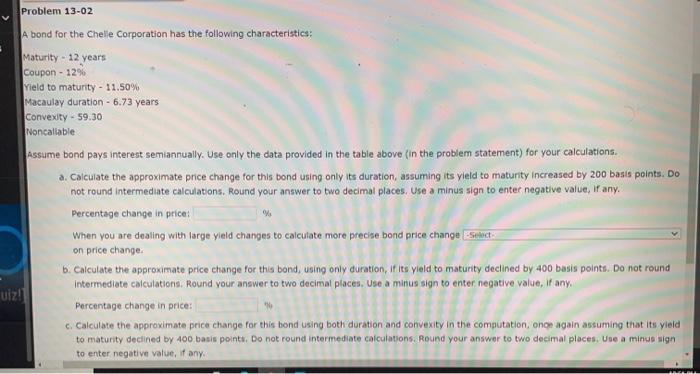

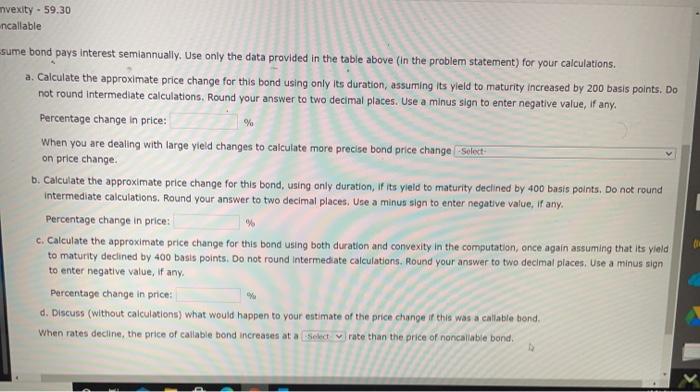

Problem 13-02 A bond for the Chelle Corporation has the following characteristics: Maturity - 12 years Coupon - 1296 Yield to maturity - 11.50% Macaulay duration - 6.73 years Convexity - 59.30 Noncalable Assume bond pays Interest semiannually. Use only the data provided in the table above (in the problem statement) for your calculations. a. Calculate the approximate price change for this bond using only its duration, assuming its yield to maturity increased by 200 basis points. Do not round Intermediate calculations, Round your answer to two decimal places. Use a minus sign to enter negative value, If any. Percentage change in price: % When you are dealing with large yield changes to calculate more precise bond price change Select on price change b. Calculate the approximate price change for this bond, using only duration, if its yield to maturity declined by 400 basis points. Do not round intermediate calculations, Round your answer to two decimal places. Use a minus sign to enter negative value, if any, uiz! Percentage change in price: c. Calculate the approximate price change for this bond using both duration and convexity in the computation, once again assuming that its yield to maturity declined by 400 basis points. Do not round intermediate calculations. Round your answer to two decimal places. Use a mindesign to enter negative value, if any. mvexity - 59.30 ncallable % sume bond pays Interest semiannually. Use only the data provided in the table above (In the problem statement) for your calculations. a. Calculate the approximate price change for this bond using only its duration, assuming its yield to maturity increased by 200 basis points. Do not round intermediate calculations. Round your answer to two decimal places. Use a minus sign to enter negative value, If any. Percentage change in price: When you are dealing with large yield changes to calculate more precise bond price change Select: on price change. b. Calculate the approximate price change for this bond, using only duration, if its yield to maturity declined by 400 basis points. Do not round intermediate calculations. Round your answer to two decimal places. Use a minus sign to enter negative value, if any. Percentage change in price: c. Calculate the approximate price change for this bond using both duration and convexity in the computation, once again assuming that its yield to maturity declined by 400 basis points. Do not round Intermediate calculations. Round your answer to two decimal places. Use a minus sign to enter negative value, if any, Parcentage change in price: d. Discuss (without calculations) what would happen to your estimate of the price change if this was a collable bond When rates decline, the price of callable bond increases at a Select rate than the price of noncallable bond