Answered step by step

Verified Expert Solution

Question

1 Approved Answer

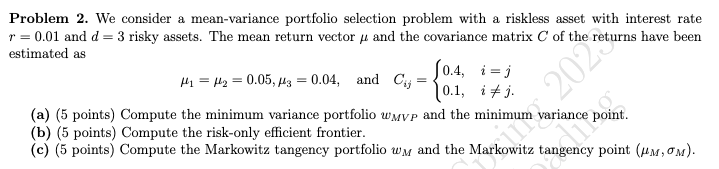

Problem 2. We consider 3 meshvariance portfolio selection problem with e. riskless asset with interest rate r = [1.01 and d = 3 risky assets.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Linear Algebra A Modern Introduction

Authors: David Poole

4th edition

1285463242, 978-1285982830, 1285982835, 978-1285463247