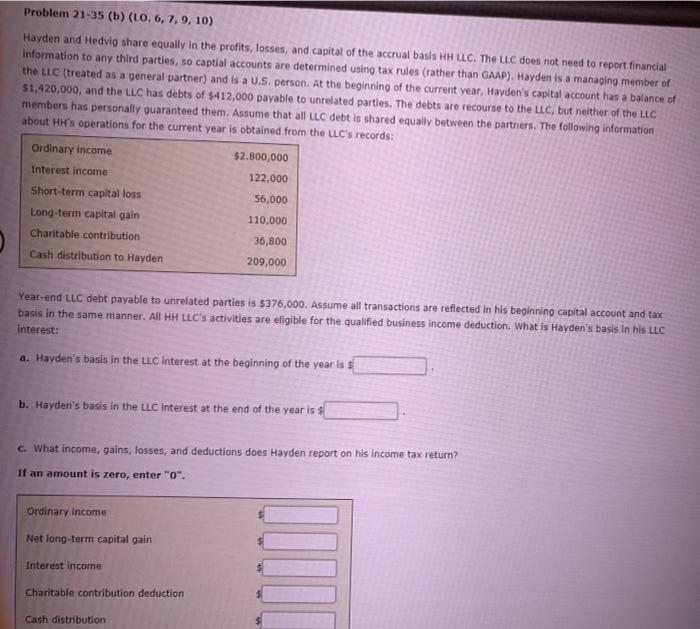

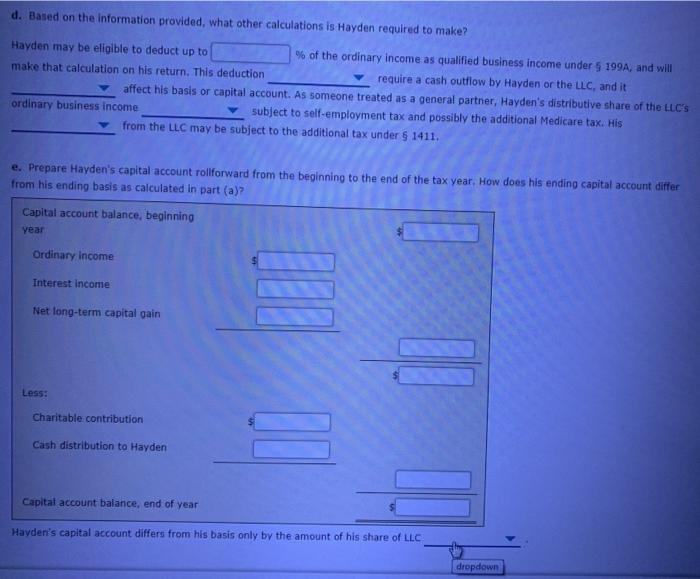

Problem 21-35 (b) (L0.6, 7, 9, 10) Hayden and Hedvig share equally in the profits, losses, and capital of the accrual basis HH LLC, The LLC does not need to report financial Information to any third parties, to captial accounts are determined using tax rules (rather than GAAP). Hayden is a managing member of the LLC (treated as a general partner) and is a U.S. person. At the beginning of the current year, Hayden's capital account has a balance of $1,420,000, and the LLC has debts of $412,000 payable to unrelated parties. The debts are recourse to the LLC, but neither of the LLC members has personally guaranteed them. Assume that all LLC debt is shared equally between the partners. The following information about Hi's operations for the current year is obtained from the LLC's records: Ordinary income $2.800,000 Interest income 122,000 Short-term capital loss 56,000 Long-term capital gain 110,000 Charitable contribution 36,800 Cash distribution to Hayden 209,000 Year-end LLC debt payable to unrelated parties is $376,000. Assume all transactions are reflected in his beginning capital account and tax basis in the same manner. All HH LLC's activities are eligible for the qualified business income deduction. What is Hayden's basis in his LLC Interest: a. Hayden's basis in the LLC interest at the beginning of the year is $ b. Hayden's basis in the LLC Interest at the end of the year is s c. What income, gains, losses, and deductions does Hayden report on his income tax return? If an amount is zero, enter "O". Ordinary income Net long-term capital gain Interest income HIILI Charitable contribution deduction Cash distribution d. Based on the information provided, what other calculations is Hayden required to make? Hayden may be eligible to deduct up to % of the ordinary income as qualified business income under 5 199A, and will make that calculation on his return. This deduction require a cash outflow by Hayden or the LLC, and it affect his basis or capital account. As someone treated as a general partner, Hayden's distributive share of the LLC's ordinary business income subject to self-employment tax and possibly the additional Medicare tax. His from the LLC may be subject to the additional tax under $ 1411. e. Prepare Hayden's capital account rollforward from the beginning to the end of the tax year. How does his ending capital account differ from his ending basis as calculated in part (a)? Capital account balance, beginning year Ordinary Income Interest income Net long-term capital gain Less: Charitable contribution Cash distribution to Hayden Capital account balance, end of year Hayden's capital account differs from his basis only by the amount of his share of LLC dropdown Problem 21-35 (b) (L0.6, 7, 9, 10) Hayden and Hedvig share equally in the profits, losses, and capital of the accrual basis HH LLC, The LLC does not need to report financial Information to any third parties, to captial accounts are determined using tax rules (rather than GAAP). Hayden is a managing member of the LLC (treated as a general partner) and is a U.S. person. At the beginning of the current year, Hayden's capital account has a balance of $1,420,000, and the LLC has debts of $412,000 payable to unrelated parties. The debts are recourse to the LLC, but neither of the LLC members has personally guaranteed them. Assume that all LLC debt is shared equally between the partners. The following information about Hi's operations for the current year is obtained from the LLC's records: Ordinary income $2.800,000 Interest income 122,000 Short-term capital loss 56,000 Long-term capital gain 110,000 Charitable contribution 36,800 Cash distribution to Hayden 209,000 Year-end LLC debt payable to unrelated parties is $376,000. Assume all transactions are reflected in his beginning capital account and tax basis in the same manner. All HH LLC's activities are eligible for the qualified business income deduction. What is Hayden's basis in his LLC Interest: a. Hayden's basis in the LLC interest at the beginning of the year is $ b. Hayden's basis in the LLC Interest at the end of the year is s c. What income, gains, losses, and deductions does Hayden report on his income tax return? If an amount is zero, enter "O". Ordinary income Net long-term capital gain Interest income HIILI Charitable contribution deduction Cash distribution d. Based on the information provided, what other calculations is Hayden required to make? Hayden may be eligible to deduct up to % of the ordinary income as qualified business income under 5 199A, and will make that calculation on his return. This deduction require a cash outflow by Hayden or the LLC, and it affect his basis or capital account. As someone treated as a general partner, Hayden's distributive share of the LLC's ordinary business income subject to self-employment tax and possibly the additional Medicare tax. His from the LLC may be subject to the additional tax under $ 1411. e. Prepare Hayden's capital account rollforward from the beginning to the end of the tax year. How does his ending capital account differ from his ending basis as calculated in part (a)? Capital account balance, beginning year Ordinary Income Interest income Net long-term capital gain Less: Charitable contribution Cash distribution to Hayden Capital account balance, end of year Hayden's capital account differs from his basis only by the amount of his share of LLC dropdown