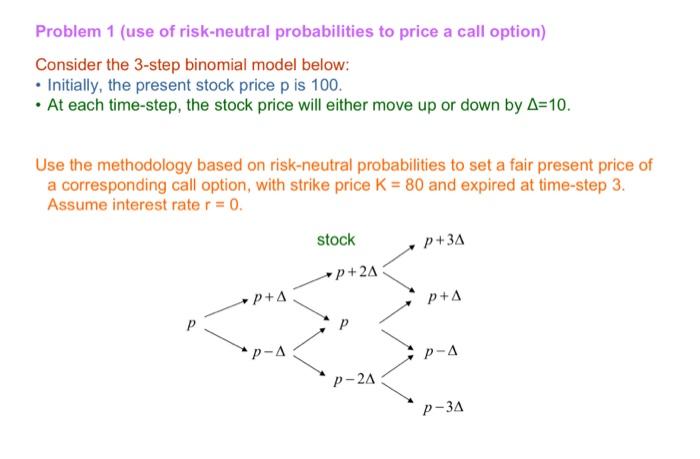

Problem 1 (use of risk-neutral probabilities to price a call option) Consider the 3-step binomial model below: Initially, the present stock price p is 100.

Problem 1 (use of risk-neutral probabilities to price a call option) Consider the 3-step binomial model below: Initially, the present stock price p is 100. At each time-step, the stock price will either move up or down by A=10. Use the methodology based on risk-neutral probabilities to set a fair present price of a corresponding call option, with strike price K = 80 and expired at time-step 3. Assume interest rate r = 0. P + A p-A stock P+2A P-2A P+3A p+A P-A P-3A

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Energy Audit Of Building Systems An Engineering Approach

Authors: Moncef Krarti

1st Edition

0849395879, 978-0849395871