Answered step by step

Verified Expert Solution

Question

1 Approved Answer

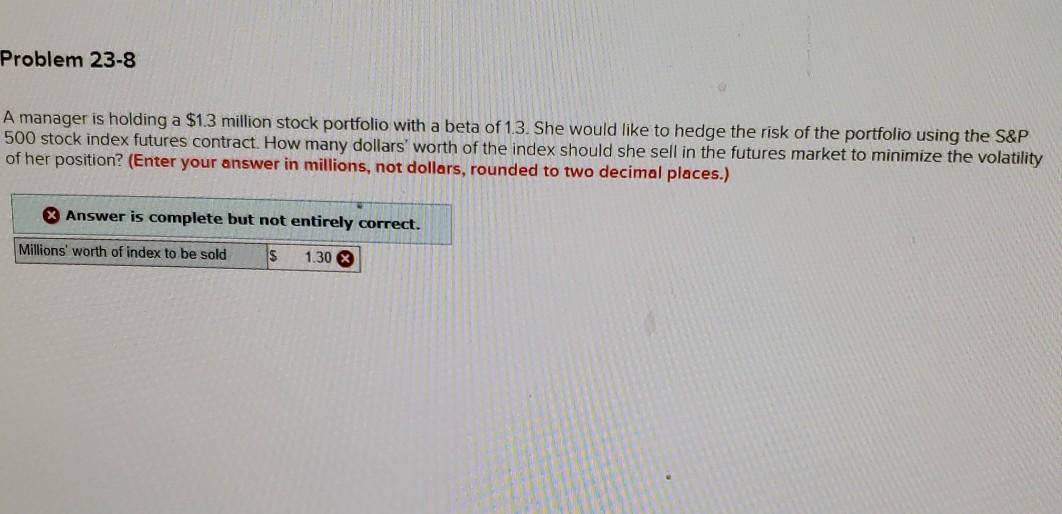

Problem 23-8 A manager is holding a $1.3 million stock portfolio with a beta of 1.3. She would like to hedge the risk of the

Problem 23-8 A manager is holding a $1.3 million stock portfolio with a beta of 1.3. She would like to hedge the risk of the portfolio using the S&P 500 stock index futures contract. How many dollars' worth of the index should she sell in the futures market to minimize the volatility of her position? (Enter your answer in millions, not dollars, rounded to two decimal places.) X Answer is complete but not entirely correct. Millions' worth of index to be sold is 1.30

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Options Trading Crash Course

Authors: Jay Douglas

1st Edition

1689360070, 978-1689360074