Answered step by step

Verified Expert Solution

Question

1 Approved Answer

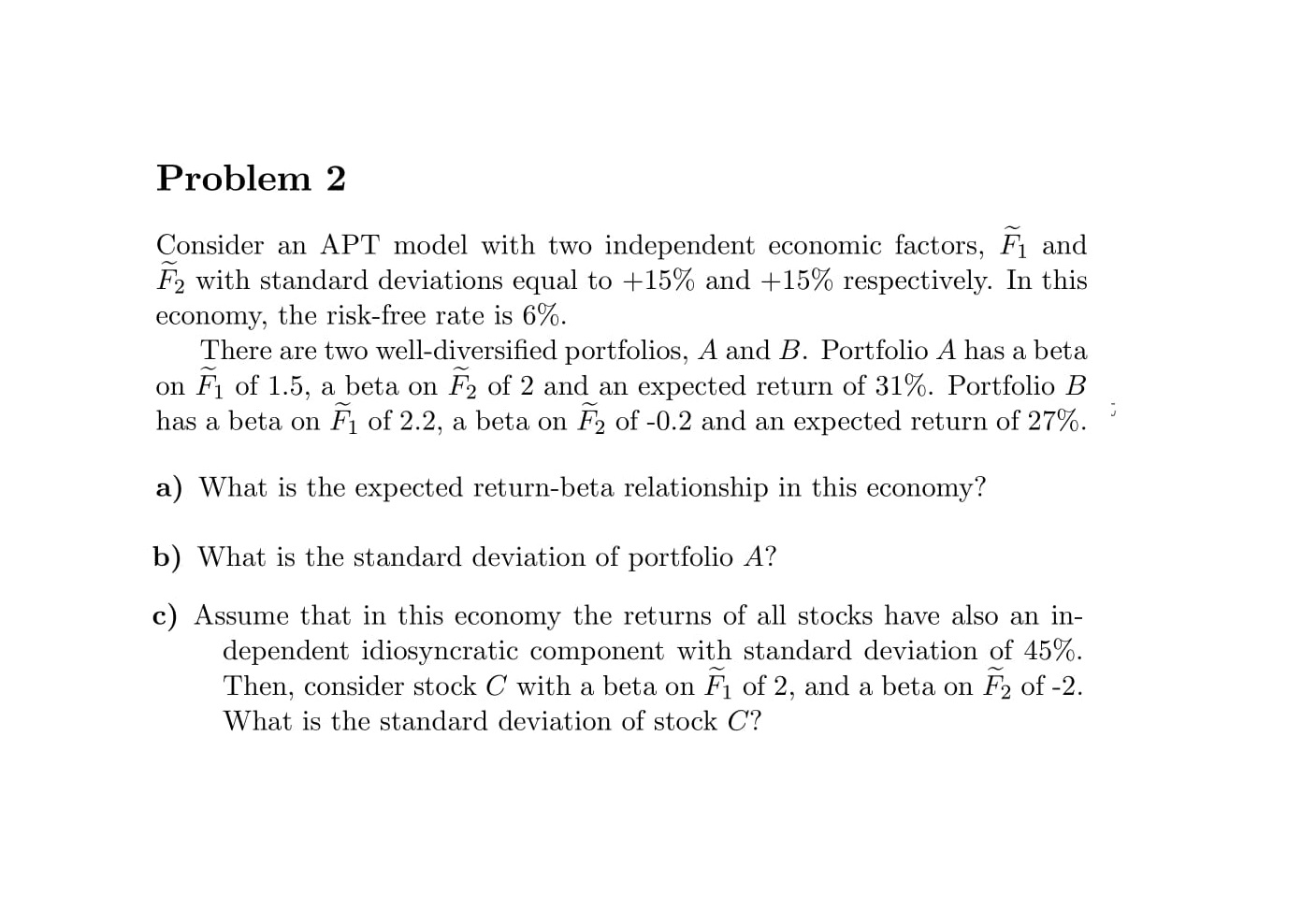

Problem 2 Consider an APT model with two independent economic factors, i and F2 with standard deviations equal to +15% and +15% respectively. In this

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting For Risk In The Nhs

Authors: P. Fenn, S. Diacon, R. Hodges, P. Watson

2nd Edition

1859713491, 978-1859713495