Answered step by step

Verified Expert Solution

Question

1 Approved Answer

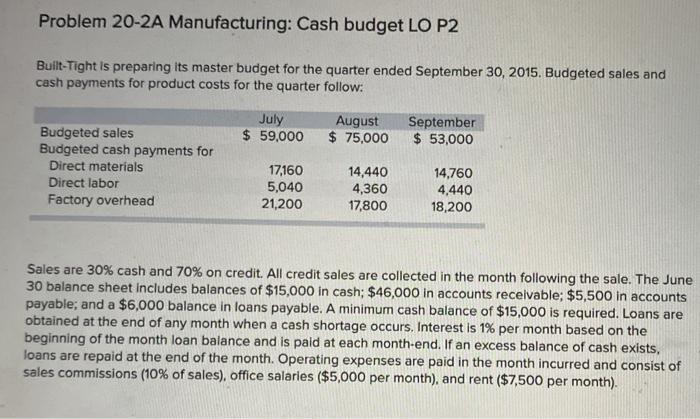

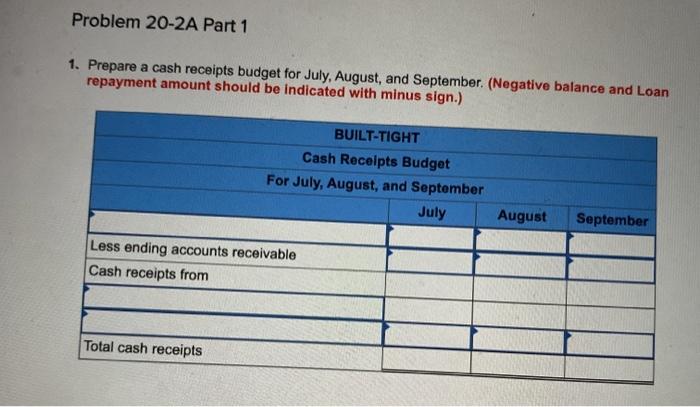

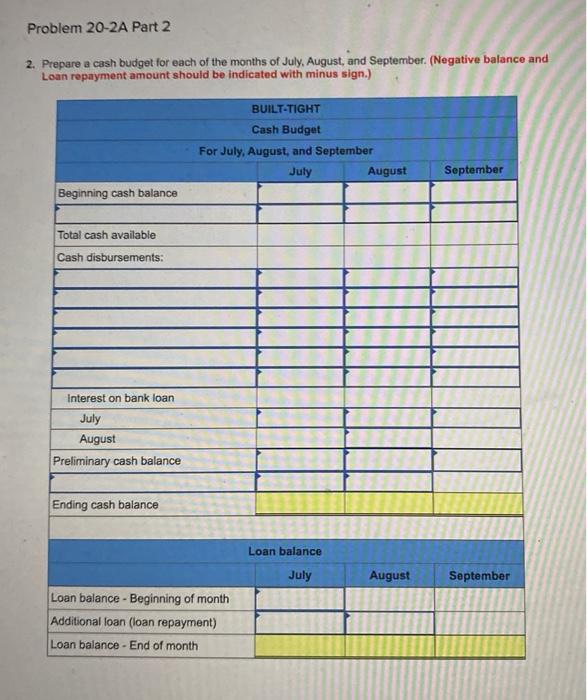

Problem 20-2A Manufacturing: Cash budget LO P2 Built-Tight is preparing its master budget for the quarter ended September 30, 2015. Budgeted sales and cash payments

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Evaluating Web Sites For Legal Compliance Basics For Web Site Legal Auditing

Authors: Leopoldo Brandt Graterol, John Ng'ang'a Gathegi

1st Edition

0810844737, 978-0810844735