Answered step by step

Verified Expert Solution

Question

1 Approved Answer

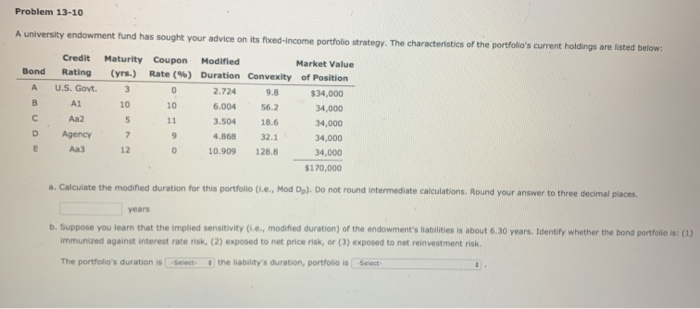

Problem 13-10 A university endowment fund has sought your advice on its fixed-income portfolio strategy. The characteristics of the portfolio's current holdings are listed below:

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Financial Management

Authors: Cheol S. Eun, Bruce G.Resnick

6th Edition

71316973, 978-0071316972, 78034655, 978-0078034657