Answered step by step

Verified Expert Solution

Question

1 Approved Answer

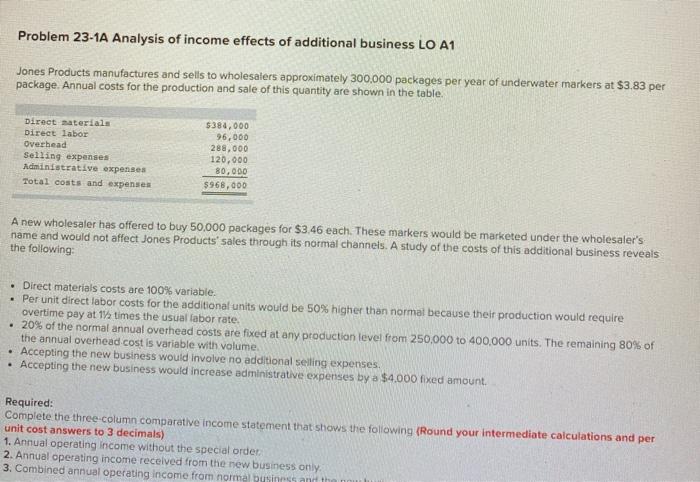

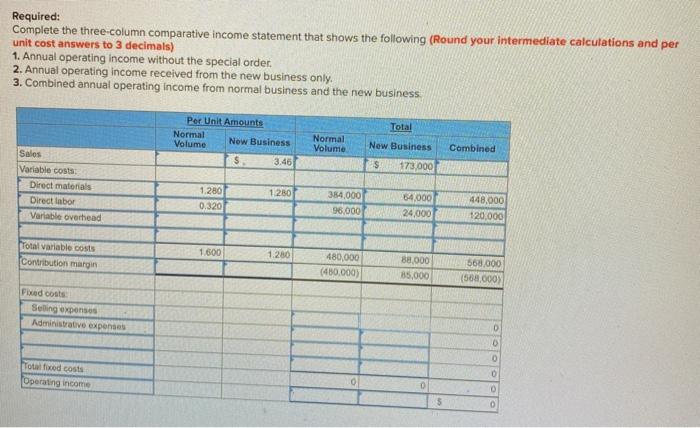

Problem 23-1A Analysis of income effects of additional business LO A1 Jones Products manufactures and sells to wholesalers approximately 300,000 packages per year of underwater

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Audit Studies Behind The Scenes With Theory Method And Nuance

Authors: S. Michael Gaddis

1st Edition

3030100200, 978-3030100209