Answered step by step

Verified Expert Solution

Question

1 Approved Answer

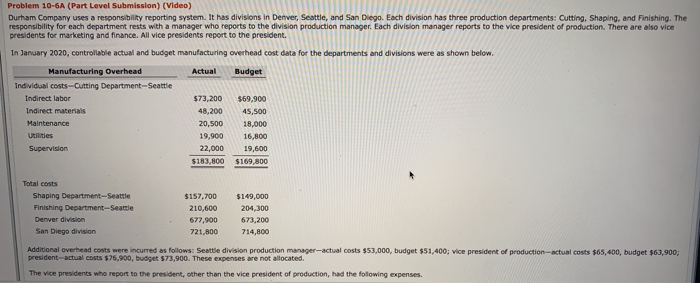

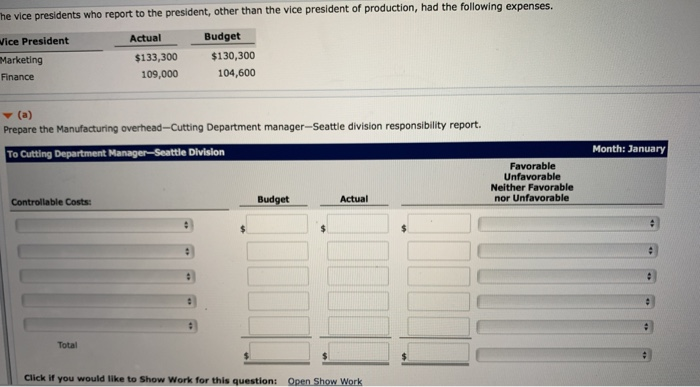

Problem 10-6A (Part Level Submission) (Video) Durham Company uses a responsibility reporting system. It has divisions in Denver, Seattle, and San Diego. Each division has

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting Version 3.0

Authors: Leah Kratz, Joe Ben Hoyle, C. J. Skender

3rd Edition

1453392904, 9781453392904