Answered step by step

Verified Expert Solution

Question

1 Approved Answer

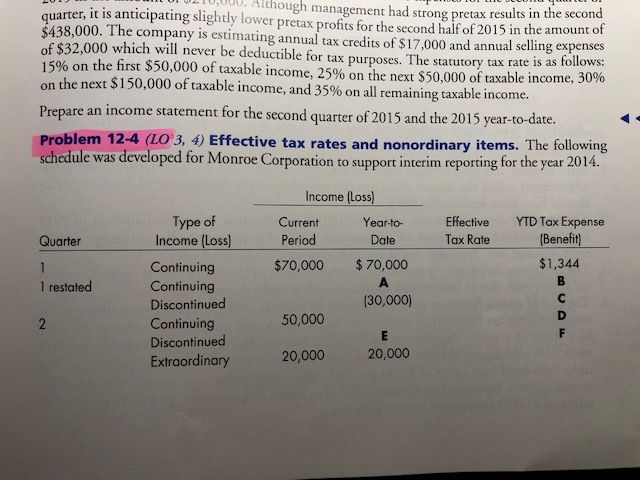

Problem 12-4: Provide the value for the items A - F with all appropriate steps. we wrzu . Mithough management had strong pretax results in

Problem 12-4: Provide the value for the items A - F with all appropriate steps.

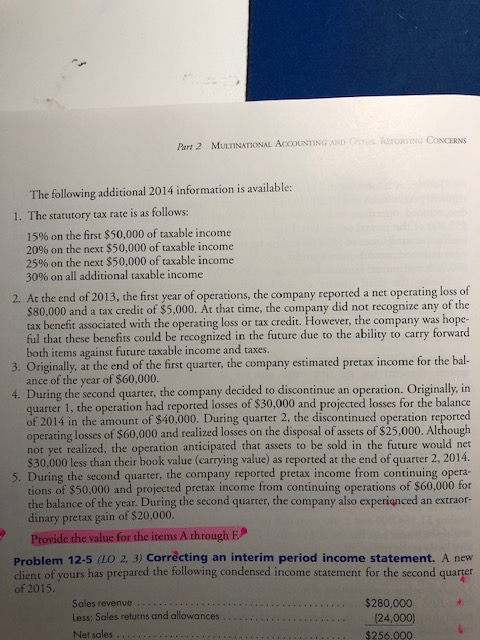

we wrzu . Mithough management had strong pretax results in the second quarter, it is anticipating slightly lower pretax profits for the second half of 2015 in the amount of $438,000. The company is estimating annual tax credits of $17.000 and annual selling expenses of $32,000 which will never be deductible for tax purposes. The statutory tax rate is as follows: 15% on the first $50,000 of taxable income, 25% on the next $50,000 of taxable income, 30% on the next $150,000 of taxable income, and 35% on all remaining taxable income. Prepare an income statement for the second quarter of 2015 and the 2015 year-to-date. Problem 12-4 (LO 3, 4) Effective tax rates and nonordinary items. The following schedule was developed for Monroe Corporation to support interim reporting for the year 2014. Income (Loss) Current Year-to- Period Date $70,000 $70,000 Effective Tax Rate YTD Tax Expense (Benefit) Quarter $1,344 1 restated Type of Income (Loss) Continuing Continuing Discontinued Continuing Discontinued Extraordinary (30,000) 50,000 20,000 20,000 Part 2 MULTINATIONAL ACCOUNTING AND BEYORING CONCERNS The following additional 2014 information is available: 1. The statutory tax rate is as follows: 15% on the first $50,000 of taxable income 20% on the next $50,000 of taxable income 25% on the next $50,000 of taxable income 30% on all additional taxable income 2. At the end of 2013, the first year of operations, the company reported a net operating loss of $80,000 and a tax credit of $5,000. At that time, the company did not recognize any of the tax benefit associated with the operating loss or tax credit. However, the company was hope- ful that these benefits could be recognized in the future due to the ability to carry forward both items against future taxable income and taxes. 3. Originally, at the end of the first quarter, the company estimated pretax income for the bal ance of the year of $60,000. 4. During the second quarter, the company decided to discontinue an operation. Originally, in quarter 1, the operation had reported losses of $30,000 and projected losses for the balance of 2014 in the amount of $40,000. During quarter 2, the discontinued operation reported operating losses of $60,000 and realized losses on the disposal of assets of $25,000. Although not yet realized, the operation anticipated that assets to be sold in the future would net $30,000 less than their book value (carrying value) as reported at the end of quarter 2, 2014. 5. During the second quarter, the company reported pretax income from continuing opera- tions of $50,000 and projected pretax income from continuing operations of $60,000 for the balance of the year. During the second quarter, the company also experienced an extraor dinary pretax gain of $20,000. Provide the value for the items A through F Problem 12.5 (LO 2, 3) Correcting an interim period income statement. A new client of yours has prepared the following condensed income statement for the second quarter of 2015. Sales revenue .... $280,000 Less: Sales returns and allowances.. (24,000) Net sales ........ .. . ....... $256,000 we wrzu . Mithough management had strong pretax results in the second quarter, it is anticipating slightly lower pretax profits for the second half of 2015 in the amount of $438,000. The company is estimating annual tax credits of $17.000 and annual selling expenses of $32,000 which will never be deductible for tax purposes. The statutory tax rate is as follows: 15% on the first $50,000 of taxable income, 25% on the next $50,000 of taxable income, 30% on the next $150,000 of taxable income, and 35% on all remaining taxable income. Prepare an income statement for the second quarter of 2015 and the 2015 year-to-date. Problem 12-4 (LO 3, 4) Effective tax rates and nonordinary items. The following schedule was developed for Monroe Corporation to support interim reporting for the year 2014. Income (Loss) Current Year-to- Period Date $70,000 $70,000 Effective Tax Rate YTD Tax Expense (Benefit) Quarter $1,344 1 restated Type of Income (Loss) Continuing Continuing Discontinued Continuing Discontinued Extraordinary (30,000) 50,000 20,000 20,000 Part 2 MULTINATIONAL ACCOUNTING AND BEYORING CONCERNS The following additional 2014 information is available: 1. The statutory tax rate is as follows: 15% on the first $50,000 of taxable income 20% on the next $50,000 of taxable income 25% on the next $50,000 of taxable income 30% on all additional taxable income 2. At the end of 2013, the first year of operations, the company reported a net operating loss of $80,000 and a tax credit of $5,000. At that time, the company did not recognize any of the tax benefit associated with the operating loss or tax credit. However, the company was hope- ful that these benefits could be recognized in the future due to the ability to carry forward both items against future taxable income and taxes. 3. Originally, at the end of the first quarter, the company estimated pretax income for the bal ance of the year of $60,000. 4. During the second quarter, the company decided to discontinue an operation. Originally, in quarter 1, the operation had reported losses of $30,000 and projected losses for the balance of 2014 in the amount of $40,000. During quarter 2, the discontinued operation reported operating losses of $60,000 and realized losses on the disposal of assets of $25,000. Although not yet realized, the operation anticipated that assets to be sold in the future would net $30,000 less than their book value (carrying value) as reported at the end of quarter 2, 2014. 5. During the second quarter, the company reported pretax income from continuing opera- tions of $50,000 and projected pretax income from continuing operations of $60,000 for the balance of the year. During the second quarter, the company also experienced an extraor dinary pretax gain of $20,000. Provide the value for the items A through F Problem 12.5 (LO 2, 3) Correcting an interim period income statement. A new client of yours has prepared the following condensed income statement for the second quarter of 2015. Sales revenue .... $280,000 Less: Sales returns and allowances.. (24,000) Net sales ........ .. . ....... $256,000Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Quality Audits For Improved Performance

Authors: Dennis R. Arter

3rd Edition

0873895703, 978-0873895705