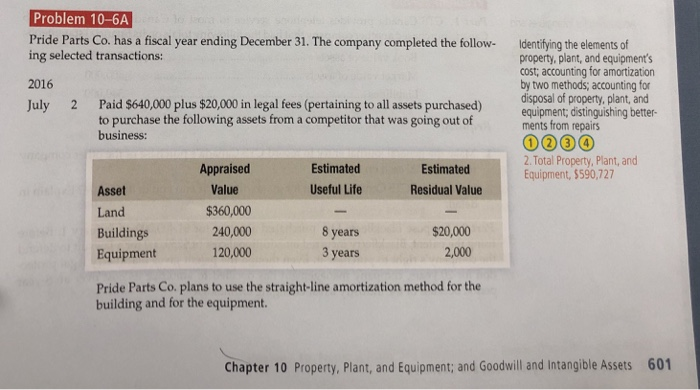

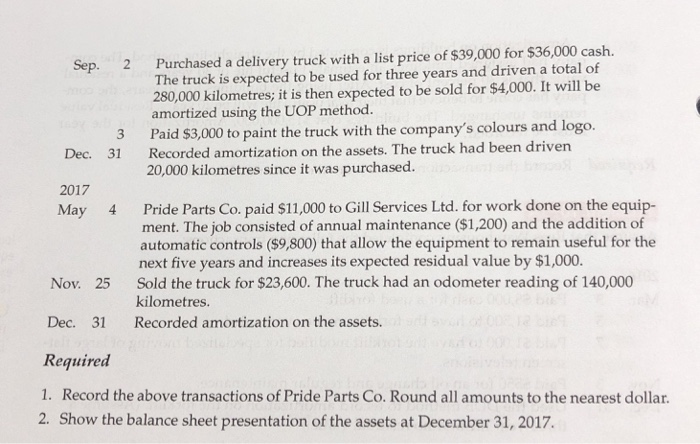

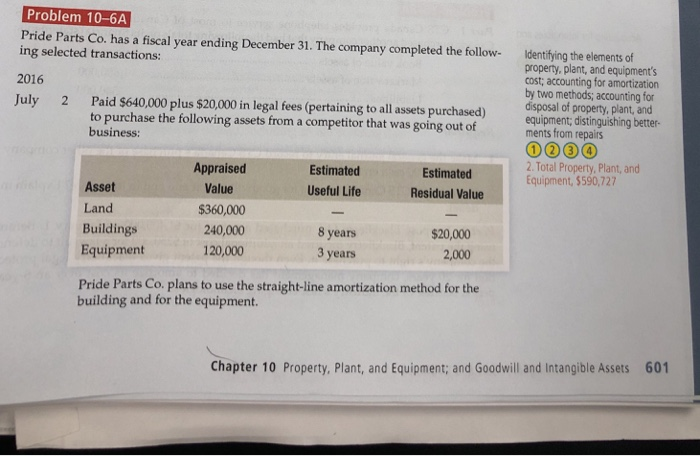

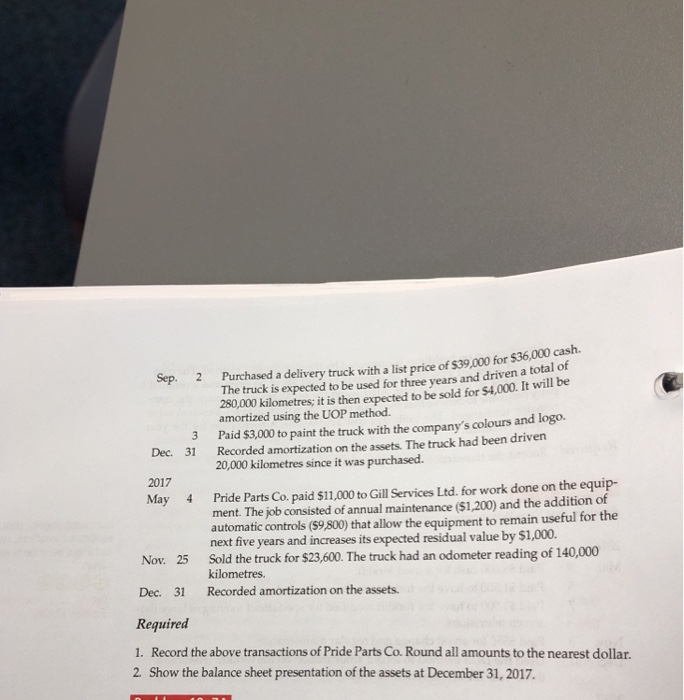

Problem 10-6A Pride Parts Co. has a fiscal year ending December 31. The company completed the follow- ldentifying the elements of property, plant, and equipment's cost, accounting for amortization by two methods; accounting f disposal of property, plant, and equipment; distinguishing better- ments from repairs ing selected transactions: 2016 July 2 Paid $640,000 plus $20,000 in legal fees (pertaining to all assets purchased) to purchase the following assets from a competitor that was going out of business: 2. Total Property, Plant, and Equipment,$590,727 Appraised Value $360,000 240,000 120,000 Estimated Useful Life Estimated Residual Value Asset Land Buildings Equipment 8 years 3 years $20,000 2,000 Pride Parts Co. plans to use the straight-line amortization method for the building and for the equipment. Chapter 10 Property, Plant, and Equipment; and Goodwill and Intangible Assets 60 Sep. 2 Purchased a delivery truck with a list price of $39,000 for $36,000 cash. The truck is expected to be used for three years and driven a total of 280,000 kilometres; it is then expected to be sold for $4,000. It will be amortized using the UOP method. Paid $3,000 to paint the truck with the company's colours and logo. Recorded amortization on the assets. The truck had been driven 20,000 kilometres since it was purchased. 3 31 Dec. 2017 May Pride Parts Co. paid $11,000 to Gill Services Ltd. for work done on the equip- 4 ment. The job consisted of annual maintenance ($1,200) and the addition of automatic controls ($9,800) that allow the equipment to remain useful for the next five years and increases its expected residual value by $1,000. Nov. 25 Sold the truck for $23,600. The truck had an odometer reading of 140,000 Dec. 31 Recorded amortization on the assets. Required 1. Record the above transactions of Pride Parts Co. Round all amounts to the nearest dollar 2. Show the balance sheet presentation of the assets at December 31, 2017. kilometres. Problem 10-6A Pride Parts Co. has a fiscal year ending December 31. The company completed the follow- Identifying the elements of ing selected transactions: 2016 July 2 Paid $640,000 plus $20,000 in legal fees (pertaining to all assets purchased) property, plant, and equipment's cost; accounting for amortization by two methods, accounting fo disposal of property, plant, and equiomenistinguishi to purchase the following assets from a competitor that was going out of business ments from repairs 2. Total Property, Plant, and Equipment, $590,727 Appraised Value $360,000 240,000 120,000 Estimated Useful Life Estimated Residual Value Asset Land Buildings Equipment 8 years 3 years $20,000 2,000 Pride Parts Co. plans to use the straight-line amortization method for the building and for the equipment. 601 Chapter 10 Property, Plant, and Equipment; and Goodwill and Intangible Assets $36,000 cash sep. 2 Purchased a delivery truck with a list price of $39,000 for total of 280,000 kilometres; it is then expected to be sold for $4,000. It will be 3 Paid $3,000 to paint the truck with the company's colours and logo. The truck is expected to be used for three years and driven a amortized using the UOP method. Dec. 31 Recorded amortization on the assets The truck had been driven 2017 May 4 Pride Parts Co. paid $11,000 to Gill Services Ltd. for work done on the equip- 20,000 kilometres since it was purchased. ment. The job consisted of annual maintenance ($1,200) and the addition of automatic controls (59 800) that allow the equipment to remain useful for the next five years and increases its expected residual value by $1,000. Nov. 25 Sold the truck for $23,600. The truck had an odometer reading of 140,000 Dec. 31 Recorded amortization on the assets Required 1. Record the above transactions of Pride Parts Co. Round all amounts to the nearest dollar 2. Show the balance sheet presentation of the assets at December 31, 2017 kilometres