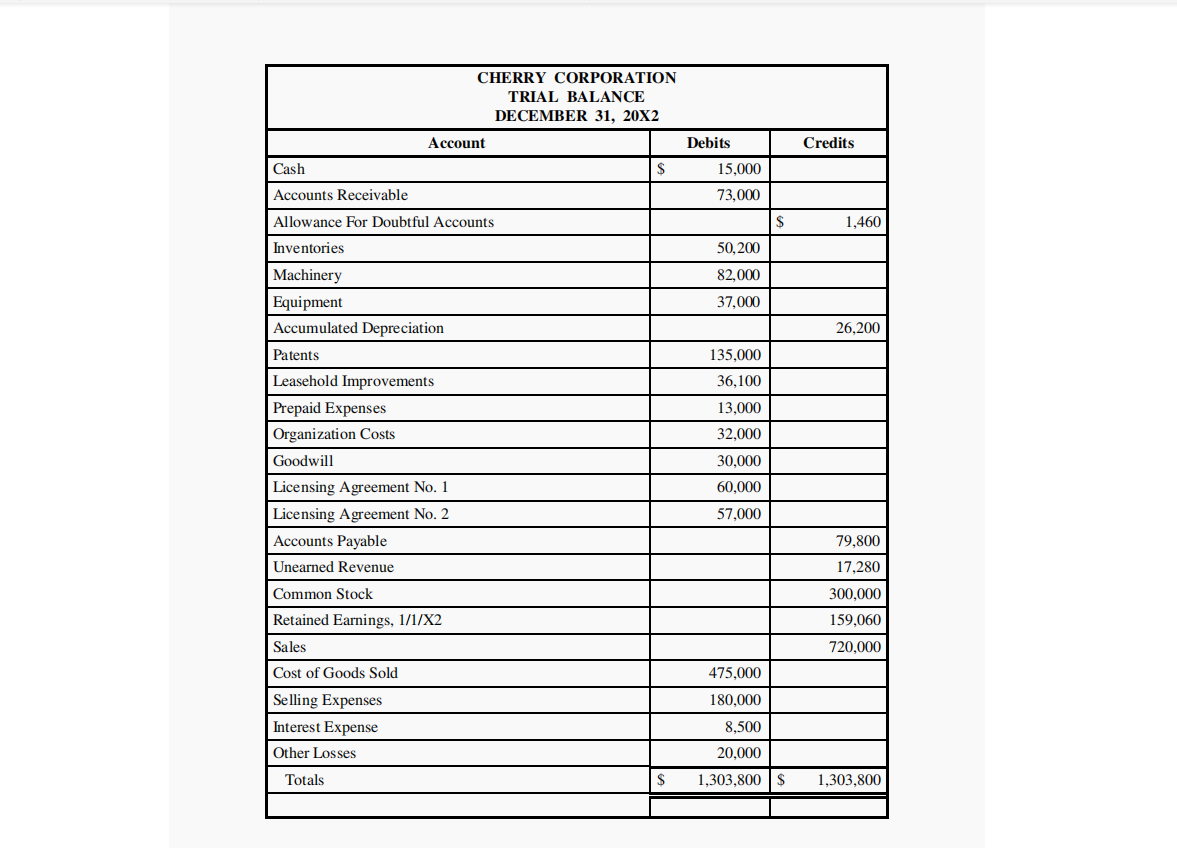

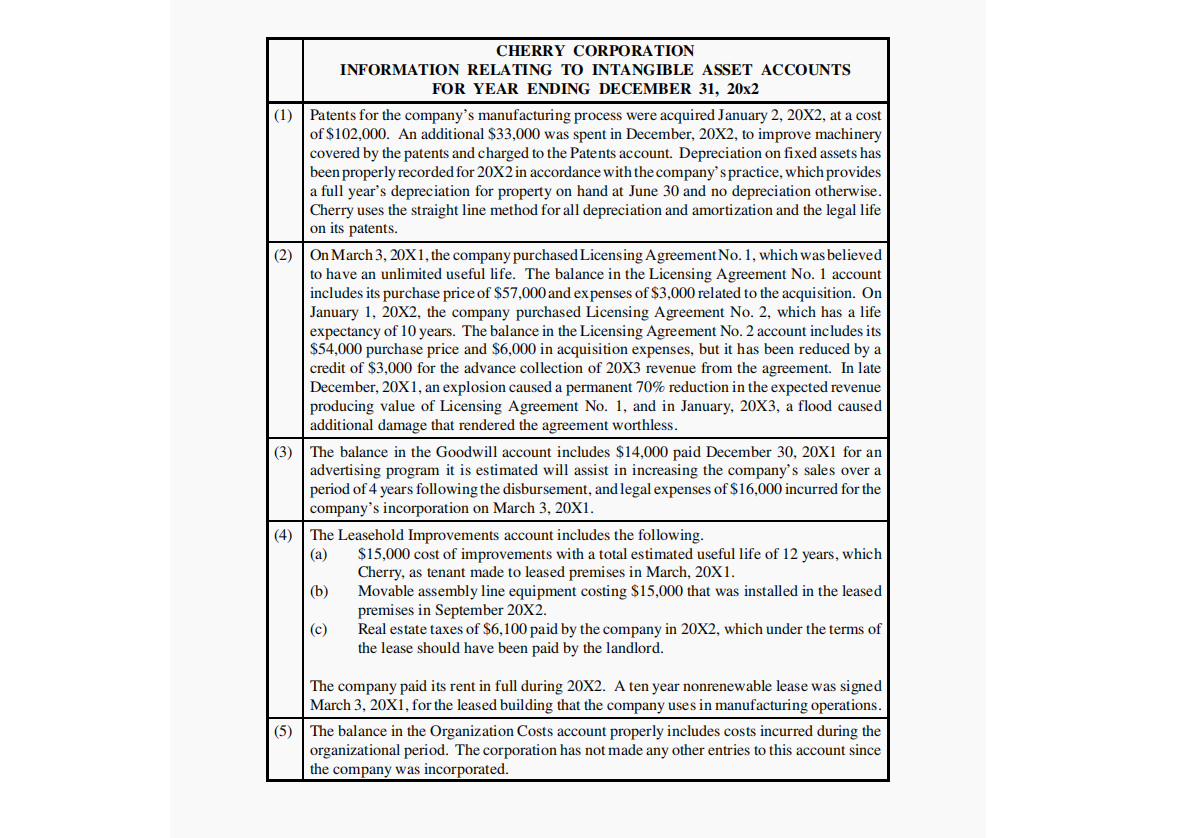

Problem 2 (25 points). Cherry Corporation was incorporated on March 3, 20X1. The corporation's financial statements for its first year of operations were not examined by a CPA. You have been engaged to examine the financial statements for the year ending December 31, 20X2, and your examination is substantially completed. The corporation's trial balance at December 31, 20X2 is attached. The attached information relates to accounts that may require adjustments. REQUIRED: Prepare an eight column worksheet to adjust accounts that require adjustment and include columns for an income statement and a balance sheet. The format should appear as follows. (a) A column for the account title. Two columns for the unadjusted trial balance amounts (debit and credit). Two columns for the adjustments (debit and credit). Two columns for the income statement (debit and credit). (e) Two columns for the balance sheet (debit and credit). (b) A separate account should be used for the accumulation of each type of amortization and for each prior period adjustment. Formal adjusting entries and financial statements are not required. Credits Debits 15,000 73,000 $ 1,460 50,200 82,000 37,000 26,200 CHERRY CORPORATION TRIAL BALANCE DECEMBER 31, 20X2 Account Cash $ Accounts Receivable Allowance For Doubtful Accounts Inventories Machinery Equipment Accumulated Depreciation | Patents Leasehold Improvements Prepaid Expenses Organization Costs Goodwill Licensing Agreement No. 1 Licensing Agreement No. 2 Accounts Payable Unearned Revenue Common Stock Retained Earnings, 1/1/X2 135,000 36,100 13,000 32,000 30,000 60,000 57,000 79,800 17,280 300,000 159,060 720,000 Sales Cost of Goods Sold Selling Expenses Interest Expense Other Losses Totals 475,000 180,000 8,500 20,000 1,303,800 T $ $ 1,303,800 (1) CHERRY CORPORATION INFORMATION RELATING TO INTANGIBLE ASSET ACCOUNTS FOR YEAR ENDING DECEMBER 31, 20x2 Patents for the company's manufacturing process were acquired January 2, 20X2, at a cost of $102,000. An additional $33,000 was spent in December, 20X2, to improve machinery covered by the patents and charged to the Patents account. Depreciation on fixed assets has been properly recorded for 20X2 in accordance with the company's practice, which provides a full year's depreciation for property on hand at June 30 and no depreciation otherwise. Cherry uses the straight line method for all depreciation and amortization and the legal life on its patents. On March 3, 20X1, the company purchased Licensing Agreement No. 1, which was believed to have an unlimited useful life. The balance in the Licensing Agreement No. 1 account includes its purchase price of $57,000 and expenses of $3,000 related to the acquisition. On January 1, 20X2, the company purchased Licensing Agreement No. 2, which has a life expectancy of 10 years. The balance in the Licensing Agreement No. 2 account includes its $54,000 purchase price and $6,000 in acquisition expenses, but it has been reduced by a credit of $3,000 for the advance collection of 20X3 revenue from the agreement. In late December, 20X1, an explosion caused a permanent 70% reduction in the expected revenue producing value of Licensing Agreement No. 1, and in January, 20X3, a flood caused additional damage that rendered the agreement worthless. The balance in the Goodwill account includes $14,000 paid December 30, 20X1 for an advertising program it is estimated will assist in increasing the company's sales over a period of 4 years following the disbursement, and legal expenses of $16,000 incurred for the company's incorporation on March 3, 20X1. The Leasehold Improvements account includes the following. (a $15,000 cost of improvements with a total estimated useful life of 12 years, which Cherry, as tenant made to leased premises in March, 20X1. Movable assembly line equipment costing $15,000 that was installed in the leased premises in September 20X2. (c) Real estate taxes of $6,100 paid by the company in 20X2, which under the terms of the lease should have been paid by the landlord. (4) (b) (5) The company paid its rent in full during 20X2. A ten year nonrenewable lease was signed March 3, 20X1, for the leased building that the company uses in manufacturing operations. The balance in the Organization Costs account properly includes costs incurred during the organizational period. The corporation has not made any other entries to this account since the company was incorporated Problem 2 (25 points). Cherry Corporation was incorporated on March 3, 20X1. The corporation's financial statements for its first year of operations were not examined by a CPA. You have been engaged to examine the financial statements for the year ending December 31, 20X2, and your examination is substantially completed. The corporation's trial balance at December 31, 20X2 is attached. The attached information relates to accounts that may require adjustments. REQUIRED: Prepare an eight column worksheet to adjust accounts that require adjustment and include columns for an income statement and a balance sheet. The format should appear as follows. (a) A column for the account title. Two columns for the unadjusted trial balance amounts (debit and credit). Two columns for the adjustments (debit and credit). Two columns for the income statement (debit and credit). (e) Two columns for the balance sheet (debit and credit). (b) A separate account should be used for the accumulation of each type of amortization and for each prior period adjustment. Formal adjusting entries and financial statements are not required. Credits Debits 15,000 73,000 $ 1,460 50,200 82,000 37,000 26,200 CHERRY CORPORATION TRIAL BALANCE DECEMBER 31, 20X2 Account Cash $ Accounts Receivable Allowance For Doubtful Accounts Inventories Machinery Equipment Accumulated Depreciation | Patents Leasehold Improvements Prepaid Expenses Organization Costs Goodwill Licensing Agreement No. 1 Licensing Agreement No. 2 Accounts Payable Unearned Revenue Common Stock Retained Earnings, 1/1/X2 135,000 36,100 13,000 32,000 30,000 60,000 57,000 79,800 17,280 300,000 159,060 720,000 Sales Cost of Goods Sold Selling Expenses Interest Expense Other Losses Totals 475,000 180,000 8,500 20,000 1,303,800 T $ $ 1,303,800 (1) CHERRY CORPORATION INFORMATION RELATING TO INTANGIBLE ASSET ACCOUNTS FOR YEAR ENDING DECEMBER 31, 20x2 Patents for the company's manufacturing process were acquired January 2, 20X2, at a cost of $102,000. An additional $33,000 was spent in December, 20X2, to improve machinery covered by the patents and charged to the Patents account. Depreciation on fixed assets has been properly recorded for 20X2 in accordance with the company's practice, which provides a full year's depreciation for property on hand at June 30 and no depreciation otherwise. Cherry uses the straight line method for all depreciation and amortization and the legal life on its patents. On March 3, 20X1, the company purchased Licensing Agreement No. 1, which was believed to have an unlimited useful life. The balance in the Licensing Agreement No. 1 account includes its purchase price of $57,000 and expenses of $3,000 related to the acquisition. On January 1, 20X2, the company purchased Licensing Agreement No. 2, which has a life expectancy of 10 years. The balance in the Licensing Agreement No. 2 account includes its $54,000 purchase price and $6,000 in acquisition expenses, but it has been reduced by a credit of $3,000 for the advance collection of 20X3 revenue from the agreement. In late December, 20X1, an explosion caused a permanent 70% reduction in the expected revenue producing value of Licensing Agreement No. 1, and in January, 20X3, a flood caused additional damage that rendered the agreement worthless. The balance in the Goodwill account includes $14,000 paid December 30, 20X1 for an advertising program it is estimated will assist in increasing the company's sales over a period of 4 years following the disbursement, and legal expenses of $16,000 incurred for the company's incorporation on March 3, 20X1. The Leasehold Improvements account includes the following. (a $15,000 cost of improvements with a total estimated useful life of 12 years, which Cherry, as tenant made to leased premises in March, 20X1. Movable assembly line equipment costing $15,000 that was installed in the leased premises in September 20X2. (c) Real estate taxes of $6,100 paid by the company in 20X2, which under the terms of the lease should have been paid by the landlord. (4) (b) (5) The company paid its rent in full during 20X2. A ten year nonrenewable lease was signed March 3, 20X1, for the leased building that the company uses in manufacturing operations. The balance in the Organization Costs account properly includes costs incurred during the organizational period. The corporation has not made any other entries to this account since the company was incorporated