Answered step by step

Verified Expert Solution

Question

1 Approved Answer

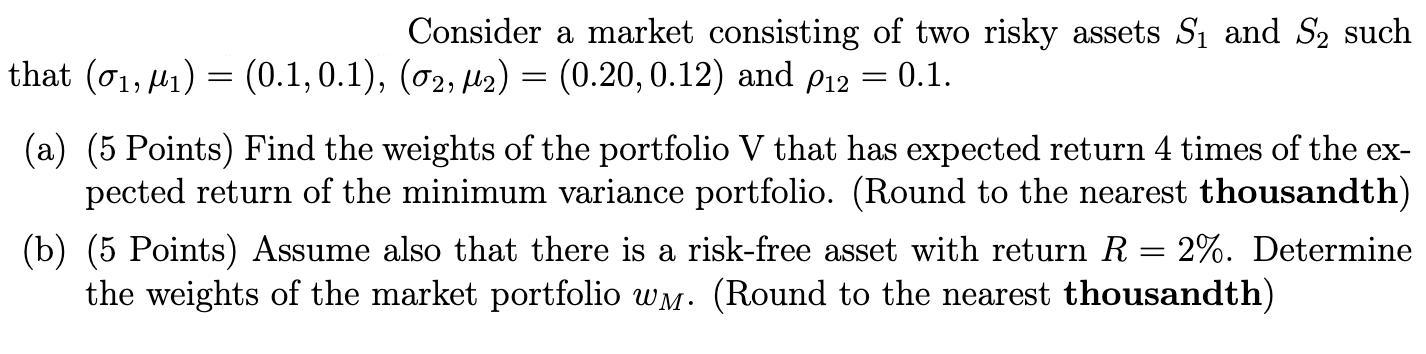

Consider a market consisting of two risky assets S and S such that (0, 1) (0.1, 0.1), (02, 2) = (0.20, 0.12) and P12

Consider a market consisting of two risky assets S and S such that (0, 1) (0.1, 0.1), (02, 2) = (0.20, 0.12) and P12 = 0.1. = (a) (5 Points) Find the weights of the portfolio V that has expected return 4 times of the ex- pected return of the minimum variance portfolio. (Round to the nearest thousandth) (b) (5 Points) Assume also that there is a risk-free asset with return R = 2%. Determine the weights of the market portfolio wm. (Round to the nearest thousandth)

Step by Step Solution

★★★★★

3.43 Rating (156 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Economics

Authors: William F. Samuelson, Stephen G. Marks

8th edition

1118808940, 978-1119025900, 1119025907, 978-1119025924, 978-1118808948