Answered step by step

Verified Expert Solution

Question

1 Approved Answer

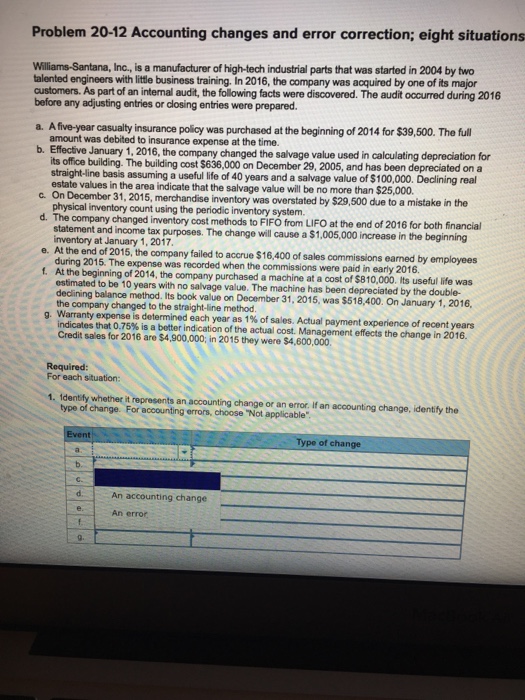

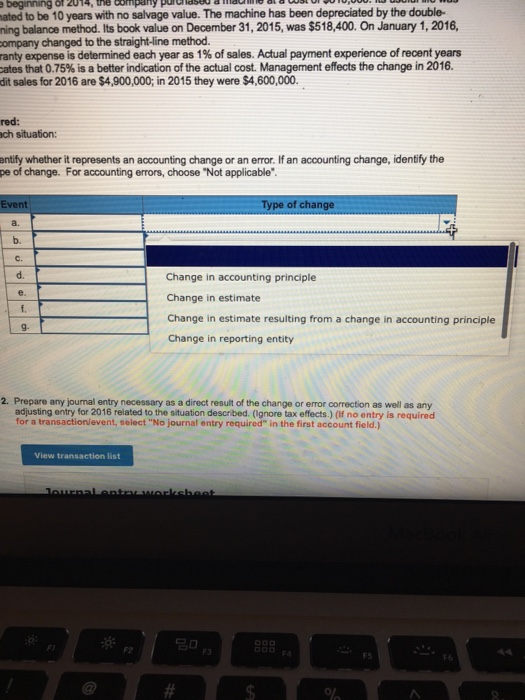

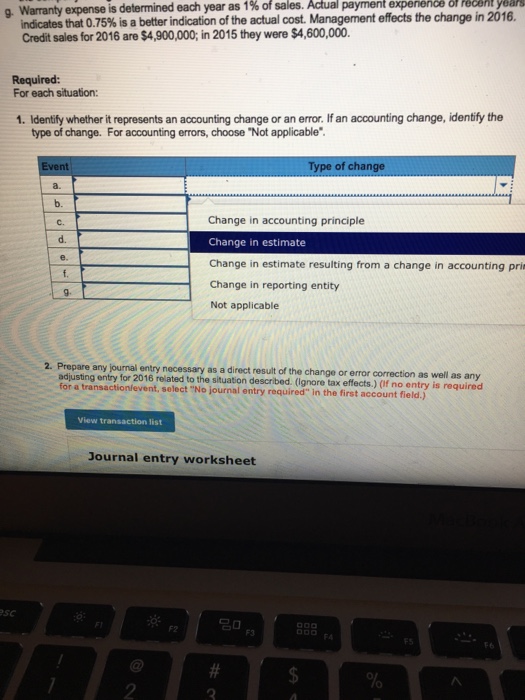

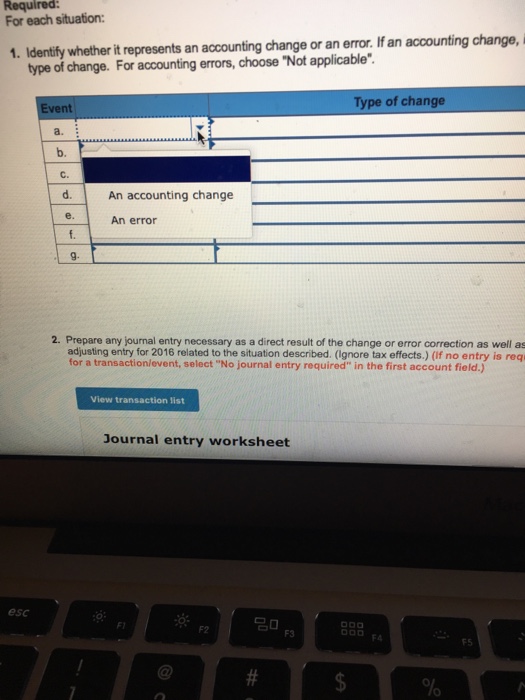

Problem 20-12 Accounting changes and error correction; eight situations Williams-Santana, Inc., is a manufacturer of high-tech industrial parts that was started in 2004 by two

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Employers Guide To Surviving Payroll And Human Resources Audits 2019

Authors: Paul E Love

1st Edition

1073422771, 978-1073422777