Answered step by step

Verified Expert Solution

Question

1 Approved Answer

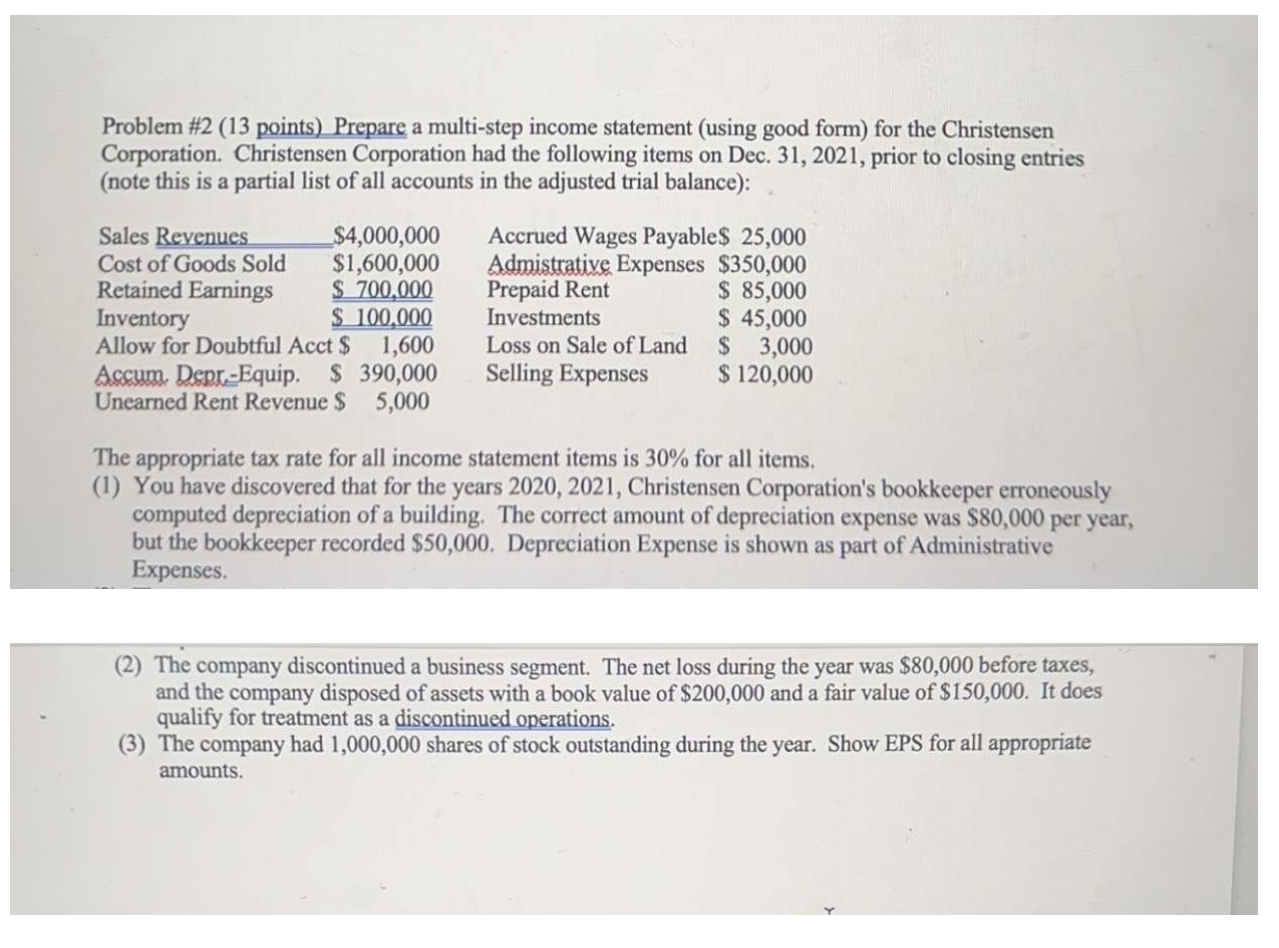

Problem #2 (13 points) Prepare a multi-step income statement (using good form) for the Christensen Corporation. Christensen Corporation had the following items on Dec. 31,

Problem \#2 (13 points) Prepare a multi-step income statement (using good form) for the Christensen Corporation. Christensen Corporation had the following items on Dec. 31, 2021, prior to closing entries (note this is a partial list of all accounts in the adjusted trial balance): The appropriate tax rate for all income statement items is 30% for all items. (1) You have discovered that for the years 2020, 2021, Christensen Corporation's bookkeeper erroneously computed depreciation of a building. The correct amount of depreciation expense was $80,000 per year, but the bookkeeper recorded $50,000. Depreciation Expense is shown as part of Administrative Expenses. (2) The company discontinued a business segment. The net loss during the year was $80,000 before taxes, and the company disposed of assets with a book value of $200,000 and a fair value of $150,000. It does qualify for treatment as a discontinued operations. (3) The company had 1,000,000 shares of stock outstanding during the year. Show EPS for all appropriate amounts

Problem \#2 (13 points) Prepare a multi-step income statement (using good form) for the Christensen Corporation. Christensen Corporation had the following items on Dec. 31, 2021, prior to closing entries (note this is a partial list of all accounts in the adjusted trial balance): The appropriate tax rate for all income statement items is 30% for all items. (1) You have discovered that for the years 2020, 2021, Christensen Corporation's bookkeeper erroneously computed depreciation of a building. The correct amount of depreciation expense was $80,000 per year, but the bookkeeper recorded $50,000. Depreciation Expense is shown as part of Administrative Expenses. (2) The company discontinued a business segment. The net loss during the year was $80,000 before taxes, and the company disposed of assets with a book value of $200,000 and a fair value of $150,000. It does qualify for treatment as a discontinued operations. (3) The company had 1,000,000 shares of stock outstanding during the year. Show EPS for all appropriate amounts Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Payroll Accounting 2016

Authors: Bernard J. Bieg, Judith Toland

26th edition

978-1305665910, 1305665910, 1337072648, 978-1337072649